LlamaRisk supports this ARFC and recommends onboarding bCSPX as a collateral-only asset within Aave V3 on Gnosis. bCSPX is an ERC20 token that tracks the performance of the iShares Core S&P 500 UCITS ETF—providing on-chain exposure to U.S. large-cap equities through Backed’s suite of tokenized real-world assets. The token is deployed on multiple chains (Ethereum, Gnosis, Polygon, Arbitrum, and Avalanche) with plans for Sonic deployment. Liquidity is notably concentrated on Gnosis via Balancer v2 and Swapr pools, which together hold a TVL of approximately $5.5 million.

The availability of a Proof of Reserves feed provides reassurance about the token’s underlying collateral. However, we have observed short-term pricing volatility in bCSPX, with brief upward spikes followed by downward adjustments that mirror fluctuations in London Stock Exchange quotes. This volatility is further exacerbated by the price feed’s 15-minute delay. Additionally, the protocol’s concentrated ownership structure presents a separate risk factor. In light of these factors, we do not recommend borrowing with bCSPX at this time.

Comprehensive audits have resolved all smart contract issues, and following detailed discussions with LlamaRisk, the team has agreed to launch a bug bounty program soon to further enhance protocol security.

From a regulatory standpoint, bCSPX operates under Jersey financial laws and the Swiss DLT Act. Its underlying ETF is authorized by the Irish Central Bank, and token issuance is approved by the Financial Market Authority of Liechtenstein. Custody services are provided by Maerki Baumann & Co. AG and InCore Bank AG, with token holders represented by Security Agent Services AG. Backed employs an institutional Multiparty Computation (MPC) Wallets solution from Fordefi.

In light of the current liquidity profile and pricing challenges, a conservative risk approach—using bCSPX solely as collateral—is advised to ensure safe integration into Aave V3 while expanding Aave’s exposure to tokenized real-world assets.

Collateral Risk Assessment

1. Asset Fundamental Characteristics

1.1 Asset

Issued as an ERC20 token, the Backed CSPX Core S&P 500 (bCSPX) functions as a tracker certificate that mirrors the iShares Core S&P 500 UCITS ETF (CSPX). The underlying ETF aims to reflect the net total return of the S&P 500 Index, composed of 500 of the largest publicly listed companies in the United States, while deducting its fees and expenses. By holding bCSPX, investors gain on-chain exposure to the same performance profile of CSPX in a format that can be easily transacted on blockchain networks.

bCSPX is one offering among a wider suite of bTokens created by Backed; a firm focused on tokenizing real-world assets in compliance with EU financial regulations. Each bToken takes the form of a structured product directly issued on a blockchain and represents a debt certificate fully collateralized 1:1 by an underlying traditional asset, such as an ETF or an equity. The bToken ecosystem spans multiple chains, including Ethereum, Gnosis, Polygon, Arbitrum, Fantom, Avalanche, BNB Smart Chain, and Base.

