ARC: Enable USDT as collateral on Aave V3 (Avalanche)

Summary

This is a proposal to enable native USDT (https://tether.to/en/) as collateral on the Avalanche V3 Market.

Motivation

As far as stablecoins go, both DAI and USDC are currently enabled as collateral and we believe that USDT has a similar risk profile and should not be treated differently. Enabling USDT as an additional option for stablecoin collateral on Aave should help safeguard against the inherent risks of any specific stablecoin failing and increasing diversity. There has been a longstanding view that Tether proposed additional risks that were not present in other stablecoins. In fact, USDT is the longest-standing stablecoin and has met redemptions in strenuous markets in the past.

This specific parameter was never debated in the Aave governance forum and we believe that it would be valuable to start a community discussion around the topic.

In response to any previous controversies surrounding USDT, Tether has taken significant steps towards increased transparency. It should be seen as a positive that USDT & Tether are under heightened scrutiny, as opposed to many other assets and organizations that are not subject to the same extensive disclosure requirements and regularly undergo external auditing.

It is important to note that USDT is the oldest and most widely distributed stablecoin in the market. There have been numerous occasions whereby market conditions deteriorated and Tether was able to satisfy all the necessary redemptions.

Driving factors

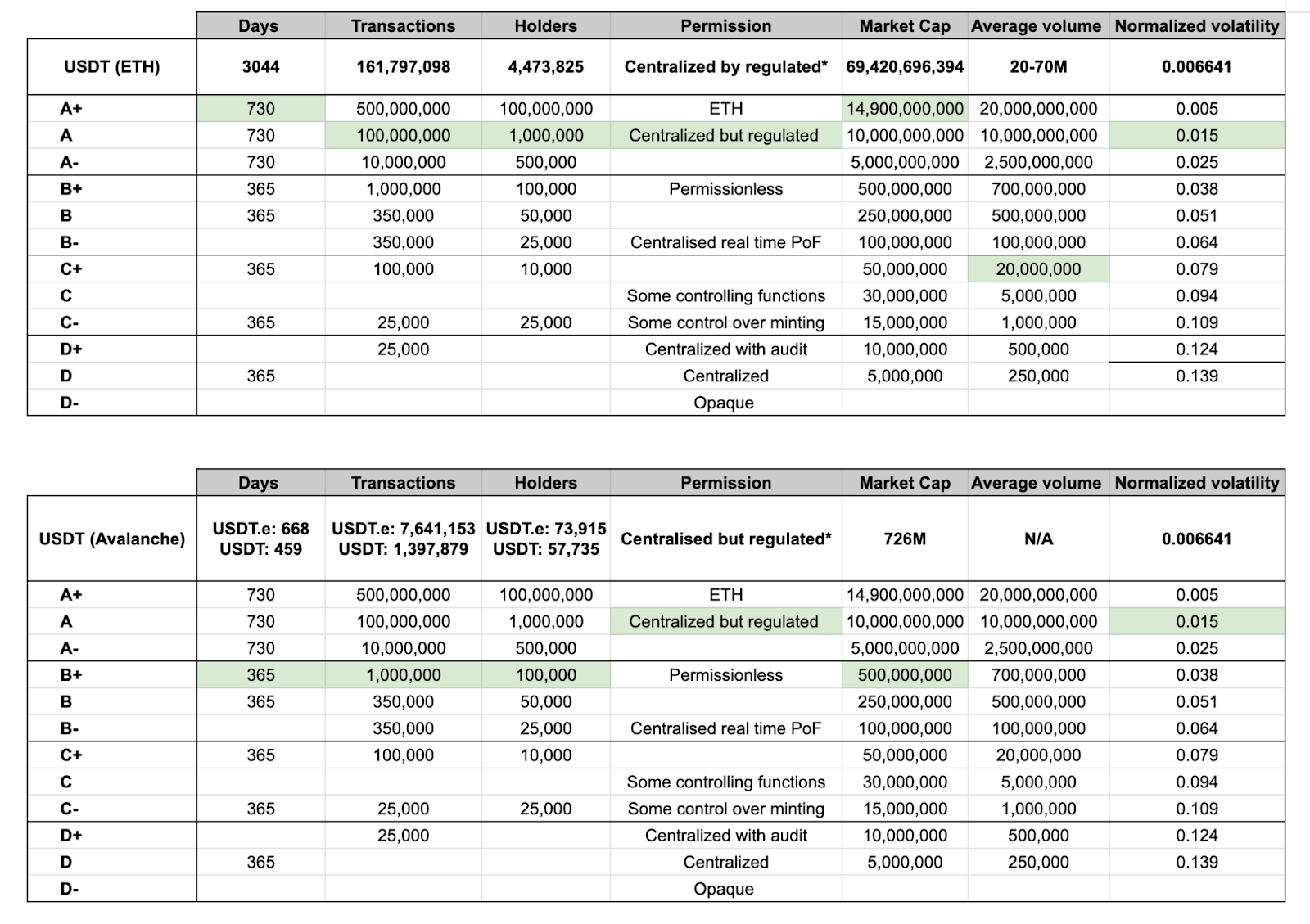

