Hey all,

Block Analitica recently received a grant from the Aave Grants DAO for building the Aave Analytics Dashboard. The dashboard is currently in the second stage of a three-part development plan. More information is available on the Aave Grants DAO website. Block Analitica believes that the Aave Analytics Dashboard can provide useful tools and data that may help the decision-making process of Aave governance. This process can be described as “Computer Aided-Governance”. The dashboard is intended to be used to make better-informed decisions by enabling a high-level view of the Aave v2 protocol on Ethereum.

This post highlights certain risks that Block Analitica has identified as it relates to Aave v2 on Ethereum and the upcoming Proof of Stake (PoS) merge. These risks are derived from and illustrated by data from the Aave Analytics Dashboard. Finally, this post includes a potential mitigation strategy and proposed parameter changes to the ETH market on Aave v2 on Ethereum.

Background

@monet-supply from our team already made a great overview of Ethereum merge risks for MakerDAO. After some discussion, we realized that lending markets such as Aave and Compound face much greater risks. Most tokens, excluding ETH, will likely be worthless on an ETHPoW chain. Hence, one strategy users may employ to maximize their cryptoasset holdings, will likely be to borrow as much ETH as possible, collateralized mainly by stablecoins or other tokens. In addition, we should probably also observe flows from stETH holders to ETH, since stETH will likely also be worthless on an ETHPoW chain.

Supported Data

Speculative strategies related to the PoS merge and the potential ETHPoW fork will likely have implications for Aave, particularly because Aave enables ETH to be borrowed from stETH. stETH collateralised ETH borrowing has become a popular strategy and has increased ETH market utilization to a level of 62% at the time of writing. A majority of ETH borrowed is currently collateralised by stETH.

