It seems obvious that major conflicts of interests are rising. Some people are trying to defend personal positions and expositions to a potential collapse of CURVE.

First, I would like to remind everyone here that the Aave “DAO” gouvernance is here for its community. This means protecting them in times of troubles.

This proposal is an economic non-sense. Our only mission is to mitigate AAVE risk and exposure to this situation. What Marc is proposing, is to increase our exposure.

We can not trust Michel Ergorov who has been playing a dangerous game. And as we speak he is still looking for “OTC deals”; let’s be honest here: he is dumping. Michel Ergorov is flooding the market with his CRV tokens, holding on to one statement “TOO BIG TOO FAIL”.

Aave has the opportunity to restore trust and positivty into the entire crpyto market by taking the right decisions, which is protecting our users and investors instead of “helping” a fraudulent “CEO” playing with funds.

We need to act now to protect our people and to protect Aave.

With all your respect, ser. I think the best way to protect AAVE is to acquire CRV at a discount and keep de-risking that market, the user will use 2M USDT to pay his debts. It’s too late to make substantial changes, that train left one year ago, and now it’s time to control the damage due to a bad risk management strategy. We need to accept that managing a lending protocol is extremely difficult vs. an AMM type of product. Let’s see the bright side of things, the user will start paying his debts; we will try to freeze the market, lower the LTV to zero, and gradually lower the LT while at the same time pushing the big migration from v2 to v3

Honestly i don’t particularly care what he does with his tokens, as long as he repays the debt (which he is actually doing). Sure a long way to go, but all things considered, if this proposal moves forward, the 2M USDT will be used to repay the debt (which reduces exposure) and aave acquires CRV. If the position gets liquidated afterwards, the CRV will be worthless, but there will be two millions less to cover in bad debt. If the proposal doesnt go forward and the position gets liquidated anyway, those two millions will be needed to cover the bad debt, achieving the same net result minus the worthless CRV. So the difference is minimal, but if the proposal goes forward, the governance gets upside in case things go well (position doesnt get liquidated).

Blockquote If Aave really wanted to protect the interest of its stakeholders and its lenders, the best strategy to use 2M USDT would be to place a limit order for CRV at $0.21 in order to buy it at a much lower price then what is currently proposed with this OTC trade. The possible outcomes would be:

If the price never drops to $0.21 then it is all good, the protocol doesn’t accrue any bad debt due to the liquidation!

If the price drops below $0.21 then the CRV position has been liquidated and Aave has occurred in bad debt, but at least we got CRV at a much lower price than $0.40…

This would be reasonable only if you managed to liquidate the position at 21cents per CRV, not to buy on the market. Buying on the market doesnt achieve the same effect because the 2M go to other counterparties, here they will be used to repay the loan. But i wouldnt bet on that game, getting into liquidating when there is a gov process in the middle is essentially impossible.

The structure of the CRV acquisition seems kind of disadvantageous to the DAO. It’s only a fair deal if both sides commit to the acquisition. Giving 0x7a simply the OPTION to swap at a predetermined price from a contract, from a purely economic point of view, is just nonsense.

I would suggest setting a predetermined price and having that address commit the funds beforehand. If they want the DAO to buy distressed assets, then the onus should be on them to put up their collateral first IMO.

Hi

I will vote for

-lots of synergies for Aave Governance to hold CRV ( liquidity of GHO on Curve)

-good OTC market price

-better for next bull run to hold CRV than USDT

-high risk reward investment

As a trader, CRV price chart is doing a double bottom pattern with a target between 10.8, 13 or 17.2 $ (OTC price 0.4$)

We’re generally supportive of expanding into CRV for the benefit of GHO and additionally we recognise that Aave V2 has generated some significant fees in USDT from the position of the specific wallet.

That being said while the treasury can handle a 2m USDT reduction we would be more in favour of swapping an asset such as ARB to USDT and cover the transaction.

We support this proposal to take advantage of this OTC deal to acquire more CRV, we believe that this opportunity will further spur our plans for bringing secondary liquidity to GHO.

I can sympathize with the sense of justice from some who have come out against this proposal. However, the proposal appears to offer a strong risk-adjusted benefit to Aave.

Firstly, whether we like it or not, there is a high risk CRV position on Aave. Some here have brought up that the position is fairly healthy - however, I would like to remind them that there does not appear to be enough liquidity on-chain to support such a position size. It is not unreasonable then, especially considering how volatile/manipulatable these markets are, for users to consider this position as bad debt regardless of health factor. The owner of the position is paying it down as they raise funds OTC, so there is at least some strategic advantage in approving this proposal.