We believe that an objective analysis of the risks associated with USDT shows that it has a similar risk profile to the other stablecoins listed on Aave & enabled as collateral and that there is no reason why it should only be listed in isolation mode.

As a baseline for our analysis, we will use the risk scale provided in the Aave documentation for evaluating new assets (Methodology - Risk):

What is immediately clear is that USDT scores well in multiple areas as it has been around since 2014 and has remained mostly stable throughout its history. It is also widely adopted and transacted across blockchains and remains the stablecoin with the highest market capitalization.

A point of contention could be Tether’s classification as “centralized but regulated”. Tether claims that it is registered as a money services business with the Financial Crimes Enforcement Network (FinCEN). This is admittedly not equivalent to being regulated by entities such as the New York State Department of Financial Services (NYDFS) like other major stablecoins are. Whether this counts as regulated is ultimately up to interpretation and USDT could also plausibly be classified somewhere between “centralized with audit” and “centralized real-time PoF” on the scale above.

Smart contract risk

Tether has undergone multiple smart contract audits by third party security auditing firms:

CertiK audit: Tether - CertiK Security Leaderboard

OpenZeppelin audit: Tether Token Audit - OpenZeppelin blog

While it is never possible to completely rule out smart contract risk, it’s clear that in the case of USDT, this risk is relatively minimal as the asset does not rely on a complex set of smart contracts like a typical DeFi protocol, which significantly reduces the vector of attack.

