TLDR

In this post we:

- Show how conservative Aave v3 liquidation thresholds are. We show how it changed over time, and compare it to Compound v3 configurations.

- Compare LTV for different lending pairs as a time-dependent protocol parameter

- Explore different LTV-Borrow Cap pairs and provide tools for active risk management

- Compare Aave v3 to Compound lending markets

- Enhance the huge role that DEX liquidity is playing in the selection of LTV values

- This is done by extending The RiskDAO research for calculating liquidation thresholds and apply to Aave Lending Markets

*This work was a collaboration between Block Analitica and RiskDAO. All authors contributed equally.

Introduction

Deciding on liquidation thresholds comes with few assumptions on how the market will behave in difficult times. These assumptions could include:

- User behavior in a downtrend market.

- Behavior of DEX liquidity in the presence of liquidations.

- Volatility amplification during black swan events

- And more (some of the assumptions have additional sub-assumptions on specific simulation parameters).

In a recent study, the RiskDAO presented a simple formula for calculating liquidation thresholds. This formula takes into account market parameters and a single confidence level factor. This factor aims to represent all the implicit and explicit assumptions with a single number.

In this work, we extend the research and apply it for Aave markets. Our contribution is twofold:

- We extend the methodology and calculate the confidence level factor for Aave markets.

- We compare the confidence level to Compound, and show how these values changed over time (as market conditions have changed).

The outline of this post is as follows. Firstly, we focus on the Price Volatility to be used as input, comparing Parkinson’s volatility estimator with simple Standard Deviation. Next, we concentrate on the confidence level, denoted by c, as a time-dependent parameter, and explore how it can assist us in defining Loan-To-Value (LTV) Ranges of confidence. To benchmark our work, we utilize the WETH-DAI lending pair, which is the most established lending market in DeFi. Finally, we continue our work with a couple of simulations that we believe will be helpful for risk managers in defining LTV and Borrow Cap pairs for any lending protocol. Finally, we compare the c parameter across different Lending Protocols, and enhance the huge role that DEX liquidity is playing in the selection of LTV values.

The confidence level

In their work, RiskDAO proposes a simple formula to determine LTV by means of readily available on-chain data:

where 𝝈 is the annualized price volatility ratio between collateral and debt, β is the liquidation bonus, ℓ and d are the available liquidity and the borrow cap of the debt, respectively, and c is the confidence level factor. It is important to note that for higher values of c the chances of insolvency decrease, and vice versa.

From our perspective, this formula introduces a crucial parameter for risk management to the ecosystem: the confidence level factor, denoted as c. The value of c depends on the risk appetite, but can also depend on qualitative properties of the collateral/debt pair (e.g., centralization risk). Hence, not all lending pairs are equal, necessitating the establishment of a benchmark for c using a well-understood lending pair with underlying assets.

Methodology

The RiskDAO’s formula allows flexibility in the choice of price volatility and whether the focus should be on liquidation events or the time-dependent evolution of returns. Both decisions are challenging. On one hand, using the LTV formula implies that price volatility serves as the primary market indicator for risk management, warranting stress testing in all market conditions.

The choice between focusing on liquidations or the time-dependent volatility over the past years depends on the stage of backtesting and stress-testing of the model. Gathering data to backtest the model can be particularly challenging due to the occurrence of most liquidations during Black Swan Events. Therefore, as an initial approach, we will concentrate on the time-dependent returns and volatility of ETH, WBTC, UNI, DAI, and LINK over the past few years. Additionally, we propose the use of the annualized Parkinson Volatility as an estimation for the price volatility of assets.

This section is divided into four parts. First we will study price volatility for ETH, WBTC, UNI, DAI and LINK, and explore the difference between standard volatility and Parkinson volatility as a risk management tool. In the second part, we will take a look into c and we will construct the boundaries that will determine LTV values for the benchmark lending market ETH-DAI. In part three we perform simulations to show the stark differences between LTV ranges due to factors like Liquidity and Borrow Cap. Finally we take a deep dive into on-chain liquidity data and compare the confidence level factor of different lending markets in Compound and Aave v3.

