Hey @Pauljlei thanks for feedback. We agree to split the proposal in two and start the ETH borrow pause snapshot as early as possible.

As explained in our analysis, the higher rate curve for ETH has many tradeoffs, specifically because of stETH/ETH recursive leveraged positions. We are aware that a higher rate might put additional pressures on these positions to unwind and this is why we proposed to increase the rate only after kink.

Let’s assume ETH borrow gets disabled but ETH supply withdrawals start to occur for some reason and utilization starts increasing towards 100%. Speculators borrowing ETH to gain yield on ETHPoW fork are potentially prepared to carry up to 3% cumulative cost, assuming the forked ETHPoW may be trading at 0.03-0.04 ETH (currently on Poloniex). The same max cost would be then also carried by stETH/ETH recursive positions. These users are probably counting on successful merge and the current 3% stETH discount to improve. Assuming this, we believe the negative APY impact for stETH/ETH positions is quite limited.

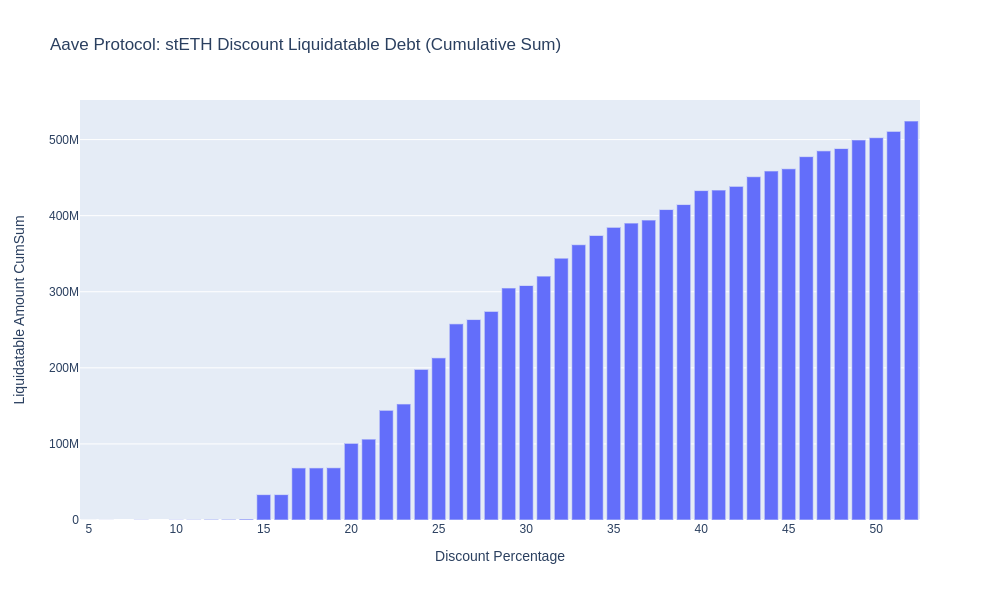

But, we could also have a situation where ETH market utilization increases over 70% and stays there for a longer duration of time. This would be unrelated of ETHPoW positions, but because of some longer lasting run on ETH deposits. The cumulative cost for stETH/ETH positions could reach over 3% and here some users might start to break and unwind. The question then becomes how much stETH selling could we witness until the utilization improves back below 70% where APY becomes positive again. There is around $800m ETH borrowed right now and at a potential 80% utilization it means we’d be seeing around 65k stETH sold to repay ETH borrow (about 33% of the curve stETH/ETH pool) in order to get back below 70% level. This pushes the price of stETH from 0.970 to 0.955 ETH, which has almost no impact on cascading liquidations. In the worst case scenario of 100% utilization and current borrow market size, we’d need to see about 160k stETH sold and ETH repaid (again to get back to 70% ETH utilization) which pushes stETH price to 0.91. As much as 10% depeg sounds devastating to stETH/ETH positions, most of them are well collateralizated (see chart below and note that this chart doesn’t assume partial liquidations so liquidated amounts would be much smaller).

Another concern of high ETH utilization is that in an extreme case where large amount of stETH liquidity is pulled from Curve or Balancer, the liquidators wouldn’t be able to source enough on-chain liquidity to liquidate stETH/ETH recursive positions. Therefore it might be better to rely on users unwinding prior to such event.

TL;DR is that we see risk of high ETH market utilization and its impacts higher than the risk of having stETH/ETH positions unwound by users due to potentially high negative APY caused by higher rate, where impact on cascading liquidations is limited. This is why a higher rate at 100% utilization was proposed. However we believe ETH borrow pause alone should hopefully be enough to prevent high utilization of ETH market. If there is an evidence of ETH supply dropping, we would advise to increase rate at 100% immediately.