Secondly, holding CRV comes with the utility of CRV which provides multiple additional advantages for Aave, such as additional influence over liquidity for the GHO token. I believe those with a strong sense of justice against the Curve founder must look past it and see the undeniable importance of Curve in the DeFi ecosystem and the benefits CRV provides Aave.

And finally, there is some margin of safety due to the unique opportunity to acquire CRV at a discounted $0.4.

I strongly believe the downside risks of purchasing $2M worth of CRV are far outweighed by the benefits listed above. In addition to approving this proposal, we should also adjust our risk parameters appropriately to prevent another situation like this one from arising in the future.

Daily Revenue from CryptoFees.info, $2.6M daily revenue on Aave v2 Ethereum, 2nd August 2023. The revenue from just Ethereum v2 on one day exceeded the value requested in the proposed OTC deal.

The health factor of Michael’s position is 2-2.10 with around $40M of debt. If liquidated, the DAOs funds would be called upon and it is likely a Short Fall event will occur which will significantly affect the AAVE price. There was clear front running speculation on 30th and 31st July when AAVE and CRV prices moved in tandem. This also risks causing liquidations to users that have AAVE as collateral.

We note that at $2M USDT, this is small relative to the debt outstanding. Michael has been continually selling CRV up to now and there is every indication this could continue until either such time as the risk exposure to Aave is meaningfully lower or the OTC deal flow dries up. The latter is an understated risk and may justify the DAO exploring a purchase.

We are supportive of helping de-risk Aave Protocol and sending a positive signal to the market. However, it is unknown if Aave DAO participation will make a material difference. Several well known actors like @WintermuteGovernance have already participated in the OTC offering.

Acquiring CRV at 40 cents/unit is expected to generate an instant $1,000,000 unrealised profit due to the DAO receiving a 33% discount to the spot price, 60 cents per unit of CRV. This is the same price offered for the other 111M units of CRV being sold via OTC in the last few days. This can be viewed as a binary value proposition, if the position is liquidated this goes to zero. If Michael avoids cascading liquidations, then Aave will have an unrealised profit.

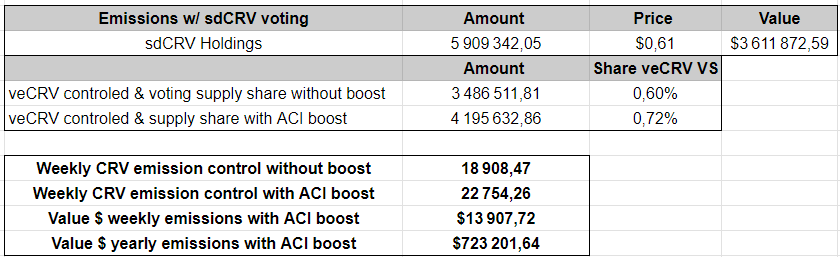

There are some benefits to GHO liquidity. For context, the CRV can be used to attain veCRV and sdCRV, which will give Aave DAO around 1% and 0.72% (with ACI Boost) of veCRV. There are other benefits to sdCRV as well. However, both options can be used to direct emissions to GHO pools. Using the CRV position to support GHO is complementary to the Balancer strategy. We note GHO/crvUSD will likely receive support from other actors.

From the perspective of investing $2M to purchase an asset to boost GHO, acquiring CRV is not the most efficient use of DAO funds. The relative maturity of Curve’s inflation schedule to other DEXs, means the highest Return on Investment will be elsewhere. However, we reiterate this is not the main value driver, but if it was, then alternative investments should be considered.

More generally, our concerns specific to veCRV are detailed below:

veCRV Supply increase substantially over the recent week due to OTC deals

15% reduction in CRV inflation schedule occurring during August

Emissions will drop from ~ 194.3M to ~ 163.4M, leading to a weekly reduction of around 560k CRV

Previous discussions bootstrapping GHO/crvUSD with Michael concluded he would personally provide, >1M worth of veCRV voting support without any support from Aave DAO.

The volume of CRV swapped through OTC deals by Michael is shown below.

The increase in CRV deposited into the veCRV contract is shown below.

We would like to thanks everyone involved in the discussion about this proposal and we’re grateful for the high quality of the discussion.

With the ACI and as proposal creators, we feel that everyone had ample opportunity to voice their opinion against or in support of this proposal.

Furthermore, @TokenLogic recent feedback added valuable information in the context of this proposal

We feel the community is now in a suitable position to cast their opinion during an AIP vote.

Tentatively the ACI in cooperation with @bgdlabs for payload review will escalate this proposal to AIP stage on Monday.

In terms of implementation, the AIP execution will result inside the same atomic transaction to the pulling of aCRV from the counter party of this proposal and the repayment of the counterparty position via USDT.

