Gm, sorry for not posting before ! That’s an interesting proposal but imo we’re too late to the party to invest 2M$ in CRV.

Disclaimer: I’m contributing as DeFi strategist to @TokenLogic (mostly on GHO liquidity strategy atm) & @Llamaxyz (mostly on the SM Upgrade). This comment represents my personal view & a quick data analysis.

I tried to propose adding CRV to the treasury and build a veCRV position 2 years ago, aiming for a significant spot in the Curve Wars, at this point it would have been interesting but now it seems inappropriate to allocate ñearly 8% of the stable treasury to acquire CRV when Curve is not the most efficient DEX anymore.

Additionally, this proposal does not take into account that other strategic assets acquisitions might be proposed in the coming months (such as BAL/AURA, MAV and/or LIT/LIQ for example).

I do support allocating the CRV already in the treasury to either vlCVX, reducing the amount of time and benefit from the discount in price (if OTC deals can be found ofc), or veCRV to minimize additional risks and keep a long term position.

With this additional amount acquired, it seems obvious that the sdCRV is not a viable option anymore as it would lead to a highly reduced voting power compared to the other options without a significant amount of boost or SDT lock.

However, even if I agree that spending 2M$ would send a strong support signal, it might not be the best decision to buy that much CRV now as the impact on GHO support would still be limited, even if improved for secondary pools.

It’s important to note that Curve emission will be reduced by 15% this month (like each year) impacting the previous calculations shared on CRV related proposals. Starting in August 2023, the yearly community allocation will drop from ~ 194.3M to ~ 163.4M CRV, leading to a weekly reduction of ~ 560k CRV emissions.

Additionally, many OTC deals have been made, increasing the veCRV supply and diluting furthermore the CRV emissions. It seems a considerable part has been locked as stated on the Dune dashboard shared in @TokenLogic comment, but might not be fully updated as new deals can happen so the supply might increase even more. Also, even if unlikely, an important relock event from current veCRV holders can theoretically increase the veCRV supply from 619M to 710M.

Nevertheless, here are some approximative estimations on the CRV new emissions with current supply & prices for each options (happy to explain calculations details if needed & fix errors if any obviously):

1. Acquisition of 5M CRV + holdings (emissions in CRV with veCRV voting option):

Note that veCRV has a 4 years lock and a decay so it needs to be relocked each week to retain max voting power. This table is not taking into account the DAO veBoost or liquidity deposited as it would require a deeper analysis.

2. Acquisition of 5M CRV + holdings used to acquire CVX (emissions in CRV & CVX if farming on Convex with vlCVX voting option):

Considering there are a lot of variables that can influence these numbers, this assumes that:

- An OTC deal at market prices CRV to CVX is found

- The DAO farm on Convex as the boost is higher (so Convex fees are deduced)

- The DAO would lock CVX for vlCVX & vote with it to support GHO pools

- Ratio veCRV/vlCVX is calculated using cvxCRV total supply divided by vlCVX voting supply last round

Note that vlCVX has a 4 months lock without decay to retain max voting power. This table is not taking into account Convex veBoost or liquidity deposited as it would require a deeper analysis.

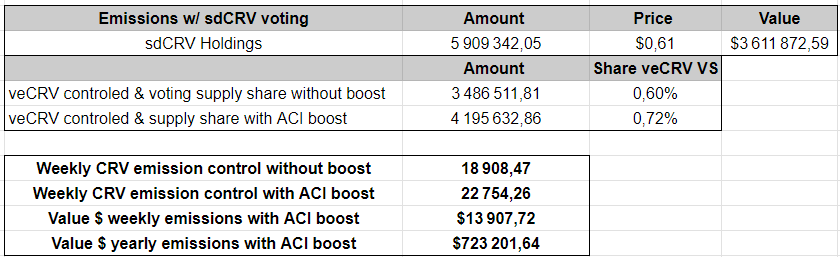

3. Acquisition of 5M CRV + holdings used to deposit in sdCRV locker reward contract (emission of CRV with sdCRV voting option):

Considering there are a lot of variables that can influence these numbers, this assumes that:

- CRV are deposited on the locker at 1:1 (buying a small amount if underpeg could slightly increase this amount but liquidity is limited)

- SDT emissions are not included as it would require veSDT gauge power

- The DAO will not farm on Stake DAO as the veCRV boost is lower than Convex

- No additional veBoost delegation & no veSDT acquisition

Note that sdCRV has no lock but the boost (if any) needs to be relegated each week to retain max capacity. However the emissions are quite lower than other options without significant veSDT support. This table is not taking into account StakeDAO veBoost or liquidity deposited as it would require a deeper analysis.

Overall, this shows that no matter which option is choosen, the extra support that could be added with this acquisition is limited for liquidity pools with considerable TVLs.

For this reason I disagree with the argument of this acquisition leading to a strategic position for the DAO, but I can’t deny that any amount acquired would both increase the voting power for Curve secondary GHO pools, and send a support signal

This acquisition represents ~ 8% of the stable treasury spent on an incomplete proposal as there is no information about the estimated benefit and possible additional support brought. It doesn’t take into account the fact that the DAO might need to acquire more efficient strategic assets.

I’d personally be supportive of allocating 1-2% of the stable treasury to benefit from a discount of buying from 250K$ to 500K$ maximum as a support to the DeFi ecosystem as you proposed, but more seems overspending.

I can update the above estimations with a smaller amount and evaluate the impact depending on several TVL targets if needed.

This is really bothering me tbh. Time sensitivity is taken as the reason this time (not sure it’s still really the case with the considerable HF increase & amount of OTC deals that happened during the weekend), but it’s not the first time you’re proposing to bypass the governance framework which you proposed a few weeks ago.

This proposal and others recently posted, should simply be viewed as invalid since it’s not respecting the governance guidelines in my opinion (direct ARFC without TEMP CHECK or direct AIP without ARFC snapshot vote), but anyway, that might be a topic for another proposal.

Considering ACI’s influence in the Aave DAO & the ecosystem in general, I believe you should spread the right word instead of setting bad precedents in the Aave governance history.

Against the direct AIP, I can agree that emergency protocols are needed but they also need to be stated and clearly defined with guidelines in the governance framework.

Happy to help draft an improvement of the current framework with @TokenLogic if needed !

The above data analysis can be viewed as a follow up of the @TokenLogic comment above, however opinions in this comment are my own.

Highly disagree with this. This proposal was posted during summer including the first weekend of August, with only 4 days of discussions (clearly not enough since no consensus has been reached), and while several participants expressed their disagreement about this proposal, it doesn’t seem you’ve taken their feedback into account.

Moreover, while the request to learn more on the expected support for GHO & other specifications were posted several times, the ACI didn’t shared any (making it complex for the community to be in a suitable position to vote) and is ready to publish an AIP bypassing 3 times the governance framework:

- No TEMP CHECK forum post

- No TEMP CHECK snapshot vote

- No ARFC snapshot vote

I’m really concerned about the potential future impacts of these decisions on the Aave governance.