Acknowledgements

Thank you for the initiative, hard work, and thought that went into this post! The relentless pursuit from – Chaos Labs, Llamarisk, Karpatkey, Tokenlogic, Certora, Catapulta, Aave Chan Initiative (ACI), Bored Ghosts Developing (BGD), and Aave Labs – to continue Aave’s position as a keystone DeFi primitive is refreshing to see in the industry.

Blockworks Advisory Introduction

As first time posters, we at Blockworks Advisory would like to briefly introduce ourselves. Blockworks Advisory integrates curated and tested expertise from Blockworks Research to deliver deep actionable insights rooted in theory and data. We utilize our distribution, conviction, and native understanding of crypto to collaboratively foster on-chain growth for protocol teams, communities, and DAOs.

We have been following AaveDAO closely as of late, specifically as it relates to the Aavenomics proposal, and would like to offer another solution that we believe the DAO should consider to further deepen Aave’s moat.

Key Points

- Token Repurchase Risks: Aave has grown significantly, but AAVE’s price-to-earnings multiple has risen from 15–20x to over 30x. Buying back tokens at this higher valuation halves the treasury’s purchasing power compared to when the buyback was first proposed, raising concerns of overpaying and undermining future strategic spending.

- Raydium Case Study: Raydium’s indiscriminate buyback at a lower P/E (5–15x) has led to $82M in unrealized losses and missed opportunities to bolster its competitive moat. By allocating treasury reserves to buybacks instead of reinvesting in innovation, competition, or other strategic priorities, Aave potentially lowers barriers for competitors seeking to capture market share.

- Aave DAO As Lender of Last Resort: Building trust in a public credit system requires an efficient liquidation engine and sufficient reserves. The DAO must weigh whether diverting funds toward buybacks weakens Aave’s potential to become the strongest credit system in DeFi and secure Aave’s long-term competitive advantage.

Suggestions

- As an alternative use of accumulated treasury funds, explore protocol-owned liquidity in Umbrella with Aave DAO using revenue to backstop protocol solvency.

- The Treasury Committee should be price-sensitive to the market price it is willing to pay to buyback AAVE tokens.

AAVE Token Repurchase Concerns

On July 24th, 2024, the introduction of AAVEnomics TEMP CHECK announced the AAVE buyback program. Since the introduction of this proposal, Aave has executed on all fronts:

- Deposits grew from $20B to $27B

- Active Loans have grown from $8.2B to $10.4B

- GHO supply eclipsed 200M

- Treasury balance exceeded $100M

At the TEMP CHECK introduction, AAVE tokens were traded at a historically low P/E of 15-20x. Since then, the AAVE token has been traded quite favorably, rising over 300% later in 2024 and residing at 90% higher in Q1 2025. Given the rise in the token value, the P/E has expanded to 32x, hitting as high as 40x. An elevated valuation adds risks to a buyback program should tokens be reacquired at unfavorable prices. Concretely, if treasury funds are used to repurchase AAVE at these prices, the DAO is effectively getting ½ as much AAVE for the same $1 from the treasury than what would have been received in July when the TEMP CHECK was first introduced.

The concern is that the eight-month delay between TEMP CHECK and ARFC telegraphed intent to repurchase AAVE at market price. If Aave continues with an indiscriminate repurchase strategy, market participants who used the gap to sizably position themselves before the ARFC will sell to AAVE for favorable liquidity at an elevated multiple to Aave.

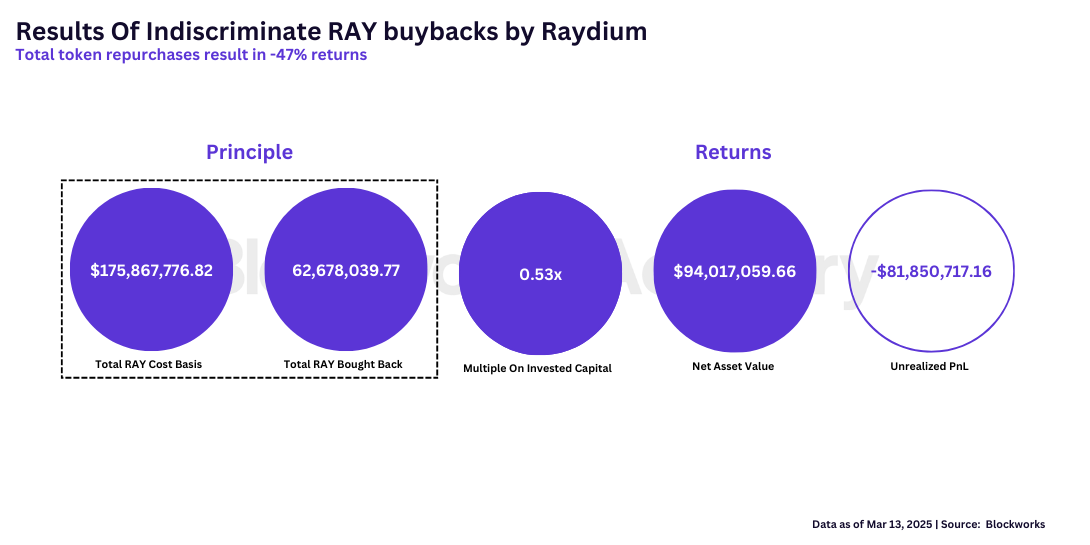

Raydium serves as a valuable case study on the risks involved with buying back tokens indiscriminately of the market price. On the Raydium DEX, 12% of swap fees are used to repurchase the RAY token at any market price.

