Summary

LlamaRisk supports this proposal and the specific parameters proposed by @ChaosLabs.

This measured adjustment supports the initial motivations of mitigating exposure to volatile debt-collateral and hedging against early market uncertainty. The increased risk parameters would serve to meet the demonstrated demand for weETH collateral in stablecoin borrowing and boost protocol revenue.

Following our own assessment, increasing LT and LTV to align with the baseline configuration of weETH on the Ethereum Core instance presents minimal volatility risk; however, reduced DEX liquidity presents potential liquidation bottlenecks.

Market Liquidity

Onchain supply at the time of writing currently stands at 75,599 weETH (~$294M) with 258 holders. Approximately 90% of the supply is allocated to the Aave Plasma weETH contract. Since the proposal’s publication, supply has declined from over 100K (~$460M); however, it remains significant given the chain’s relatively recent launch.

Source: weETH supply on Plasma, Dune, October 10th, 2025

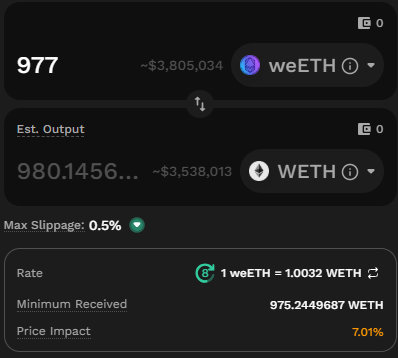

Relative to onchain supply, DEX liquidity is limited: 977 weETH (~$3.8M) can be swapped at 7.5% slippage. This presents a more pessimistic outlook than initially observed. One factor to consider in this respect is the evolving nature of Plasma pools, given the chain’s recent deployment (e.g., the effect of early liquidity incentives).

This presents risks in the event of a significant negative price action, limiting available liquidity to liquidate bad debts.

Source: weETH to WETH, Kyberswap, November 10th, 2025

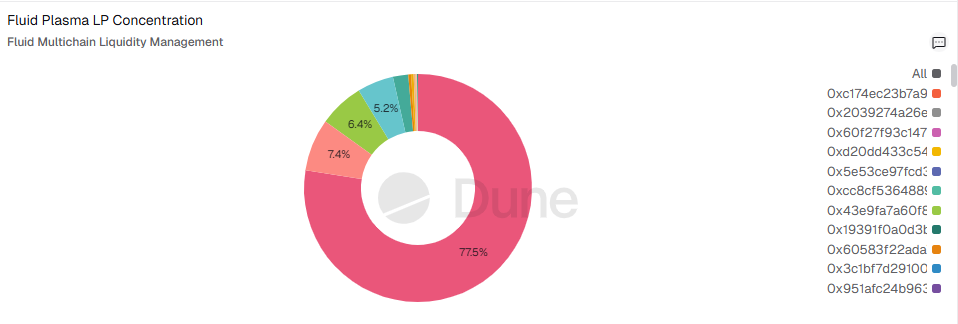

LP Concentration

The largest DEX pool, Fluid weETH/WETH (~$9.27M TVL), currently has a highly concentrated distribution of liquidity providers, with 4 EOAs supplying over 96% of the pool’s liquidity.

Source: Fluid weETH/WETH LP concentration, Dune, October 11th, 2025

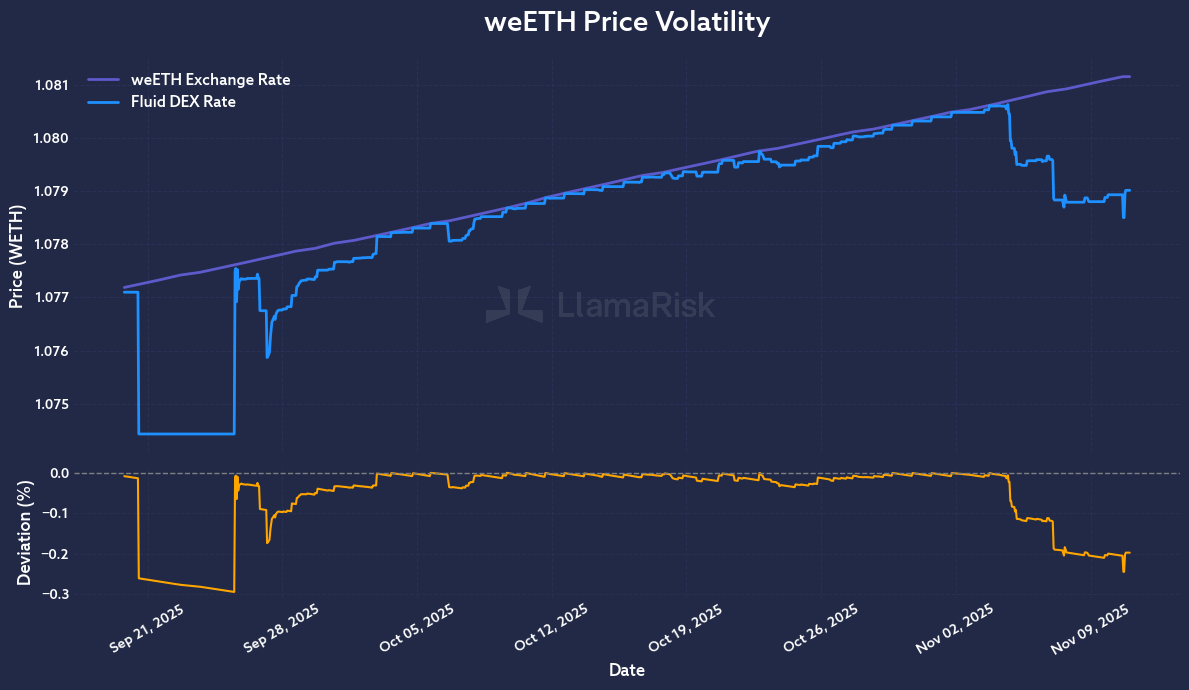

Volatility

When comparing weETH’s DEX rate and internal exchange rate, the secondary market rate has largely followed the internal exchange rate, but has recently been trading at a slight discount. The Plasma deployment has overall exhibited low deviation from the rate.

Source: LlamaRisk, November 11, 2025

Utilisation Considerations

The high utilisation of weETH for borrowing stablecoins indicates a high demand for this use case, and therefore, increased parameters are required. We support the view that greater exposure to weETH and stablecoin borrowing would lead to greater protocol revenue.

Disclaimer

This review was independently prepared by LlamaRisk, a DeFi risk service provider funded in part by the Aave DAO. LlamaRisk is not directly affiliated with the protocol(s) reviewed in this assessment and did not receive any compensation from the protocol(s) or their affiliated entities for this work.

The information provided should not be construed as legal, financial, tax, or professional advice.