Overview

Chaos Labs provides a recap of the impact of recent market activity on Aave V3.

During recent market events, the protocol experienced significant liquidations, primarily on the Ethereum network involving the WETH asset. All liquidations were executed efficiently, ensuring the protocol remained protected and no bad debt occurred.

Key highlights include:

- Collateral at Risk increased by 21%

- The liquidation bonus surged to $13.2 million, leading to significant protocol revenues

- Despite the market events, no accrued bad debt was identified

- We observed a 100-fold increase in liquidations compared to the daily average over the past month, which were handled effectively by the protocol

- Temporary depegging was noted in LSTs and LRTs, which will be considered in our future recommendations. A detailed report will follow

- Please note that the data for this report was collected on August 5 at 19:00 UTC

Analysis

Overall, we observed the following increases during the recent market events:

| Bad Debt | Collateral Liquidated | Agg. Liquidation Bonus | Collateral at Risk |

|---|---|---|---|

| $0 | $276.71M | $13.2M | $51.5M |

Collateral Liquidated

On the event day, liquidations surged to $276.71 million, a significant increase compared to the daily average of $2.15 million over the past month.

Liquidation Bonus

The liquidation bonus on the event day climbed to $13.2 million, a substantial jump from the monthly average of $90,000. This notable increase emphasizes the effect of recent market dynamics and the resulting surge in liquidation activity.

Collateral at Risk

Over the past month, the daily Value at Risk (VaR) averaged around $244 million, but on the event day, it surged to $295.5 million, reflecting a significant ~21% increase.

Bad Debt

We have not identified insolvencies from the previous day due to recent events. As observed, the liquidation mechanism and risk parameters, LT and LB, perform effectively under stressed market conditions.

Markets

Ethereum

The vast majority of liquidations took place on Ethereum, at over $233M. Since 12 am ET on August 5, we have observed one significant liquidation event primarily affecting WETH, WBTC, and wstETH.

Since that time, liquidations have been more infrequent and smaller in size, in large part because of recovering prices.