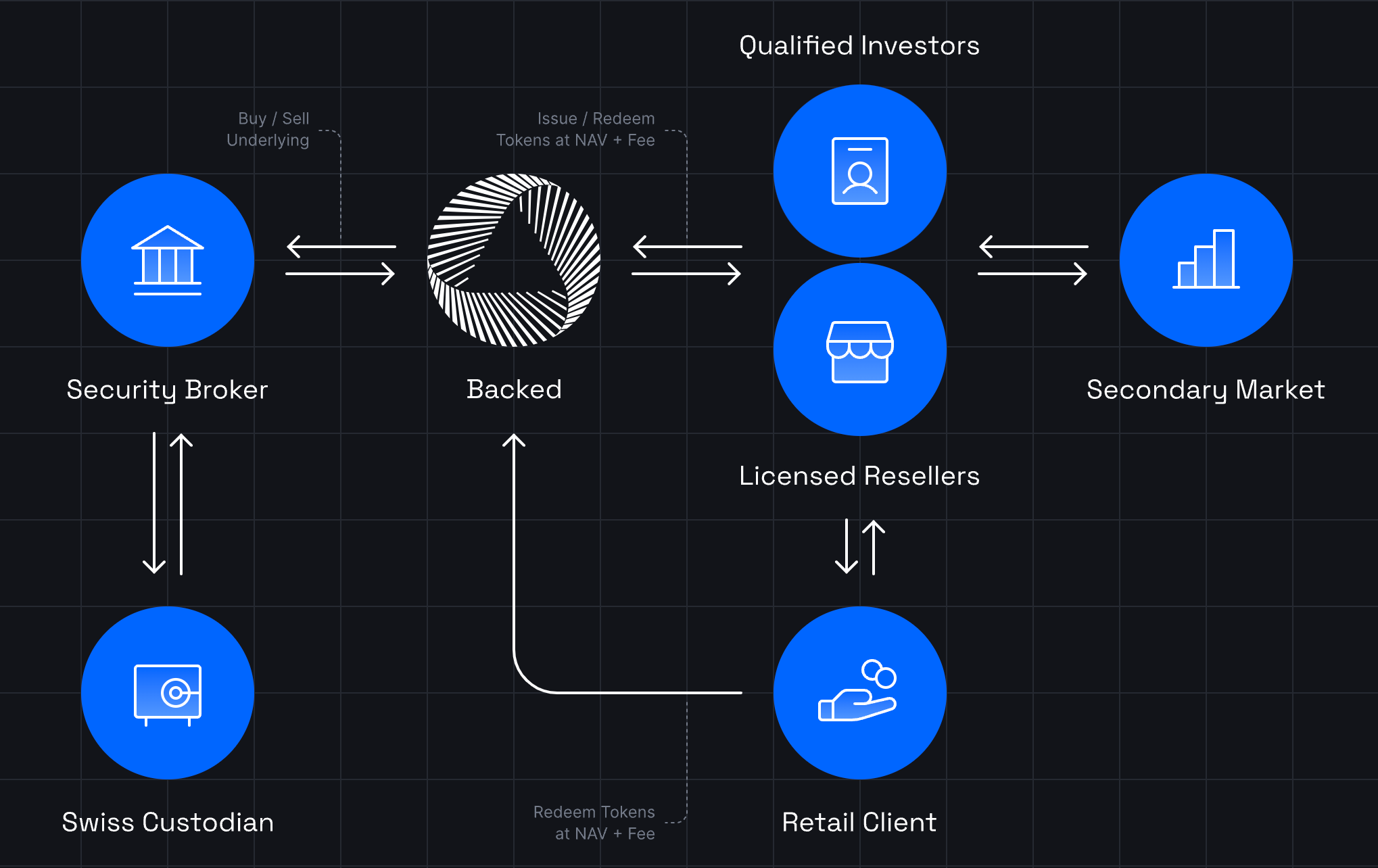

1.2 Architecture

Only professional/qualified investors can mint or redeem bCSPX, while retail participants have redemption rights but cannot mint new tokens. Under Jersey law, professional investor status may be granted to financial professionals, high-net-worth individuals, regulated service providers, EU professional clients, persons recognized by the Jersey Financial Services Commission (JFSC) on a case-by-case basis, etc. Prospective investors affirm this capacity by completing a self-declaration form. Backed products are unavailable to US persons, US entities, US-controlled entities, and entities or individuals located in prohibited or high-risk jurisdictions.

The subscription process, also known as issuance, starts with the tokenizer (Backed Finance AG) pre-creating ledger-based securities for specific products and holding them in a wallet on behalf of the Issuer (Backed Assets (JE) Limited). When investors want to purchase a product, they submit an order to the Issuer and go through a KYC process. Once the KYC is complete and the Issuer receives payment, it buys the equivalent amount of underlying and transfers it to a collateral account. Then, they instruct the tokenizer to activate the pre-created securities and transfer them to the investor’s specified wallet. It’s worth noting that if the Issuer can’t purchase the underlying within the given timeframe, they’ll cancel the order and refund the investor, minus a small fee to cover expenses.