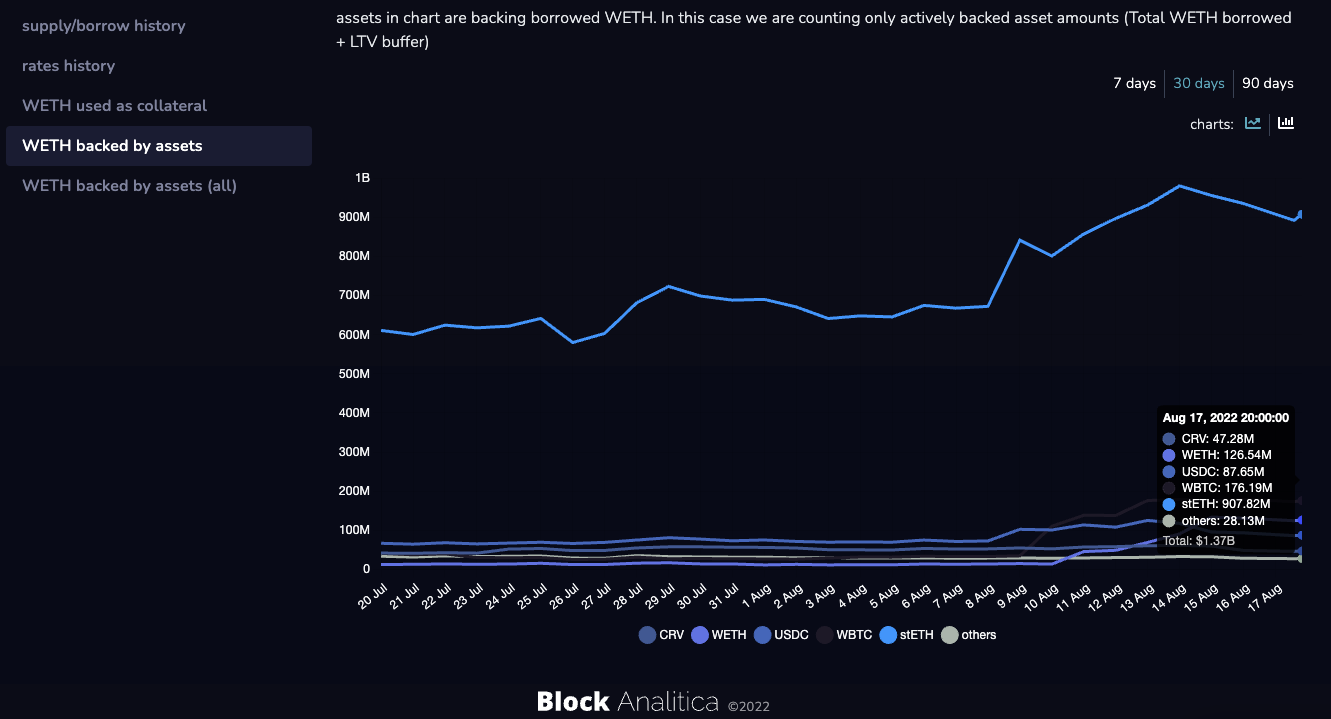

As illustrated in the chart below, large part of ETH that is currently borrowed is collateralised by stETH (approximately $907 million in stETH collateral is backing ETH, represented as the dollar-denominated ETH amount borrowed from stETH divided by the LTV ratio). The stETH depeg situation recently improved as a result of the merge date prediction which, in turn, led to the stETH/ETH recursive position strategy to regain popularity and grow in size.