Counterparty risk

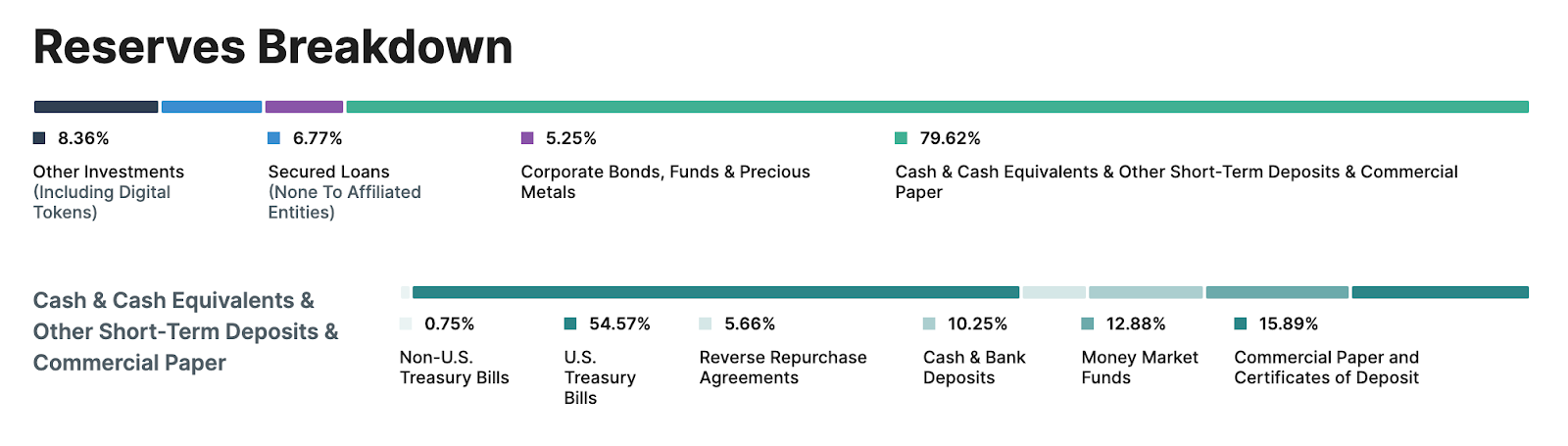

Counterparty risk is arguably the most significant risk factor to consider in the case of USDT. Tether is the only entity through which USDT can be minted and redeemed by corporate customers and exchanges. This is similar to other centralized stablecoins such as USDC. Due to this level of centralization, Tether has taken steps to increase the transparency of its reserve (see reserves breakdown & audits below) and has been regularly audited.

Market risk

USDT is pegged 1:1 to the US dollar. This is guaranteed by the official minting and redemption process. However, most users acquire and trade USDT through centralized & decentralized exchanges. Given how liquidity pools and AMMs work, there have been instances where USDT has depegged, trading at less than $1 for a short period of time before returning to its peg.

Reserves & other disclosures

- Transparency page: https://tether.to/en/transparency/

- Independent audit reports on consolidated reserves:

- BDO: https://assets.ctfassets.net/vyse88cgwfbl/2xJyKdUKicdRUWpC9buRWR/6fe2987698dbbf39b947af718d736ddb/Std_ISAE_3000R_Opinion_30-6-2022_RC134792022BD0303.pdf

- Mha Cayman: https://assets.ctfassets.net/vyse88cgwfbl/1np5dpcwuHrWJ4AgUgI3Vn/e0dac722de3cea07766e05c52773748b/Tether_Assurance_Consolidated_Reserves_Report_2022-03-31__3_.pdf

- Moore: https://assets.ctfassets.net/vyse88cgwfbl/01lZdtaNYx7jZ4jU5xmlYO/90aa0d5b1e3559c393ff135f987ddbd0/tether-assurance-sept-30-2021.pdf

Specifications

-

What is the link between the author of the ARC and the Asset?

- The author of the ARC is a representative of the Ava Labs team.

-

Provide a high-level overview of the project and the token

Launched in 2014, Tether tokens (USDT) pioneered the stablecoin model and are the most widely traded. Tether tokens offer the stability and simplicity of fiat currencies coupled with the innovative nature of blockchain technology, representing a perfect combination of both worlds. USDT is 100 percent backed by Tether’s reserves and Tether tokens have grown in popularity over the past few years, with a market cap of over US$70 billion (as of November 2022). Tether tokens allow customers the ability to transact across different blockchains, without the inherent volatility and complexity typically associated with digital tokens.

- Explain the positioning of the token in the AAVE ecosystem. Why would it be a good asset to borrow or use as collateral?

- USDT is a stablecoin that is fully backed by assets that are considered safe cash equivalents with proper levels of liquidity along with stability. Proof of reserves audits for Tether have been done 4 times in 2022 alone and every audit has passed without a single problem. During times when USDT has strayed away from USD peg, users were easily able to buy discounted USDT and redeem it for cash until there was no longer a discount without any issues.

USDT is already integrated into multiple DeFi protocols within the Avalanche ecosystem such as Trader Joe, Platypus Finance, Pangolin, Benqi, and Paraswap.

-

Provide a brief history of the project and the different components: DAO (is it live?), products (are they live?). How did it overcome some of the challenges it faced?

- Founded in July 2014 by Brock Pierce, Craig Sellars, and Reeve Collins, Tether (USDT) is a stablecoin with the intent of tracking the US dollar one to one. Tether was created as an attempt to solve two major issues with existing cryptocurrencies: high volatility and convertibility between fiat currencies and cryptocurrencies. While the tokens themselves operate in a decentralized network, Hong Kong based Tether Ltd is solely responsible for creating and redeeming tokens as well as maintaining the 1:1 deposit backing. Over the years Tether has been a target for false accusations and controversy regarding the assets USDT, but through every market downturn redemptions have all worked as intended and the asset has always restored peg. Within the past year Tether has started to be much more open regarding the assets that back USDT and has had multiple audits performed.

