UST Risk Assessment

ParaFi is in support of adding UST to AAVE v2 and v3. UST on AAVE will likely drive additional stablecoin liquidity and borrow demand to AAVE.

The version of UST added will be USTw (Wormhole UST). This is due to Terra migrating from the centralized Shuttle Bridge to the decentralized Wormhole V2 bridge. The Wormhole Network underpins the bridge with a validator set that observes the chains it’s connected on. The Network is governed by 19 guardians that watch connected chains and sign message observations. Users deposit funds onto the token bridge from where their tokens are originating (e.g. UST on Terra) and the action is deconstructed into a message which is sent to the Wormhole Network who validates it and produces a signed message. The signed message is sent to the output token bridge (e.g. USTw on Ethereum) which verifies it and sends the user the wrapped bridge tokens.

The UST peg to $1.00 is maintained through an open market arbitrage system facilitated by Terra’s market module. An explanation of the contraction system is outlined below from the Terra docs.

If 1 UST is trading at .99 USD, users can buy 1 UST for .99 USD. Users then utilize Terra Station’s market swap function to trade 1 UST for 1 USD of Luna. The swap burns 1 UST and mints 1 USD of Luna. Users profit .01 UST from the swap. This arbitrage continues, and UST is burned to mint Luna until the price of UST rises back to 1 USD.

The reverse works if 1 UST is trading above 1.00 USD. Through this system, UST has been able to maintain its peg within a relatively tight range.

USTw Smart Contract Risk: C

Onboarding UST takes on smart contract risk from two sources: the wrapped UST on Ethereum and the UST contract on Terra. The Terra codebase has been extensively reviewed.

The wormhole Terra contracts have been developed by Certus One (part of Jump Crypto) and audited by Kudelski. The wormhole v2 contracts are in active development.

The wormhole Solana/Ethereum/Polygon contracts have gone through sufficient use, transferring a variety of assets cross chain. For reference, there have been 8500 Solana transfers on the Wormhole V1 contracts and 650 on the V2 contracts.