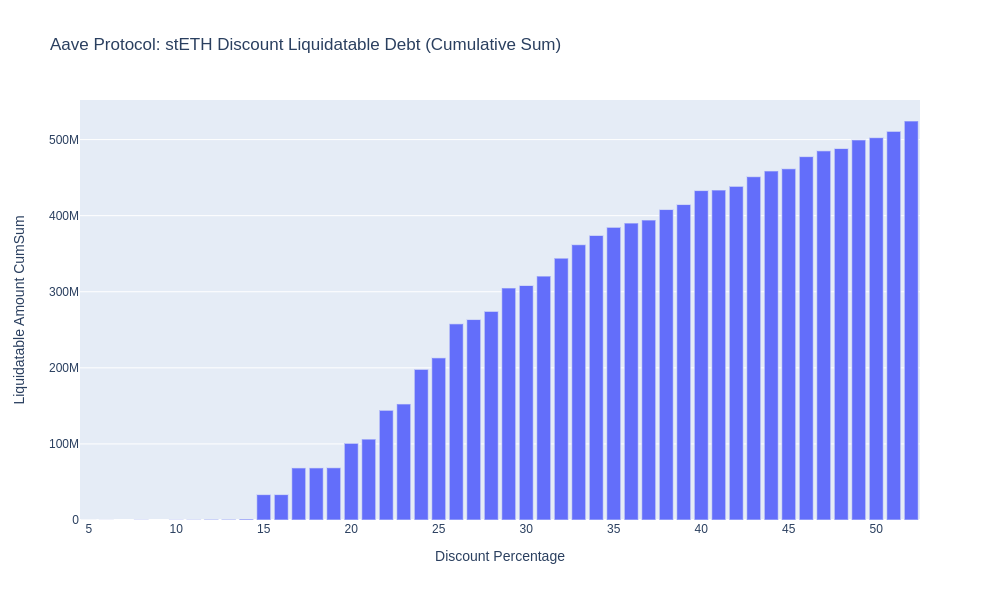

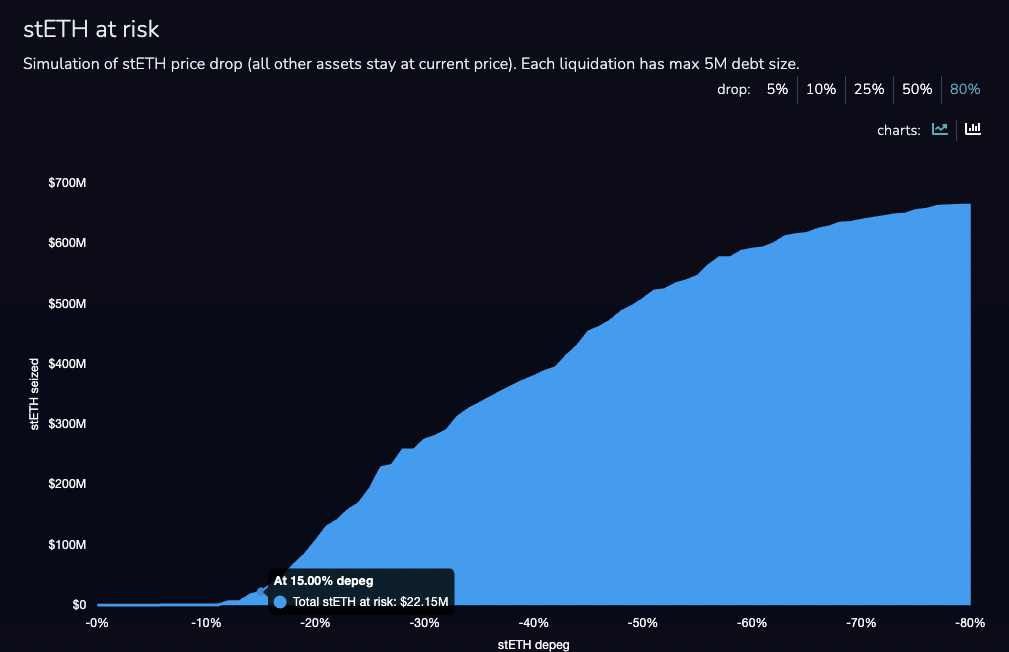

Luckily, stETH/ETH positions maintain a high buffer. A discount of stETH to ETH would need to reach around 15% to start experiencing larger liquidations. Further information is provided in the chart below. Note that the chart assumes a partial liquidation scenario in chunks of a maximum of $5 million, until the position health ratio is improved, which is based on empirical data of Aave liquidations.