The redemption process can be triggered in two ways: an investor submits a redemption order (exercising their Investor Put Option), or the issuer decides to terminate a product (using their Issuer Call Option). The issuer’s call is an uncommon measure, generally included for regulatory and legal safeguard purposes. Furthermore, a robust KYC process is in place to ensure full compliance with regulatory standards. Once the tokenizer receives the investor’s products and forwards the redemption order to the Issuer, the Issuer has five business days to complete the redemption. During this time, they deactivate the received products, liquidate the corresponding underlying in the collateral account, calculate the redemption amount, and finally, instruct the payment provider (the custodian) to pay the redemption amount to the investor. If an investor opts to redeem in stablecoins, the issuer converts the specified amount into the chosen stablecoin and transfers it to the investor’s pre-approved wallet.

Issuance for bCSPX generally follows a T+2 timeline, which ensures that new tokens are minted within two business days. Smaller orders can be processed within minutes through Backed’s available working capital. When investors wish to purchase, they must submit an order and complete mandatory KYC procedures by regulatory requirements. The Issuer maintains discretion in rejecting orders based on negative findings.

A similar structure applies to redemptions, where requests of modest size can be settled promptly, and larger ones are finalized within T+3. As with subscriptions, successful KYC verification is required before redemption can proceed. Redemptions may be received in stablecoins or cash, and while orders can be placed at any time on the Backed platform, actual execution depends on the trading hours of the exchange where the underlying ETF is listed. Daily and monthly operational limits apply at different thresholds for professional and institutional clients.

Source: https://assets.backed.fi/, February 19th, 2025

1.3 Tokenomics

bCSPX is issued or redeemed at the price Backed’s brokers obtain for the underlying asset, plus applicable fees, in adherence to best execution practices. The total issue volume can go up to CHF 100,000,000, with the possibility of further expansion. Subscribers can invest at least CHF 5,000, while the overall issue volume caps the maximum. A transaction fee of 0.5% is charged on both issuance and redemption, and no performance fee is associated with bCSPX. The Issuer of the underlying ETF charges an annual management fee of approximately 0.07% of the investment’s value. This rate reflects the actual costs documented by the ETF over the past year.

1.3.1 Token Holder Concentration

On Mainnet Backed:Deployer controls 99.35% of the total supply of 2,843.43 tokens ($1.8m at current ETF price). The next four holders out of 54 in total collectively own <0.34% of the supply.

Source: Etherscan, February 19th, 2025

The total supply of 8622.47 tokens ($5.5m) on the Gnosis chain is currently held by 119 addresses, but the ownership is heavily skewed toward the top holders. Four addresses dominate the token distribution, collectively controlling 98.75% of the total supply. The primary holder is a Vault with 31.15%, followed by the Backed: Deployer holding 28.52%.

Source: Gnosisscan, Date: February 19th, 2025

Overall, the supply of bCSPX is distributed over 5 different chains as follows:

Source: Chain explorers (linked above), February 19, 2025

2. Market Risk

2.1 Liquidity

Liquidity for bCSPX is concentrated on the Gnosis Chain, where the Balancer v2 bCSPX/sDAI pool maintains a total value locked of approximately $3,475,096 including $1.72M in bCSPX. A bCPSX/sDAI pool on Swapr is also available and has $1.05M in bCPSX.

In addition, a lending option through PWN.xyz offers a long strategy with around $30,362.94 in available credit, accessible in USDC.e, EURe, and WXDAI against bCSPX collateral.

There are currently 1900 bCSPX ($1.2m) available to be sold for USDC.e under 2.5% price impact on Gnosis.

Source: CowSwap, Date: February 18th, 2025

2.2 Volatility

bCSPX has reliable price alignment with its underlying CSPX ETF. The trading pattern for bCSPX/USD on DEX demonstrates overall stability, with small-bodied candles reflecting the change underlying off-chain ETF’s price changes.

Source: GeckoTerminal, Date: February 19th, 2025

2.3 Exchanges

Beyond its Balancer and Swapr presence, bCSPX does not currently have listings on centralized exchanges.

2.4 Growth

The tokenized stock metrics for bCSPX reveal distribution across two networks, with Gnosis Chain holding the majority at $5.60M and Ethereum maintaining $1.80M, totaling $7.40M in market cap.

The current price of $641.86 bCSPX has demonstrated a strong upward trend visible from March 2023 to February 2025 with approximately 24% price growth, reflecting the broader positive tradFi market conditions since October 2024.