USTw Market Risk: B

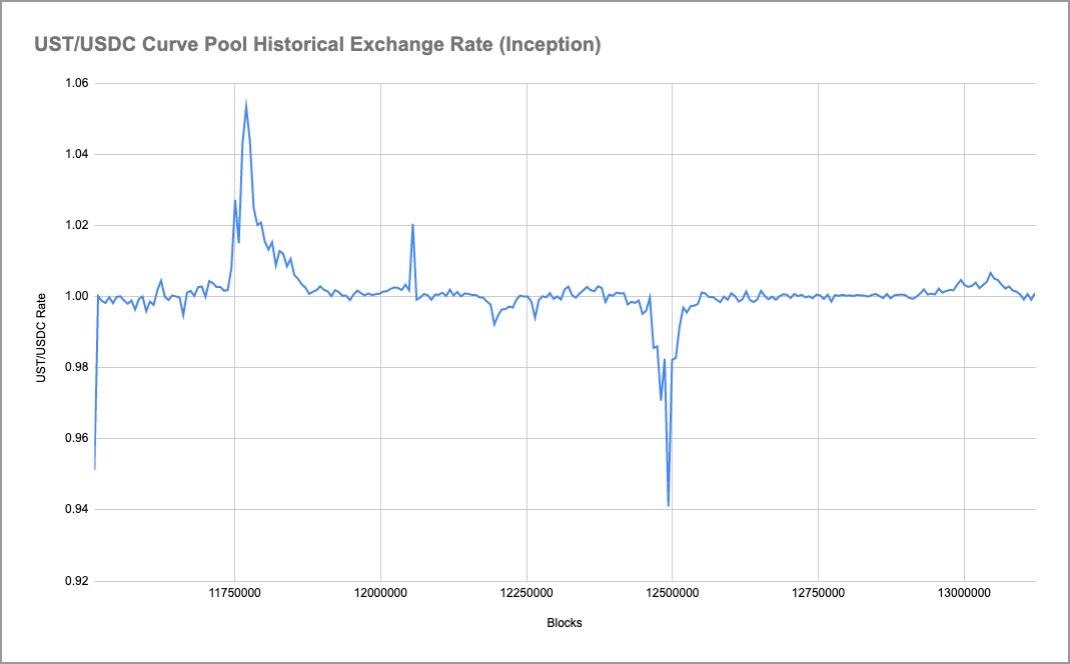

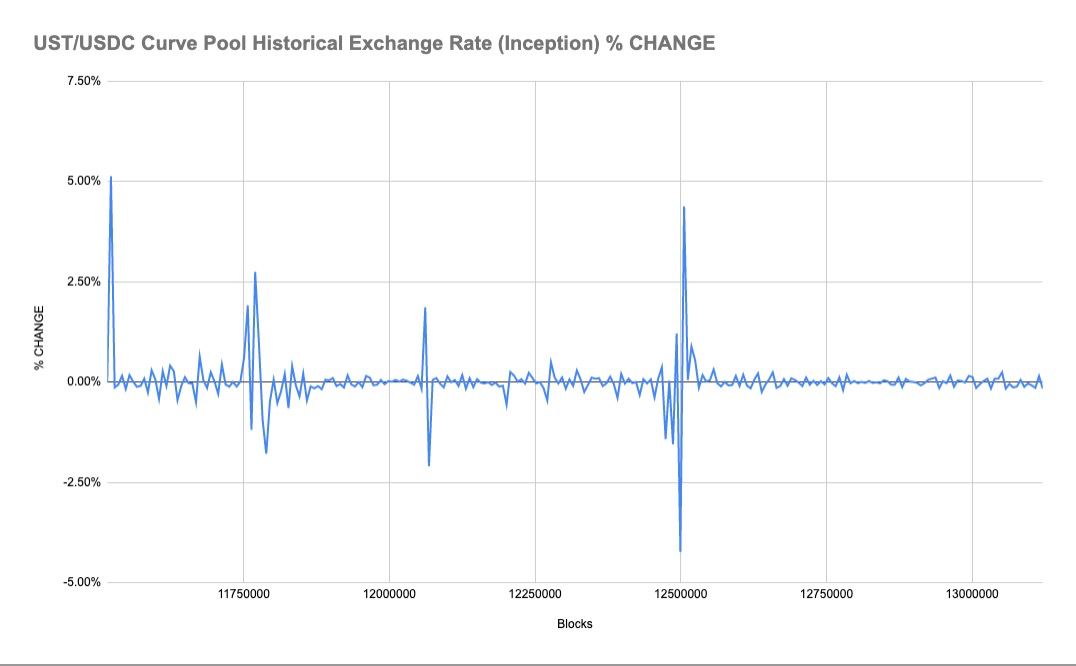

The peg mechanism does have a possibility of failure - the most apparent case would be in a flash crash / extreme market downturn. However, we analyzed the UST Curve Pool from December 23, 2020 and observed that UST has generally stayed within an acceptable range. Simulating 50,000 UST → USDC swaps over our time range, outside of three past outlier events (where UST was +5%, +2%, and -6%), UST has almost always been within a very close range to USDC on a 50,000 unit swap basis.

USTw Counterparty Risk: C+

Since Wormhole has recently added USTw, it has a small number of holders (38). However, with the centralized Terra bridge being retired, users will need to use the Wormhole bridge to move assets back over to Terra. 85% of the tokens are being held in the protocol owned Shuttle->Wormhole pool, which will distribute naturally as the 20,000 holders of wUST migrate over. Another 11% of the USTw tokens are held in a Curve contract to bootstrap liquidity.

Proposed Risk Parameters:

- Strategy: rateStrategyStableTwo

- Base LTV As Collateral: 0

- Liquidation Threshold: 0

- Liquidation Bonus: 0

- Borrowing Enabled: true

- Stable BorrowRate Enabled: false

- Reserve Decimals: 18

- Reserve Factor: 2000

Rationale

To mitigate concerns, a 0% collateral factor will allow UST to be supplied or borrowed - not used as collateral. This limits risk for Aave and its users in other markets. As the wormhole contracts continue to be used and UST gains further adoption, the collateral factor can be increased.

We welcome feedback on these parameters.