Summary

LlamaRisk supports the proposed pyUSD parameter changes, increasing uOptimal from 80% to 90% and decreasing the Reserve Factor from 20% to 10%, as they do not introduce incremental risks under current market conditions. The pyUSD Supply APR remains unchanged under the proposed changes, while the lower Borrow APR is expected to attract borrowers and slightly raise the pool utilization. We recommend monitoring utilization once PayPal incentives launch, as they could potentially drive borrowing demand, though details of the campaign are not yet available.

Source: LlamaRisk, September 10, 2025

Impact on Yield

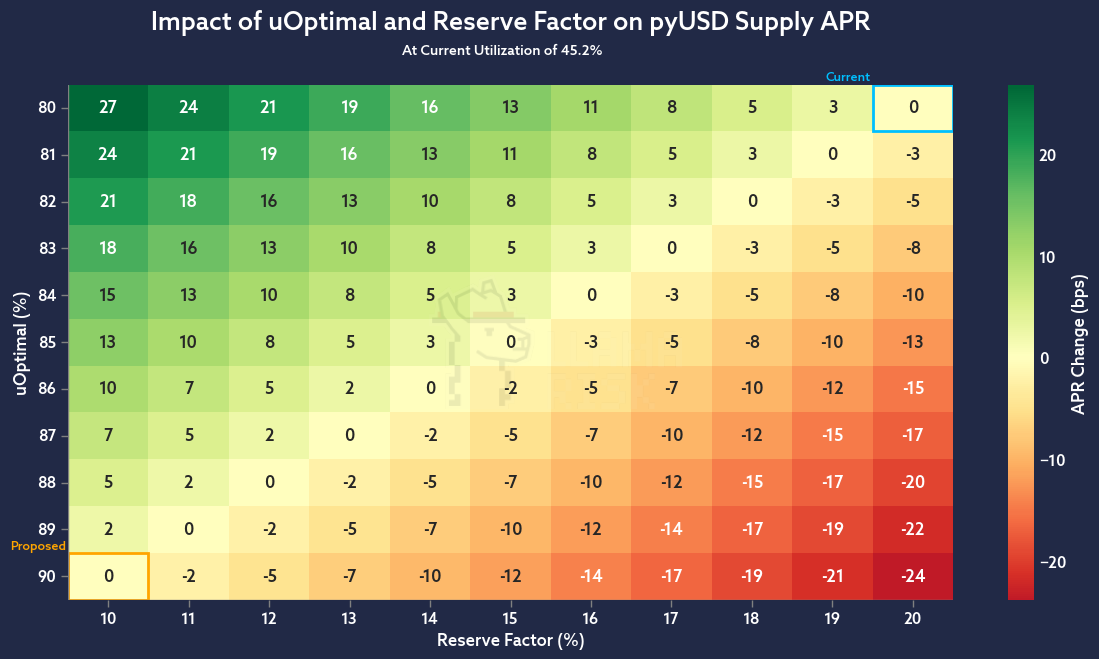

Recently, pyUSD utilization has remained in the 40–45% range. With the proposed increase in uOptimal and decrease in Reserve Factor, the pyUSD Supply APR will remain unchanged. This is because the additional revenue for suppliers from the lower Reserve Factor offsets the decrease in supply APR caused by the higher uOptimal. This is beneficial, as it ensures suppliers continue to receive the same yield without being discouraged from supplying liquidity. Meanwhile, the Borrow APR is expected to decrease by 66 bps, making pyUSD more attractive to borrowers while maintaining the same yield for suppliers. Under current market conditions, the reduction in Borrow APR could attract approximately $0.52M in new borrows, pushing utilization up to around 50% until the Borrow APR returns to its prior level.

Source: LlamaRisk, September 10, 2025

Risks

The risk of increasing uOptimal lies in the lower Borrow APR can lead to a spike in utilization, reducing available liquidity. This diminishes the reserve’s buffer for supplier withdrawals and liquidation execution, potentially increasing market risk. However, given the relatively low utilization of the pyUSD pool, these changes do not currently pose a significant threat. We recommend closely monitoring utilization levels once the proposed PayPal incentives are implemented, as they may or may not discount borrowing costs, potentially causing utilization spikes. However, the information on such a potential campaign remains unavailable.

Another notable impact of the proposed parameters is a significant reduction in DAO revenue, due to the decrease in the Reserve Factor from 20% to 10%, resulting in a 50% decline in revenue from pyUSD amounting to $31.5K annually, assuming utilization remains stable. While the DAO’s revenue halved, the absolute revenue loss in dollar terms may be partially offset if the lower borrow rates successfully increase pool utilization and, consequently, the total interest generated.

Disclaimer

This review was independently prepared by LlamaRisk, a DeFi risk service provider funded in part by the Aave DAO. LlamaRisk is not directly affiliated with the protocol(s) reviewed in this assessment and did not receive any compensation from the protocol(s) or their affiliated entities for this work.

The information provided should not be construed as legal, financial, tax, or professional advice.