Source: Goingecko, Date: February 19th, 2025

The total supply of the bCSPX tokens has risen overall in 5 chains. The growth has correlated with the positive market periods, especially since the beginning of November 2024.

Source: Dune, February 18th, 2025

3. Technological Risk

3.1 Smart Contract Risk

3.2 Bug Bounty Program

Backed does not presently offer a bug bounty program. After contacting the protocol team, we were informed that the bug bounty program would be created in the near future.

3.3 Price Feed Risk

Source: https://oracles.backed.fi/, Date: February 19th, 2025

An active Chainlink CSPX/USD oracle supports the asset by updating its data daily or whenever a market price fluctuation exceeding 2% occurs. The market price feed relies on sources from the London Stock Exchange, with updates on a fifteen-minute delay.

The feed setup and the inherent delay may result in a large deviation between the oracle’s reported price and the secondary market price on DEX pools. This is an important consideration for time-critical integrations, especially in lending protocols.

3.4 Dependency Risk

bCSPX employs a Chainlink Proof of Reserves feed, which refreshes every 24 hours or earlier if the latest value diverges by more than 10% from the previously recorded figure. This Proof of Reserves mechanism is facilitated by The Network Firm, an independent auditor granted full access to Backed’s custody accounts. By examining bCSPX’s collateral, the firm verifies the underlying reserves and provides an attestation relayed on-chain via an external adapter.

Source: Backed Proof of Reserves Architecture, Date: February 19th, 2025

bCSPX contract implements:

- ERC-20 token functionality, incl. support for basic token operations like transfer, balance tracking, and allowances.

- EIP-712 Standard for permitted and delegated transfer functionality, token approvals and transfers via signed messages, gas-efficient and secure way to manage token permissions

- Chainalysis sanctions list interface to prevent transfers involving sanctioned addresses

The contract imports and depends on the following:

@openzeppelin/contracts-upgradeable/access/OwnableUpgradeable.sol - upgradability frameworkERC20PermitDelegateTransfer.sol (custom implementation)SanctionsList.sol (custom implementation)

4. Counterparty Risk

4.1 Governance and Regulatory Risk

European investment regulations established the iShares Core S&P 500 UCITS ETF underlying bCSPX as a UCITS fund. Its Issuer, iShares VII Public Limited Company, J.P. Morgan, 200 Capital Dock, 79 Sir John Rogerson’s 8 Quay, Dublin 2, D02 RK57, Ireland, operates under authorization from the Irish Central Bank and is registered under number 469617.

bCSPX itself is issued by Backed Assets (JE) Limited, incorporated in Jersey Channel Islands and wholly owned by Backed Finance AG in Zug, Switzerland. The bCSPX issuance observes Jersey legal requirements, along with COBO consents under the Control of Borrowing (Jersey) Order 1958 and CGPO consents under the Companies (General Provisions) (Jersey) Order 2002. These approvals align with Jersey’s financial laws, ensure that high-risk securities are not offered to unsophisticated investors, and confirm adequate disclosure in the offering materials. Tokenization follows the Swiss DLT Act, meaning the securities are structured as blockchain-based cryptographic tokens. Because they do not qualify as collective investment schemes under the Swiss Collective Investment Schemes Act, they are not subject to FINMA authorization.

Source: JFSC, Date: February 19th, 2025

On May 6, 2024, the Financial Market Authority (FMA) Liechtenstein, as competent authority under the Prospectus Regulation, approved the Securities Note and Registration Document for bTokens. The Issuer has asked the FMA to notify regulators in other EU member states of this approval.

Brokerage and custodial services for bCSPX are furnished by Maerki Baumann & Co. AG, an independent Swiss private bank in Zurich, and InCore Bank AG, a B2B transaction bank also based in Switzerland.