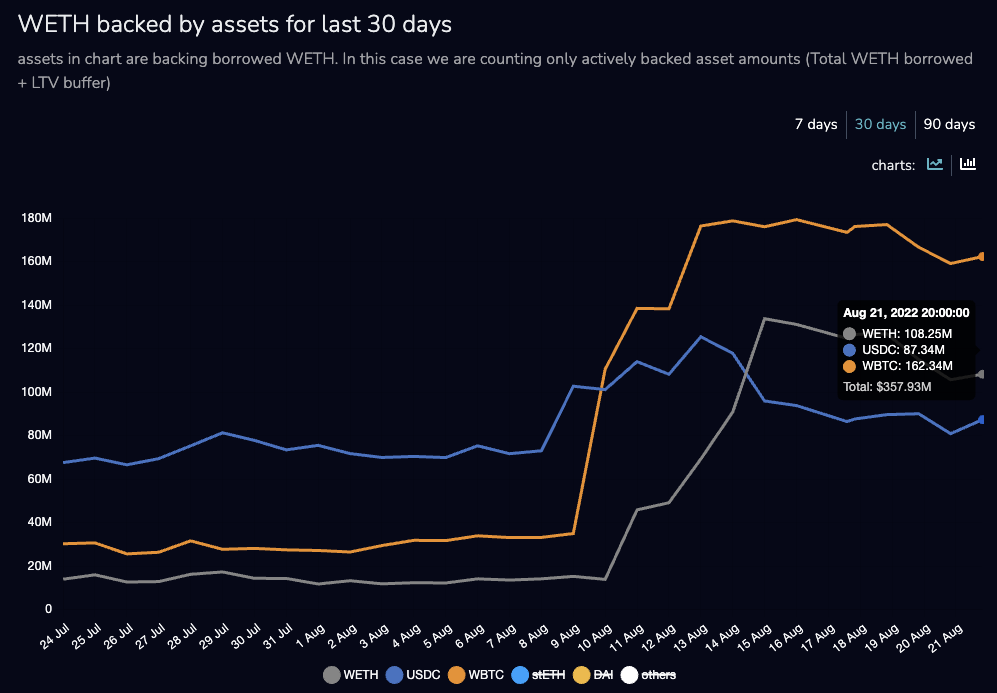

Examining the chart of collateral backing borrowed ETH in more detail (see chart below), reveals another potential issue that may arise: ETH is increasingly being borrowed and collateralized by other, non-stETH assets, such as USDC, WBTC, or even ETH itself. The value of non-stETH collateral for ETH borrowing has increased from $120m to $390m in the last 10 days. This trend suggests that our hypothesis about the ETH market becoming increasingly utilised up until the merge is correct.

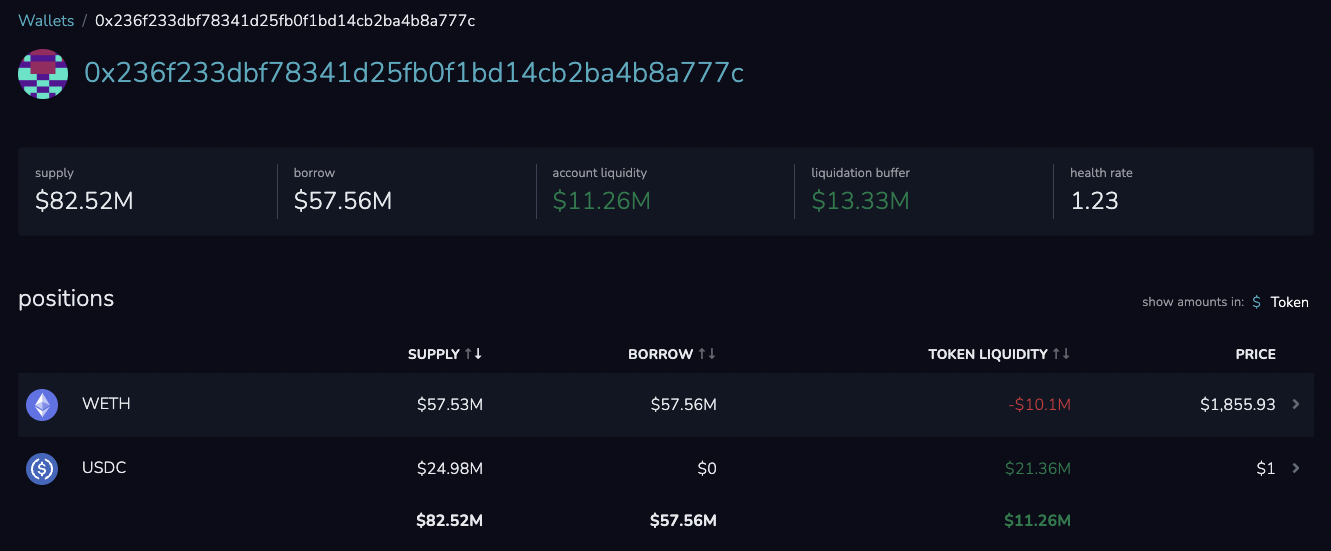

By studying individual Aave wallets and strategies through the Aave Analytics Dashboard we noticed an unusual behaviour of users building ETH/ETH recursive positions. There are at least two larger wallets that we have identified. The screenshot below includes an example of one such wallet. This strategy enables ETH holders to maximize their ETH that will be redeemable on an Aave ETHPoW fork. However, this strategy might not work since ETHPoW intends to freeze aWETH contract.

