This post was part of the Delphi Daily released today, in which I introduced this ARC to our community of readers and shared my take on it.

Given that the main role of the SM within the Aave ecosystem is to serve as an insurance fund in case of a shortfall event, it is obvious why slashing is necessary; without it, the SM would serve no function. Thus, my comments will focus on the more nuanced second point of the ARC: introducing BPT to the SM. Concretely, I will argue why this ARC is a first step towards making the SM more robust and better suited to handle shortfall events.

Let’s first speculate on what a shortfall event could mean for the price of AAVE. As I see it, there could be three main drivers of price action given a platform deficit (the numbering doesn’t imply chronological order):

-

Price gets hit as trust in the platform is questioned. Selling within this group would be more long-term and fundamentals oriented from investors that get disenchanted with the brand.

-

Price declines as sellers try to front run selling from group 1, the upcoming liquidation event of the SM and potentially the minting (and selling) of new AAVE tokens if the SM can’t cover the whole deficit.

-

As price declines because of the previous points, a higher share of the SM needs to be liquidated to cover the losses of the shortfall event. This can even get to the point where the SM can’t cover the losses and additional minting and selling of AAVE tokens would be required.

The most dangerous aspect of the previous scenario is that a vicious cycle can emerge from the dynamic between points 2 and 3. As price declines as a product of points 1 and 2, a higher share of the SM needs to be liquidated, which in turn can exacerbate more selling from group 2, which would imply that an even higher share of the SM would need to be liquidated and so on (see next figure). The higher the share of AAVE held by the SM, the more powerful this dynamic can become.

Figure 1. Shortfall Effect on Price.

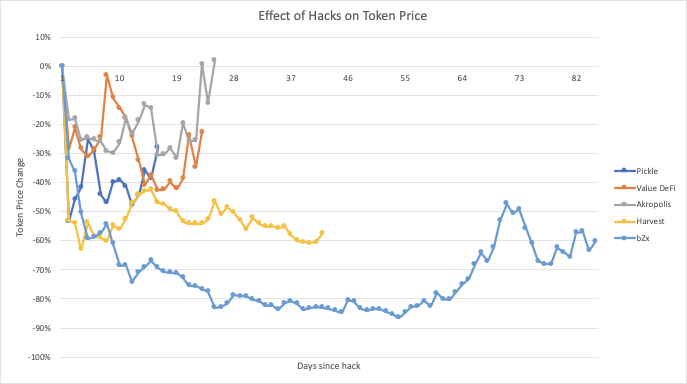

Even though it is impossible to estimate what the precise effect on price a shortfall event could have on AAVE, we can look into the recent past for some hints. The next figure shows price evolution from different DeFi projects since they were hacked. Two important facts are worth noting from that graph: 1) Token prices have been aggressively hit (-18 to -53%) immediately following the hacks; and 2) Some tokens are able to recover over time. An additional point worth noting here is that none of these protocols had native token backed insurance funds (as the SM); as such, the price impact of a shortfall event on AAVE could be greater.

Figure 2. Soure: Data from Coingecko. Calculations my own.

Considering the above, a useful liquidation mechanism could be put in place whereas, given a shortfall event, the SM liquidation would happen gradually over a predetermined period of time. This would mitigate the reflexive dynamic pointed in Figure 1 and would also potentially allow AAVE price to recover before starting to liquidate the assets.

As was pointed before, the higher the share of AAVE within the SM, the more powerful the reflexive dynamic in Figure 1 becomes. In this sense, another mechanism that could help mitigate that dynamic is adding other assets to the SM (this is where the BPT introduction comes into play). The best assets suited for this purpose would be assets with low correlation to AAVE and low volatility. Low correlation with AAVE is needed because, as correlation rises, real diversification from adding a new asset declines. In other words, adding highly correlated assets to the SM would virtually just mean keeping it 100% in AAVE. On the other hand, low volatility is needed so that the value of the SM doesn’t aggressively change over time. Let’s explore how ETH, which is the second asset proposed to be part of the SM, behaves for these two metrics.

First, let’s consider ETH and AAVE correlation. The correlation coefficient between these two assets stands at 0.56, which implies low to moderate correlation. The following graph shows a plot of the logarithmic return correlation between these two assets.

Figure 3. Data from Coingecko. Calculations my own.

As was mentioned before, a good asset to be added to the SM should have low volatility. The following graph shows the 30-day volatility of ETH (red) versus AAVE (green). What’s clear from that graph is that ETH has experienced consistently lower volatility than AAVE for most of the examined period.

Figure 4. 30-Day Volatility. ETH (red) and AAVE (green). Source: Coinmetrics.

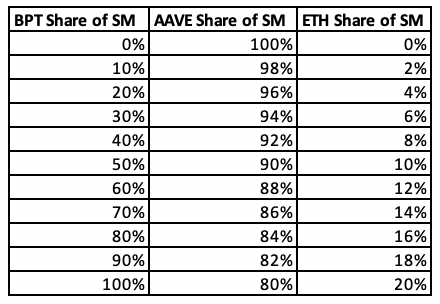

Putting the above together, ETH is an asset that presents low-to-moderate correlation to AAVE and consistently lower volatility. Thus, I consider its addition to the SM a positive step towards making the SM more robust (and less reflexive). And I say a step because even with this addition the SM will still be highly exposed to the price of AAVE. The next table shows how the AAVE and ETH shares of the SM evolve as the share of the BPT in the SM increases. As can be seen, even at 100% BPT share of the SM, it’s still 80% AAVE overall.

Table 1. AAVE and ETH Share of SM vs. BPT Share of SM.

The 80/20 AAVE/ETH BPT design decision, however, was made taking other additional factors into consideration. One of those factors is protecting stakers from impermanent loss and allowing them to still be highly exposed to AAVE – that’s in part why the 80/20 decision was made. As the share of ETH in the BPT increases, stakers would be less exposed to AAVE and more exposed to impermanent loss.

If DeFi has taught me anything, it’s that every design decision comes with tradeoffs. In this case, the tradeoff of the 80/20 Balancer Pool is between diversification (as the share of ETH increases, diversification of the SM increases) and staker incentives (as the share of ETH increases, stakers are less exposed to AAVE and more exposed to impermanent loss). In this sense, I think the 80/20 design decision strikes a good balance between SM diversification and staker incentives.

Let me conclude by saying that this ARC (if passed) marks the beginning of the journey for Aave’s Safety Module. On one hand, it introduces slashing, which underpins the main functionality the SM serves. On the other hand, it introduces a BPT 80/20 AAVE/ETH as a new asset backing the SM – making it more robust and better suited to serve its purpose. As I’ve argued in this piece, I welcome these developments for the SM and look forward to the next evolutions of this critical piece of infrastructure within the Aave ecosystem.