If for some reason 0x7a16ff8270133f063aab6c9977183d9e72835428has not approved the governance V2 Short executor on aCRV contract, the proposal will fail regardless of the voting outcome assuring no risk is taken by any of this agreement parties.

The execution will be carried out on-chain, in a transparent, auditable, and decentralized manner, aligning with both the Aave and Curve ethos.

From now on, the community is invited to voice their opinion by casting a vote during the AIP stage.

In my opinion, opportunistic asset acquisition doesn’t set a good precedent for what I think should be the DAO’s strategy.

As we can see in this thread, it is pretty easy to support the proposal if doing multiple assumptions, like the acquisition price (which counterparty should accept), CRV market price, how it reduces the aforementioned debt position, some (non defined at all) future strategy with GHO, etc.

But by that rule, multiple other assets “look” net positive.

I don’t believe Aave should focus on this type of asset investment at this stage, as the DAO is simply not prepared for it while keeping high-quality innovation, security, and overall quality. For example, what GHO needs is more innovation, improvement, and adoption.

I am curios, what kind of improvement and innovation do you think GHO needs? And how else should you thrive adoption of GHO if not with the stablecoin DEX itself Curve. I may just not see it that’s why I am asking. But imo CRV could be used to vote for GHO pools and incentives for people to mint and deepen liquidity.

Just a little side note. I don’t think cryptofees is accurate. Aave v3 Arbitrum is showing high fees for a long time now and I cannot imagine these numbers are correct.

Gm, sorry for not posting before ! That’s an interesting proposal but imo we’re too late to the party to invest 2M$ in CRV.

Disclaimer: I’m contributing as DeFi strategist to @TokenLogic (mostly on GHO liquidity strategy atm) & @Llamaxyz (mostly on the SM Upgrade). This comment represents my personal view & a quick data analysis.

I tried to propose adding CRV to the treasury and build a veCRV position 2 years ago, aiming for a significant spot in the Curve Wars, at this point it would have been interesting but now it seems inappropriate to allocate ñearly 8% of the stable treasury to acquire CRV when Curve is not the most efficient DEX anymore.

Additionally, this proposal does not take into account that other strategic assets acquisitions might be proposed in the coming months (such as BAL/AURA, MAV and/or LIT/LIQ for example).

I do support allocating the CRV already in the treasury to either vlCVX, reducing the amount of time and benefit from the discount in price (if OTC deals can be found ofc), or veCRV to minimize additional risks and keep a long term position.

With this additional amount acquired, it seems obvious that the sdCRV is not a viable option anymore as it would lead to a highly reduced voting power compared to the other options without a significant amount of boost or SDT lock.

However, even if I agree that spending 2M$ would send a strong support signal, it might not be the best decision to buy that much CRV now as the impact on GHO support would still be limited, even if improved for secondary pools.

It’s important to note that Curve emission will be reduced by 15% this month (like each year) impacting the previous calculations shared on CRV related proposals. Starting in August 2023, the yearly community allocation will drop from ~ 194.3M to ~ 163.4M CRV, leading to a weekly reduction of ~ 560k CRV emissions.

Additionally, many OTC deals have been made, increasing the veCRV supply and diluting furthermore the CRV emissions. It seems a considerable part has been locked as stated on the Dune dashboard shared in @TokenLogic comment, but might not be fully updated as new deals can happen so the supply might increase even more. Also, even if unlikely, an important relock event from current veCRV holders can theoretically increase the veCRV supply from 619M to 710M.

Nevertheless, here are some approximative estimations on the CRV new emissions with current supply & prices for each options (happy to explain calculations details if needed & fix errors if any obviously):

1. Acquisition of 5M CRV + holdings (emissions in CRV with veCRV voting option):

Note that veCRV has a 4 years lock and a decay so it needs to be relocked each week to retain max voting power. This table is not taking into account the DAO veBoost or liquidity deposited as it would require a deeper analysis.

2. Acquisition of 5M CRV + holdings used to acquire CVX (emissions in CRV & CVX if farming on Convex with vlCVX voting option):

Considering there are a lot of variables that can influence these numbers, this assumes that:

An OTC deal at market prices CRV to CVX is found

The DAO farm on Convex as the boost is higher (so Convex fees are deduced)

The DAO would lock CVX for vlCVX & vote with it to support GHO pools

Ratio veCRV/vlCVX is calculated using cvxCRV total supply divided by vlCVX voting supply last round

Note that vlCVX has a 4 months lock without decay to retain max voting power. This table is not taking into account Convex veBoost or liquidity deposited as it would require a deeper analysis.

