aip: TBA

title: Round 5 Liquidity Mining Aave v2 Ethereum Market

status: Proposal

author: Governance House - @MatthewGraham, 3SE Holdings

created: 03/06/2022

Simple Summary

This Arc presents the community with the opportunity to reinitiate stkAAVE incentives on the Aave v2 Ethereum market for a 90 day period upon execution of this proposal.

stkAAVE rewards are to be provided to Users who borrow selected stablecoins and lend selected assets.

Abstract

Liquidity mining incentives were introduced to Aave v2 on the 26th April 2021 via AIP-16, renewed by AIP-32, reduced by 30% with AIP-47, reduced by 30% with AIP-60 and are to be reduced by a further by 20% with this proposal.

A summary is shown below.

- AIP-16: 2,200 stkAAVE per day from 26th Apr 2021 on Aave v2 Ethereum market

- AIP-32: 2,200 stkAAVE per day from 24th Aug 2021 on Aave v2 Ethereum market

- AIP-47: 1,540 stkAAVE per day from 22nd Nov 2021 on Aave v2 Ethereum market

- AIP-60: 1,078 stkAAVE per day from 21st Feb 2022 on Aave v2 Ethereum market

- AIP-X: 862.4 stkAAVE per day upon implementation of AIP on Aave v2 Ethereum market

Continuing with the trend of refining how incentives are distributed across the market to focus on encouraging borrowing demand on selected Stablecoins, USDC, DAI, USDT and FEI, along with lending ETH.

The inclusion of FEI recognises the contribution of the Tribe DAO community for providing lending and borrowing incentives upon listing. Through this proposal, we can encourage other communities to bootstrap their token listing with incentives.

Motivation

This proposal continues on from AIP-60 with a further 20% tapering of incentives and shall last for another proposed 90 day period. The refined rational within this proposal is presented below:

- Continue to reduce the quantity of stkAAVE being distributed over time.

- Encouraging borrowing of stables with the expectation that borrowing demand will attract lenders.

- Recognise the contribution of partners who provide incentives upon listing a new asset.

- Attract ETH as collateral.

By subsidising borrowing costs with stkAAVE incentives, it is expected that the resulting borrowing demand will generate sufficient yield to entice Users to deposit stablecoins into the lending market to earn yield.

With the recent growth in borrowing demand for ETH and with the expectation other staking derivatives like stETH are to be added to the market in the future, this proposal seeks to grow the supply of ETH in the market. ETH is also the second highest contributor to the market’s AUM behind stETH.

The following more broader objectives of this proposal are as shown below:

- Grow Total Value Locked (TLV).

- Increase liquidity.

- Attractive (low) borrow rates.

- Increase the protocol income via growing the Reserve Factor.

- Redistribute governance power towards Users of the platform.

Specification

The below section outlines the proposed liquidity mining incentives to be applied to the Aave v2 Ethereum market.

Key changes from the previous liquidity mining campaign are summarised below:

- stkAAVE being distributed is down 20% from 1,078 to 862.4 per day

- Borrowing of stables is subsidised

- Lending of ETH is subsidised

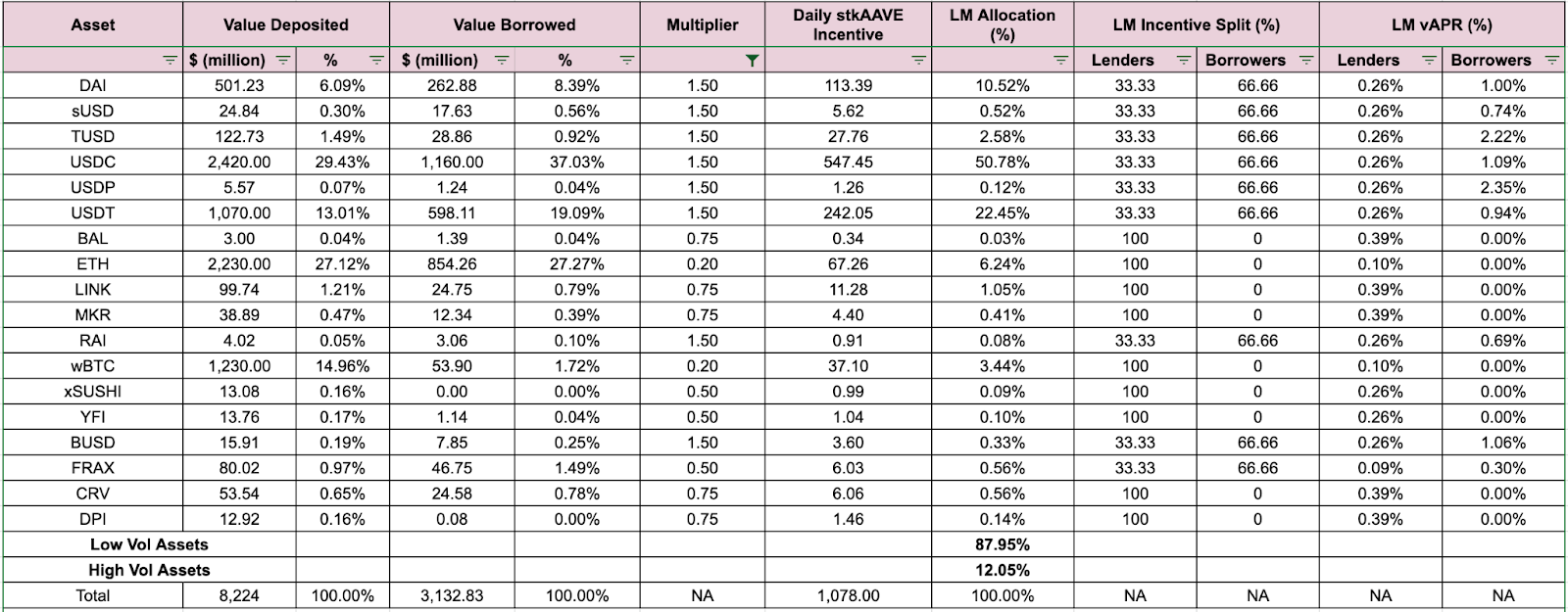

The table below shows the intend stkAAVE distribution across the Aave v2 Ethereum market asset listings. In estimating the Borrowing vAPR, existing borrowing demand was used.

Note: TVL per token is as per the 28th May 2022.

Discussion

This proposal continues the trend of refining the distribution of stkAAVE to be more closely aligned with revenue generation. The Aave v2 market generates revenue from Users who borrow funds. The most commonly borrowed assets are stablecoins and the majority of the DAOs revenue is nominated in stablecoins. By subsidising borrowing costs, it encourages Users to borrow stablecoins and this generates revenue for Aave DAO.

For further details on Aave v2 Ethereum market revenue, please see @llama’s financial reports.

The previous proposal, if implemented with no changes would lead to the following distribution of stkAAVE across the market.

If 1,078 stkAAVE was distributed as per the prior liquidity mining proposal, assuming a price of $95 per stkAAVE, then the vAPR on lending and borrowing is as shown above. This would cost an estimated $9.22m over a 90 day period.

This proposal reduces spending by 20%, with 1,078 stkAAVE reduced to 862.4 or from $9.22m to $7.37m. The borrowing vAPR from incentives on stablecoins are very similar for DAI, USDC and USDT, within 2bps. ETH yield from stkAAVE increases from around 10bps to 43bps. This would bring the current yield on ETH up from 64bps to to 103bps which compares favourably with stETH yielding 400bps and Compound yielding 6bps.

A 0.9 multiplier was applied to USDC to reduce the borrowing vAPR to be almost the same as DAI. A multiplier of 2.5 for FEI was used due to the small size of the market, $22.53m and this generates a subsidy of 179bps. Hopefully this encourages Users to deposit FEI as the current lending yield is 2.27% and the borrowing yield is the highest for any stablecoin on the v2 market. It is worth noting that even with the multiplier applied FEI receives 1% of the proposed incentives which is less than 8.85 stkAAVE per day.

Amending the stkAAVE rewards to be 100% on borrowers is thought to improve the capital efficiency relative to the previous 33% on Lenders and 67% on Borrowers. It is expected that the subsidised borrowing rates encourage Users to borrow funds such that the demand creates a lending vAPY sufficient to attract capital into the market.

