Pro & Cons of each option for CRV holdings

At the time of writing, Aaveholds 696K units of CRV. This post will recap the different options discussed:

veCRV - Lowest risk, governance and direct control CRV emissions

st-yCRV - High yield, no CRV emission influence and exit liquidity risk

sdCRV - High yield, proportional CRV emission influence and exit liquidity risk

veCRV

Aave is to gain direct governance influence, minimize risk and gain influence on gauge weights to generate external incentives. This option is not optimized for ROI or yield which introduces additional smart contract risk. Llama recommends the veCRV option.

Pros

- Gauge weight power (Influence on CRV weekly emission)

By locking it 4 years and relocking periodically to get the max voting power, the DAO would be able to redirect 0.0068 CRV/veCRV on the pools of its choice (Most likely directed to a GHO one)

With the current emission (reduced every year by 15%) the DAO would control 4,740 CRV of emission per week, representing $234.13K per year obtained without any additional expenses.

- Protocol fees (Profit sharing in 3CRV Stable pool)

50% of all protocol fees on Curve are directed to LPs, and the other 50% goes to veCRV holders. The current APR is 3,43% which is representative of the usual economic activity. With regular volumes, the APR is close to 2-5%, but weeks like USDC depeg, the APR was 15%.

No extra counterparty risk (No protocol on top of Curve)

Unlike the two other options, the CRV will be locked on Curve directly from the Collector contract. This reduces the risks compared to using protocols on top of Curve which adds an additional layer of smart contract counterparty risks.

- Easy management of the veCRV position & votes

Re-locking the veCRV position can be made accessible, via adding a function on the Collector Contract. Llama can then create a bot which automatically calls the function and re-commits the veCRV holding.

The veCRV option only requires to lock CRV, no extra token required.

When a gauge vote is submitted on Curve, there is no need to revote each week even if the position is increased, unless Aave decides to change the vote.

- Additional features from holding veCRV

Governance Power to participate in the DAO decisions (On-Chain)

veBoost which can be sold or utilized to maximize the rewards on the funds deposited: While we agree that the impact will be minimal at first, the veBoost will grow over time with the veCRV holdings, compared to both other solutions where it is lost.

Cons

- 4 unlock period with frequent relock to keep the max voting power

The goal of this strategy is to always relock to have the maximum voting power, and increase the position over time with the CRV earned. If Aave decides to stop this strategy at a later stage, the same amount of CRV that was locked will be available after 4 years.

Llama can automate the relock periodically to avoid the decay.

- Complex participation in DAO decisions

Governance participation can be challenging with the collector contract because of the important amount of DAO decisions voted, and there is no way to delegate the veCRV governance power.

st-yCRV

This option was proposed by Llama as an alternative to veCRV in case Aave preferred maximizing the yield, with the intention of accumulating CRV and gaining additional voting power for a later date.

This option does not offer any governance influence which leads to an easier management.

However, considering the recent events such as USDC de-peg and Euler hack which impacted many protocols, Llama believes that security should be prioritized and Aave should proceed with the lowest risk proposal.

Pros

- Gauge weight power profits (Influence on CRV weekly emission)

While it’s not possible to directly vote with st-yCRV, Yearn utilizes the voting power to vote for the highest vote incentives on the market, then sells everything for CRV and compounds the strategy overtime.

- Boosted protocol fees profits (Profit sharing in 3CRV Stable pool)

Yearn utilize its veCRV holdings to boost the distribution of the 3CRV (Currently 1.66x)

All 3CRV are collected, sold for CRV and compounded overtime.

- Temporary MegaBoost in CRV

As mentioned earlier in this thread, Yearn decided to distribute 30k CRV/Week for a defined amount of time to maximize the yield. These CRV are also compounded in the strategy. Unless the decision is renewed, this should not be taken into account as the initial incentives should end soon.

- Easy management of the CRV position

Requires a deposit & stake to enter the strategy. The yield sources are collected in, or sold for CRV which are automatically compounded in st-yCRV. No further action is required by Aave post-staking yCRV.

Total current APR: 33%

- Transferable Asset (yCRV)

When CRV are deposited on Yearn, it is periodically relocked as veCRV, but the protocol mint yCRV at 1:1. These yCRV can be staked for st-yCRV and transferred or sold on the yCRV-CRV pool on Curve.

Cons

No direct governance influence**

All the gauge weight power and 3CRV are sold for CRV, and the governance power and veBoost are kept by Yearn.

Extra counterparty risk (Yearn on top of Curve)**

This solution adds extra smart contract and counterparty risks as required to trust Yearn as a good manager of the strategy.