3. Acquisition of 5M CRV + holdings used to deposit in sdCRV locker reward contract (emission of CRV with sdCRV voting option):

Considering there are a lot of variables that can influence these numbers, this assumes that:

CRV are deposited on the locker at 1:1 (buying a small amount if underpeg could slightly increase this amount but liquidity is limited)

SDT emissions are not included as it would require veSDT gauge power

The DAO will not farm on Stake DAO as the veCRV boost is lower than Convex

No additional veBoost delegation & no veSDT acquisition

Note that sdCRV has no lock but the boost (if any) needs to be relegated each week to retain max capacity. However the emissions are quite lower than other options without significant veSDT support. This table is not taking into account StakeDAO veBoost or liquidity deposited as it would require a deeper analysis.

Overall, this shows that no matter which option is choosen, the extra support that could be added with this acquisition is limited for liquidity pools with considerable TVLs.

For this reason I disagree with the argument of this acquisition leading to a strategic position for the DAO, but I can’t deny that any amount acquired would both increase the voting power for Curve secondary GHO pools, and send a support signal

This acquisition represents ~ 8% of the stable treasury spent on an incomplete proposal as there is no information about the estimated benefit and possible additional support brought. It doesn’t take into account the fact that the DAO might need to acquire more efficient strategic assets.

I’d personally be supportive of allocating 1-2% of the stable treasury to benefit from a discount of buying from 250K$ to 500K$ maximum as a support to the DeFi ecosystem as you proposed, but more seems overspending.

I can update the above estimations with a smaller amount and evaluate the impact depending on several TVL targets if needed.

This is really bothering me tbh. Time sensitivity is taken as the reason this time (not sure it’s still really the case with the considerable HF increase & amount of OTC deals that happened during the weekend), but it’s not the first time you’re proposing to bypass the governance framework which you proposed a few weeks ago.

This proposal and others recently posted, should simply be viewed as invalid since it’s not respecting the governance guidelines in my opinion (direct ARFC without TEMP CHECK or direct AIP without ARFC snapshot vote), but anyway, that might be a topic for another proposal.

Considering ACI’s influence in the Aave DAO & the ecosystem in general, I believe you should spread the right word instead of setting bad precedents in the Aave governance history.

Against the direct AIP, I can agree that emergency protocols are needed but they also need to be stated and clearly defined with guidelines in the governance framework.

Happy to help draft an improvement of the current framework with @TokenLogic if needed !

The above data analysis can be viewed as a follow up of the @TokenLogic comment above, however opinions in this comment are my own.

Highly disagree with this. This proposal was posted during summer including the first weekend of August, with only 4 days of discussions (clearly not enough since no consensus has been reached), and while several participants expressed their disagreement about this proposal, it doesn’t seem you’ve taken their feedback into account.

Moreover, while the request to learn more on the expected support for GHO & other specifications were posted several times, the ACI didn’t shared any (making it complex for the community to be in a suitable position to vote) and is ready to publish an AIP bypassing 3 times the governance framework:

No TEMP CHECK forum post

No TEMP CHECK snapshot vote

No ARFC snapshot vote

I’m really concerned about the potential future impacts of these decisions on the Aave governance.

On the topic of “Direct-to-AIP” request, as you quoted, it’s an exceptional request for a time-sensitive proposal.

One thing I can guarantee is that if the DAO had taken the path of TEMP CHECK post (5 days) TEMP CHECK snapshot (4 days), ARFC post (5 days), ARFC Snapshot (4days) AIP vote and execution (4 days) the probability of the deal being still on the table is Zero. (current user HF is 2.21)

Suggesting taking the regular slow path was a viable option is revealing that you’re not very familiar with these deals and that’s a bit concerning for potential candidates for “treasury management”

On the opening of the 7th of August 2021, CRV price was 1.94$, a 2M USDT back then would have resulted in a 1.03M CRV acquisition, 5 times less than what the DAO can acquire now.

Two years ago, an aave stablecoin was not even a topic for the DAO and was not developed by the aave companies. That’s another example of the potential added value of your team for “treasury management”

I wrote most of these rules and submitted them for governance approval. They’re as important for the DAO as they’re for me. Until your post, I’ve witnessed exactly zero objection to the request for an exceptional bypass.

On the topic of the deal itself, it’s pretty hard for me to understand how a deal that makes on day one the DAO in the green for 1m$ and has the potential to generate up to 1m$ of yearly revenue by emission (option 1) while helping GHO is so terrible for the DAO.

If the technical review allows it and the counter-party confirm their willingness to process forward, the proposal will be escalated today to AIP stage, this topic is an example of having ample room for discussion in support or in opposition to the proposal. It is now time for the governance to speak by casting votes.

{kind=link}