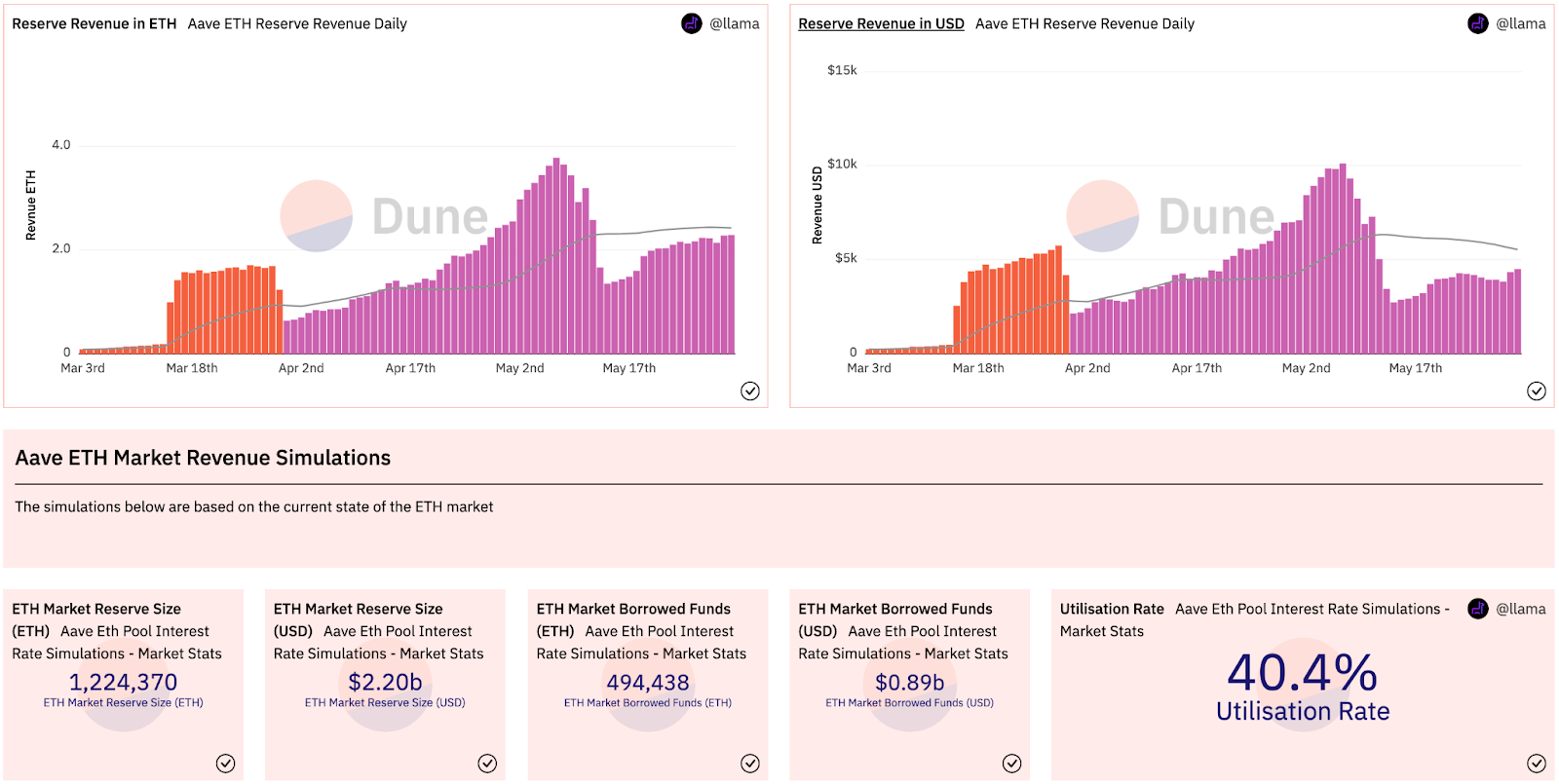

Further to incentivising borrowing of stablecoins, this proposal is seeking to increase the amount of ETH deposits. Listing stETH has generated $2.52B in TVL for the community and the image below shows the change in revenue from Users borrowing ETH since stETH was listed. The change of colour represents when AIP-68: Optimizing ETH Rates as implemented. There are likely to be several other types of staked ETH derivatives listed on Aave in the future and having sufficient ETH supply enables lower borrowing costs without actively incentivising Users to recursively borrow ETH to purchase stETH. Users who deposit ETH and Borrow supported stablecoins will receive both lending and borrowing incentives.

Reference: https://dune.com/llama/Aave-ETH-Market-Parameters-Simulation

Copyright

Copyright and related rights waived via CC0.