Tokenholders possess an exclusive claim on the collateral specifically allocated to the product they hold, with no entitlement to collateral backing other products or the Issuer’s assets. Neither bCSPX nor any other Backed product is insured or guaranteed by any governmental authority, regulatory body, or agency. Tokenholders do not acquire any rights akin to those of shareholders, and they are not entitled to voting privileges, pre-emption opportunities in subscribing to the securities of the Underlying ETF, any share in profits of the Underlying ETF issuer, or rights to a distribution of surplus in a liquidation scenario affecting the Underlying ETF. Under the most recent design update, any dividends from the underlying asset are automatically reinvested in the holder’s position, and the token is rebased to incorporate these proceeds.

Security Agent Services AG is the designated Security Agent. By acquiring bCSPX, each investor appoints the Security Agent as its direct representative, enabling the investor to exercise all rights under the Collateral Agreement concluded with the Issuer and the relevant product schedule solely through the Security Agent. In the event of the Issuer’s winding up, administration, receivership, insolvency, or any debt enforcement proceedings, the Security Agent is authorized to satisfy tokenholders’ claims under the Collateral Agreement, including related fee claims, from the proceeds of the collateral before making any other payments. The Security Agent assumes control of the custody accounts and oversees the assets’ liquidation for the tokenholders’ benefit.

Grant Thornton audited the 2022 and 2023 financial statements of Backed Assets GmbH and, based on their statutory examination, identified no indications that the financial statements or the proposal to carry forward the accumulated loss fail to comply with Swiss law or the company’s articles of incorporation. Audited financial statements for 2024 are expected to be available by late April.

4.2 Access Control Risk

4.2.1 Contract Modification Options

4.2.2 Timelock Duration and Function

The contract does not have a built-in timelock mechanism. The owner can immediately change roles and settings.

4.2.3 Multisig Threshold / Signer identity

Owner: 0x22f2dFE84a2EaCfE5d3cA81d26E610CB94eB1603 is a GnosisSafe with the following signers:

0x2860a2051A93113CB6E931022b658ed1dC68D444

0xe25B606f393b60ADcB85cC127A2d79F78C9Cb658

0xd49FbB0711E91eF730c23f0D2fEF4E5C5bF96Eb1

Minter/Pauser: 0xdD276f57e40D745E09855BA5711613F5Da0C4A71 is a GnosisSafe with the following signers:

0x414f6CB44Cd975165f8299a5cCbed92aa1A26F58

0x297C815a70EC3CF394Aa3db5B4AA166448961541

0xA0807ca21101Fd097B60795A786569F6A5F5522E

Backed employs an institutional MPC solution from Fordefi.

Note: This assessment follows the LLR-Aave Framework, a comprehensive methodology for asset onboarding and parameterization in Aave V3. This framework is continuously updated and available here.

Given the limited onchain liquidity of this asset, we recommend using Chainlink’s PoR feed in conjunction with the CSPX/USD London Stock Exchange price feed of Chainlink. Nonetheless, as discussed above, the CSPX/USD price feed is delayed by 15 minutes and, therefore, possesses a risk of large deviations.

It can be observed that Chainlink’s price feed has reported upward price spikes followed by downward re-adjustments. The nature of these spikes stems from the upward, very short-term volatility observed in the quotes of the London Stock Exchange.

Therefore, these deviations justify a proposed large liquidation bonus, which would ensure the execution of liquidations at all times. In addition, we will discuss with Chainlink the potential adaptations to the CSPX/USD price feed that would eliminate the impact of short-term exchange volatility while keeping the risk properties sufficient.

In the TEMP CHECK phase, an alternative way for Aave to onboard the bCSPX asset via a GHO facilitator was suggested by @MarcZeller. There are multiple ways to segregate the risks via GHO stablecoin, keeping the risk profile of Aave’s Gnosis market unimpacted:

Nonetheless, the feasibility and implementation of each solution remain to be explored in detail, together with other service providers. Given the limited supply of the asset at the time of this analysis, operational costs for the DAO may be too large to consider onboarding this asset via a dedicated facilitator. Therefore, it is rational to integrate this asset into Aave’s Gnosis market initially.

This review was independently prepared by LlamaRisk, a community-led non-profit decentralized organization funded in part by the Aave DAO. LlamaRisk is not directly affiliated with the protocol(s) reviewed in this assessment and did not receive any compensation from the protocol(s) or their affiliated entities for this work.

The information provided should not be construed as legal, financial, tax, or professional advice.