-

How is the asset currently used?

- Currently, there is about $72M of bridged USDT.e from Ethereum blockchain to the Avalanche ecosystem and $651M of natively minted USDT on Avalanche. The asset currently is integrated into almost every DeFi application from stableswaps like Curve and Platypus, to AMMs like Trader Joe, Pangolin and GMX as well as lending protocols like Benqi, Aave and Joe Lend. The asset is a staple ingrained into the Avalanche network and is one of the most important tokens within every ecosystem.

-

Emission schedule

- No emission schedule

-

Token (& Protocol) permissions (minting) and upgradability. Is there a multisig? What can it do? Who are the signers?

- Tether tokens exist as digital tokens built on several leading blockchains, including Algorand, Avalanche, Bitcoin Cash’s Simple Ledger Protocol (SLP), Ethereum, EOS, Liquid Network, Omni, Polygon, Tezos, Tron, Solana and Statemine. These transport protocols consist of open source software that interface with blockchains to allow for the issuance and redemption of Tether tokens. Every Tether token is 100% backed by Tether’s reserves, which includes traditional currency and cash equivalents, and may include other assets and receivables from loans made by Tether to third parties. The Tether platform is fully reserved when the sum of all Tether tokens in circulation is less than or equal to the value of our reserves. Through our Transparency page, anyone can view both of these numbers on a daily basis. Tether tokens (USDT) are created by having multiple Tether private authorization keys sign and broadcast creation transactions on the specific blockchain. These new tokens are “authorized but not issued”, meaning that these USDT are stored in Tether’s treasury and not in circulation until issued in response to market demand. Tether’s multi-signature (or multi-sig) model prevents a single person from issuing USDT on their own, which would represent a single point of failure and a security risk. Tether tokens enable businesses – including exchanges, wallets, payment processors, financial services and ATMs – to easily use fiat currencies on blockchains. Some of the largest businesses in the digital currency ecosystem have integrated Tether tokens.

-

Market data (Market Cap, 24h Volume, Volatility, Exchanges, Maturity)

- Market Cap: $70B ($723M on Avalanche)

24 Hr Volume: $59B (CEX & DEX) with around a volume of $8M on Avalanche

Exchanges: Trader Joe, Curve, Platypus Finance, GMX, and Pangolin

CoinGecko: Tether Price in USD: USDT Live Price Chart & News | CoinGecko

CoinMarketCap: Tether price today, USDT to USD live, marketcap and chart | CoinMarketCap

- Social channels data (Size of communities, activity on Github)

- Twitter: 303k followers (https://twitter.com/Tether_to)

Telegram: 7.5k members (Telegram: Contact @OfficialTether)

- Contracts date of deployments, number of transactions, number of holders for tokens

- Date of deployment: June 2021 for Ethereum bridged USDT.e on Avalanche and December 2021 for native USDT on Avalanche

The number of transactions: 9M

The number of holders: 132,000 on Avalanche

Proposed technical parameters

- Usage as collateral: Yes

- LTV: 70%

- Liquidation threshold: 80%

- Enabled to borrow: Yes

- Stable rate enabled: No

- Liquidation bonus: 5%

- Reserve factor: 10%

We look forward to discussing this proposal with the Aave community and strongly encourage you to contribute to the discussion and provide feedback. We will be posting a vote on snapshot in 7 days to evaluate the community’s sentiment on this proposal.

References

- Tether’s website: https://tether.to/en/

- Tether transparency page: https://tether.to/en/transparency/

- Coingecko: Tether Price in USD: USDT Live Price Chart & News | CoinGecko

- Coinmarketcap: Tether price today, USDT to USD live, marketcap and chart | CoinMarketCap

- CertiK audit: Tether - CertiK Security Leaderboard

- OpenZeppelin audit: Tether Token Audit - OpenZeppelin blog