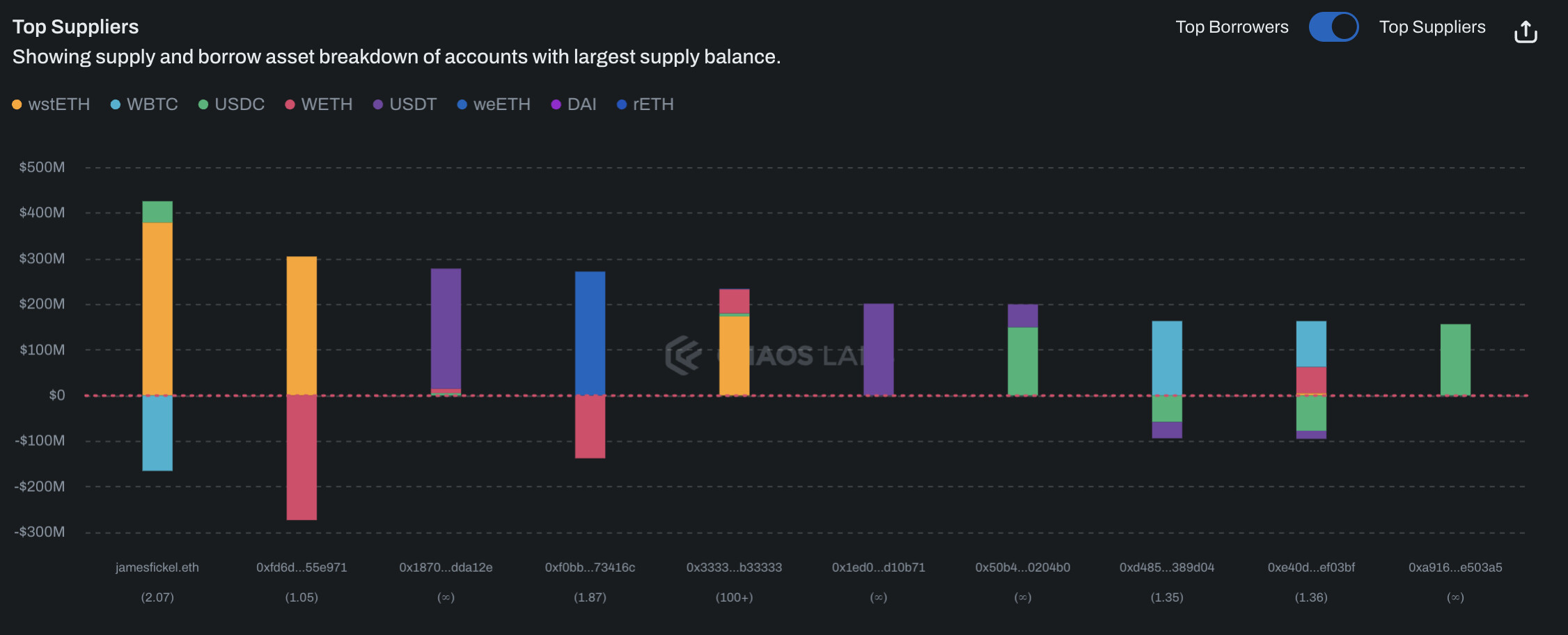

In the most important and highly utilized Ethereum markets, we observe that suppliers maintain mixed health scores. In the WETH market, the largest supplier maintains a health score of 1.41, followed by 1.38 and 2.85. In total, they represent 15% of the total supply. The largest supplier has not adjusted their position since last month’s sell off and does not have any immediately apparent liquidity to improve their health score.

Elsewhere, USDC and USDT utilization has declined significantly, to 76% and 77.5%, respectively, following liquidations of positions with stablecoins as the borrowed asset.

The wstETH market does not show any immediate warning signs, as the largest supplier borrows WBTC but has a health score of over 2. The next largest supplier is looping wstETH and WETH, putting the position at low risk of liquidation given wstETH’s calculated oracle.

Overall, there is currently $255M total collateral at risk on Ethereum.

Base

Liquidations on Base were concentrated with WETH as a collateral asset; given its strong on-chain liquidity these were processed efficiently; liquidations totaled $3.2M.

The top suppliers in this market do not currently present major risks to the protocol, given the top two are supplying and borrowing correlated assets, while those borrowing USDC against WETH maintain relatively strong health scores.

There is currently $1.64M collateral at risk on this deployment.

Arbitrum

Liquidations on Arbitrum were relatively limited relative to the market’s size, and primarily affected WETH collateral positions; liquidations totaled $25M.

There is currently $10.9M collateral at risk on this deployment.

Avalanche

Liquidations on Avalanche were concentrated in the WAVAX, BTC.b, and WETH.e markets, totaling over $5M.

The top suppliers in this market do not currently present major risks, though one position is close to liquidation, with BTC.b and WAVAX as collateral assets.

There is currently $10.25M collateral at risk on this deployment.

Optimism

As on other networks, liquidations on Optimism were concentrated in the WETH market, with WBTC and wstETH also affected.

Some of the top suppliers present liquidation risks, including those with a health score of 1.35, 1.1, and 1.21. However, given their varying collateral and liquidation points, they do not present a major risk to the protocol at this time.

There is currently $2.79M collateral at risk on this deployment.

Polygon

Liquidations on Polygon were limited and concentrated in the WETH market; WBTC and WMATIC positions were also liquidated.

Metis

Liquidations on Metis were minimal, and we do not observe significant risks among the current top suppliers.

There is currently $5.1M collateral at risk on this deployment.

Gnosis

Liquidations on Gnosis were also minimal, almost entirely concentrated in the wstETH market.

The current top suppliers do not pose significant risks to the protocol; the position likeliest to be liquidated maintains a health score of 1.58.

There is currently $6.91M collateral at risk on this deployment.

BNB Chain

Liquidations on BNB Chain were largely concentrated in ETH collateral positions and were generally limited.

The riskiest positions amongst top suppliers are using BTCB as collateral to borrow stablecoins. However, they all have differing health scores, meaning their liquidations would take place at different prices, better facilitating efficient liquidations.

Overall, collateral at risk does not show major risks to the protocol in the BTCB market. There is currently just $850K at risk.

Scroll

Liquidations on Scroll were almost entirely concentrated to WETH collateral positions, and were efficiently processed.

The top suppliers on Scroll present limited liquidation risk at this point; the top five are all looping wstETH and WETH. There is a position with WETH collateral borrowing USDC, for a health score of 1.69.

There is currently $2.04M at risk on this deployment.

Summary

The Aave protocol functioned well during a period of rapid and severe drawdowns in the prices of most crypto assets. Despite the large value of liquidations, no bad debt was incurred. Currently, no deployments are showing major signs of risk to the protocol, though continued liquidations are possible should prices continue to fall. We will continue to monitor all markets and may recommend parameter adjustments should we identify warning signs.