While this is an attractive strategy to create buy pressure on RAY and return value to token holders, the RAY token declined dramatically after news of pump.fun testing their own AMM. Tangentially, once a buyback program is started, it must continue or else risk signaling weakness to the market. One must wonder if Raydium used the $175m in repurchases to expand its moat and product offering, would it have been so exposed to a single vendor leaving?

In a competitive dynamic industry, being the current regionally dominant protocol is not enough to continue regional dominance in the future. Today, Raydium’s unrealized loss from RAY repurchases since the start of 2024 is ~$82M. The risks of using revenues to indiscriminately repurchase tokens is two-fold:

- It boldly states that the protocol does not exist in competition

- It implicitly admits that this revenue can not be used elsewhere to secure the long-term moat

In contrast to AAVE’s multiple, Raydium’s buybacks occurred within a P/E range of 5x-15x – 50% cheaper than the current valuation of AAVE.

The cognizant reader may acknowledge that the $26 million buyback program represents 23% of current treasury reserves but – assuming revenue rhymes with Q1 2025 average daily revenue – comprises 14% of forward six-month reserves plus current reserves. Notably, the justification for current expenditures should not reside in the expense’s relative percentage of total retained earnings but instead in the business’s forward-looking competitive positioning relative to the market at large.

Accordingly, the share of revenue does not matter. Importantly, what matters is whether Aave DAO feels like it has no competition and has secured the long-term competitive advantage of the protocol. If the answer is no, then it should focus on spending these resources on strategic initiatives that will. A recent example is the Fluid Alignment initiative that leverages Aave’s healthy cash position to its strengths - strategically diversifying its treasury (and revenue streams) through purchases of innovative DeFi protocol tokens. There are likely multiple protocols that AaveDAO may want to consider aligning with that offers complimentary products and can further deepen Aave’s moat.

Precedent For AAVE DAO As Lender Of Last Resort

To uphold and maintain faith in Aave protocol’s public credit system, Aave DAO has historically been the Lender Of Last Resort (LOLR) with Marc Zeller stating, “The few excess debt events in Aave protocol history have been addressed by governance through the mobilization of “cash” DAO treasury funds” (Aavenomics TEMP CHECK). The past precedent implicitly affirms that Aave DAO is willing and able to clear bad debt.

Historical precedent further serves to illustrate the widespread acceptance of fractional reserve systems to backstop public credit. Reserve systems operated by banks and governments to secure liquidity and make potential bank-run events less impactful have existed for decades. One example is the designated reserve ratio (DRR) for FDIC, which holds 2% of the aggregate collateral banks lend against.

Blockworks Advisory’s Primary Suggestion

Aave DAO should consider using the previously allocated portion of the treasury for token repurchases to be the lender of last resort (LOLR) for Aave protocol. In doing so, institutional borrowers would receive higher assurance on protocol solvency, and Aave would solidify itself as the risk-minimized solution for all on-chain lending. No other public credit system in DeFi could compete against this, and Aave would provide for its long-term moat.

We advise the DAO to explore protocol-owned liquidity in the Umbrella Safety Module as a strategic alternative. This approach offers several key outcomes:

- Free Cash Flow Generation: The Treasury can retain USDC in the main market, generating continuous free cash flow.

- Signal of Confidence: Staking aUSDC in the Umbrella Safety Module demonstrates the protocol’s commitment to, and confidence in, this new mechanism and its credit system.

- Cost Recovery: While the protocol must cover the risk premium for Umbrella stakers, it can recoup a portion of this expense through its proportional share of the Safety Module deposits.

- Low Volatility Position: Historically, losses from bad debt have been minimal. Consequently, the Treasury can earn free cash flow from its aUSDC position, offset expenses for the Umbrella Safety Module, and maintain a stable balance in USDC to support growth initiatives—or to fund AAVE buybacks when valuations are more favorable

Upon Aave adopting such an LOLR system, it could set a reserve rate as a percentage of total borrowed assets to allocate to the Umbrella Safety Module. Once this reserve rate is hit, Aave DAO could use the surplus revenue for other key initiatives or discretionary AAVE repurchase programs.

In the case of using surplus revenue for AAVE repurchases, we would recommend that the Treasury Committee be discretionary and price-sensitive towards the price it is willing to pay to repurchase AAVE from the market – rather than deterministic and price-insensitive.