High risk asset profile (Depeg risk)**

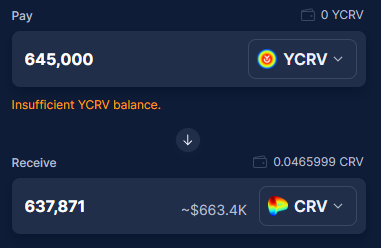

The yCRV is transferable, but the liquidity remains limited: $8.4M.

With the current Aave holdings and yCRV liquidity, it would be possible to exchange 680k yCRV with a rate of 0.9936:1.

However, any selling pressure on the yCRV could lead to Aave incurring significant slippage when trying to exit the position.

sdCRV

sdCRV was proposed by the Stake DAO team in the comments, and presents as an hybrid solution between maximizing yield and governance influence. However, it requires veSDT holdings or boost delegation to Aave to be considered efficient compared to other solutions.

Until recently, the voting power on sdCRV was acquired progressively over a 30 day period. Stake DAO mentioned a parameter change related to asdcrv, but we couldn’t find any vote or public announcement about this update. However, even after this period, the voting power of 1 sdCRV was not equal to 1 veCRV if Aave does not lock SDT itself or receive delegation from veSDT holders.

Pros

- Proportional gauge weight power (Influence on CRV weekly emission)

By depositing 696k CRV on Stake, it would result in a voting power of 0.61 veCRV vote / sdCRV. With the current emission (reduced every year by 15%) the Aave would control 2,891 CRV of emission per week, representing $142.80K per year obtained without any additional expenses or veSDT boost holdings or delegation.

To avoid a SDT acquisition and reduced voting power, Marc Zeller from ACI is to delegate all his veSDT voting power (270k) to Aave for one year, as well as relocking & re-delegating every week enabling Aave to retain the provided boost.

Other parties mentioned on the forum said that they consider to delegate, but no one other than ACI confirmed that they will delegate, relock & redelegate frequently or disclosed their holdings to track the delegation, so it’s not taken into account in this recap.

According to AaveChan engagement, the veSDT holding delegation would boost the voting power to 1.14x for 1 year.

With the current emission (reduced every year by 15%) the DAO would control 5,403 CRV of emission per week, representing $266.9K per year obtained with 270k veSDT boost delegated. However, as soon as the delegation is over, the voting power will be back to 0.61x.

- Proportional protocol fees (Profit sharing in 3CRV Stable pool)

Same as on Curve, the 3CRV fees are distributed to sdCRV stakers.

- Transferable Asset (sdCRV)

When CRV are deposited on Stake DAO, it is periodically relocked as veCRV, but the protocol mint sdCRV at 1:1. These sdCRV can be staked for sdCRV-gauge, transferred or sold on the sdCRV-CRV pool on Curve.

Additionally, the Stake DAO team communicated that the votes now operate like veCRV. Please note, Llama has not been able to publicly find this announcement beyond this forum thread.

Cons

- Extra counterparty risk (Stake on top of Curve)

This solution adds extra smart contracts risks, similar to st-yCRV with additional counterparty risk through reliance on ACI and/or others to provide delegated veSDT support. This veSDT support requires weekly relock and redelegation to avoid impacting the boost.

As Aave’s CRV continues to grow in line with Aave revenue, additional veSDT delegation will be required to maintain the maximum boost. Llama does not question ACI’s dedication to Aave. After the initial committed 1 year period, Aave will receive reduced voting power if an alternative veSDT delegate is not found.

- High risk asset profile (Depeg risk)

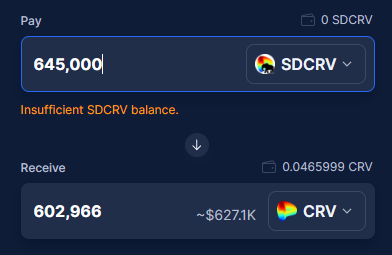

The sdCRV is transferable, but the liquidity remains limited: $3.8M.

With the current Aave holdings and liquidity, it would be possible to exchange 680k sdCRV with a rate of 0.9826:1.

- Management of the rewards

Considering that Aave will vote for pools with no vote incentives have decided on the Curve pools, Aave would not earn part of the yield disclosed on the UI.

Moreover, all rewards from vote incentives are sold for SDT and distributed. If Aave is to accumulate a CRV holding over time, the SDT tokens would need to be swapped to CRV.

- No veBoost (Kept by Stake DAO)

Same as Yearn, Stake DAO would keep the veBoost to maximize the yield on their strategies.

Next Step

Llama will be creating a Snapshot vote presenting the following options to the community:

YAE - veCRV

YAE - st-yCRV

YAE - sdCRV

NAE

ABSTAIN

We expect the Snapshot to go live 27th March 2023.