Risks

So what could go wrong? We have identified three main risks related to the ETH market becoming increasingly utilized:

High ETH utilization potentially makes liquidations harder or impossible

In a situation where the ETH market becomes heavily utilized and markets start experiencing high volatility as a result of the merge event, liquidations of regular ETH long/stablecoin short positions might not be possible. This will be due to the fact that liquidators will not have access to ETH as collateral since the majority of ETH will be borrowed. This could in turn lead to some positions becoming uncollateralized. Note that because people are now building stablecoin long/ETH short positions, a price increase in ETH could also start liquidating stablecoin collateral, which will be less of an issue, but still something to be aware of.

High ETH utilization increases the ETH rate to a level where stETH/ETH positions are making negative APY

Once the ETH borrow rate reaches 5%, which happens shortly after 70% utilization rate (we are at 63% right now), stETH/ETH positions start becoming unprofitable. Currently, borrowers on Aave are not leveraged maximally due to depeg risks. As a result, it is possible that some positions will have their APY negative much earlier. This will cause users to unwind their positions up until the ETH borrow rate reverts to a stable level where the APY becomes tolerable. This means that we would see a lot of stETH to ETH redemptions and in turn a downward push on the stETH price, which will already be under pressure due to regular stETH holders switching to ETH to gain upside on ETHPoW work. All of this can lead to a downward price spiral of stETH which can create cascading liquidations at Aave. Hopefully people start bidding stETH at a not-too-large discount, which is more likely now that the merge timeline is clearer.

Already high ETH utilization causes regular ETH suppliers to start withdrawing their ETH

As a result of the uncertainty and risks related to the ETHPoW fork and PoS merge in general, and ETH utilization on Aave in particular, current liquidity providers may become increasingly worried about their ETH on Aave, and in turn, may withdraw ETH on the supply side. The utilization rate could increase unrelated to ETH borrowers,. Also, if ETH price drops then ETH long/stablecoin short positions will likely need to be deleveraged by selling supplied ETH. In such a scenario, the ETH utilization would increase even further. One of the ETHPoW Twitter accounts is also already calling everyone to withdraw assets from lending platforms, which could create additional pressures on high ETH market utilization.

Potential Mitigations

Based on our views of the various risks related to the PoS merge and potential ETHPoW fork, we recently proposed changes to the ETH Interest rate model at Compound, including setting ETH borrow cap to 100.000. To our knowledge, Aave v2 does not have the capability to limit ETH borrowing to a specific number, but it has the option to disable borrowing. As much as this sounds like an overreaction, we believe that Aave should freeze ETH borrowing in the interim period leading up to the merge.

However, this action alone might not be enough. As previously illustrated, a high utilization rate of the ETH market could in fact increase unrelated to ETH borrow dynamics. Therefore, a more aggressive interest rate increase for the ETH market is proposed. However, this will create certain tradeoffs. A higher ETH borrow rate would force stETH/ETH recursive positions to be closed, potentially worsening the stETH depeg situation. On the other hand, the discount would need to be severe (15%+) to cause liquidations in the tens of millions of USD value.

In our view we believe that a more aggressive rate curve should be implemented, since the potential ETH borrow freeze might not be enough to prevent high market utilization. Ideally, the new curve should not affect the current stETH/ETH positions and cause massive unwinding. Therefore, a steeper slope is only proposed for the part of the ETH rate curve after the kink. Instead of a 103% rate at 100% utilization, we propose to set it to 1,000%.

In conclusion, the following parameter changes to the Aave Ethereum v2 ETH market are proposed in the interim period leading up to the merge:

1) Freeze ETH borrowing.

2) Increase the variable borrow APR at 100% utilization from 103% to 1,000%.

AAVE Payment

If this proposal is adopted, a one-time payment of 60 AAVE will be transferred from the Aave governance to the MakerDAO pause proxy. This is intended to compensate for Block Analitica’s research and development costs in connection with this proposal. BA provides risk management consulting services to MakerDAO as the Maker risk core unit.

Transfer 60 AAVE to 0xBE8E3e3618f7474F8cB1d074A26afFef007E98FB