Price Volatility

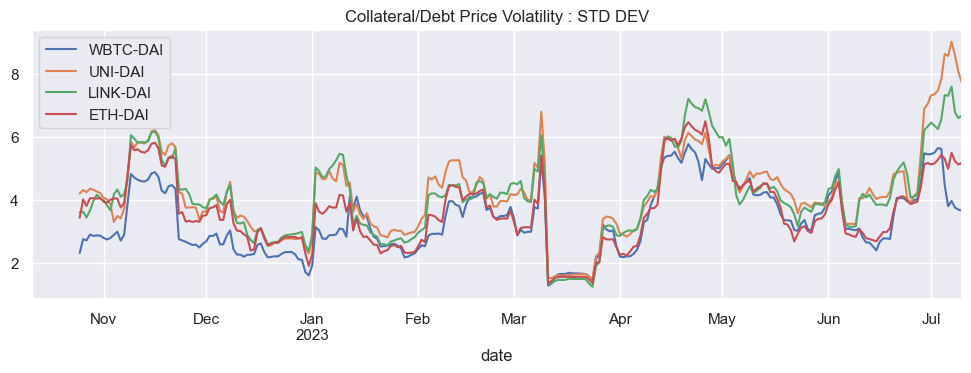

It is evident that lower market cap assets like UNI and LINK have different volatility fingerprints than the more established assets ETH and WBTC. This greater volatility is due to different factors like liquidity. The simplest estimator of volatility is the close-to-close realized standard deviation on a rolling window, however, a big chunk of price information is not taken into account. Thinking about risk management, we estimate the price volatility of ETH, WBTC, UNI, DAI and LINK, by means of the Parkinson Volatility over a period of 360 days, using the annualized daily returns, selecting a 14 day rolling subperiod to reduce variance. We further normalize the sample using the collateral-to-debt ratio assuming that the borrower will always acquire debt in DAI when posting collateral. The results are shown by Fig. (1).

Fig. (1). Time-dependent Collateral/Debt Price Volatility for different Lending Pair Markets. UP: Simple close-to-close standard deviation. DOWN: Parkinson Volatility estimator.

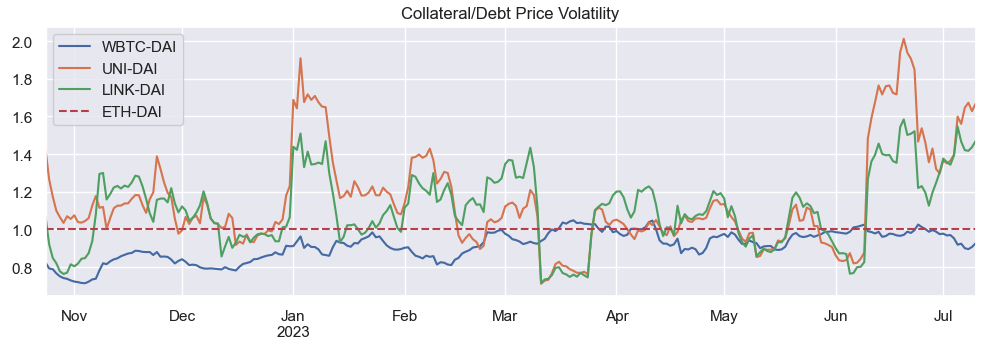

From FIg. (1) it is evident that even though UNI and LINK have clearly more dispersion, by using the Parkinson Volatility we reduce noise in the sample and we standardize the volatility into a tighter range. To simplify the interpretability of the graph above we can benchmark volatility by means of the Price Volatility of WETH-DAI, the most common lending market in DeFi, by simply dividing, as shown in Fig. (2).

Fig. (2). Time-dependent Collateral/Debt Price Volatility for different Lending Pair Markets using the Parkinson Volatility estimator and benchmarking using WETH-DAI.

Confidence Level Factor

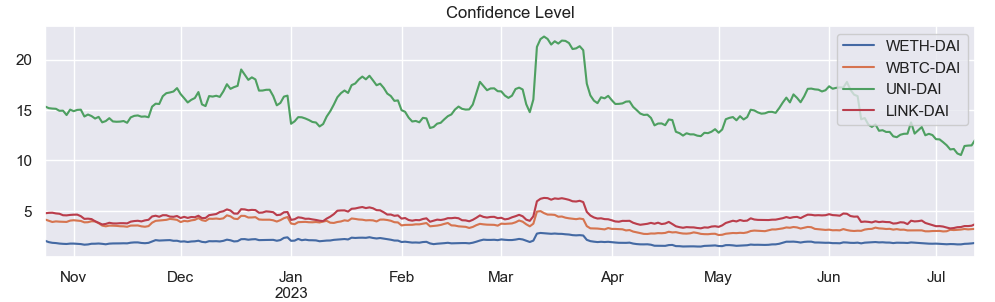

Next, we demonstrate how the ETH-DAI lending market establishes a benchmark for the confidence level by simulatiing its historical behavior on Aave v3 Ethereum market. We accomplish this by utilizing the aforementioned formula and considering time-dependent Price Volatility, as illustrated in Figure (3).

Fig. (3). Time-dependent Confidence Level Factor for different Lending Pair Markets using the Parkinson Volatility estimator and benchmarking using WETH-DAI. For simplicity all data for Borrow Cap, Liquidity and Bonus is constant and was taken from the current Aave v3 Ethereum set parameters. A higher confidence value implies that the LTV configuration is more conservative.

Back to LTV. Finally, considering the time-dependent evolution of the c factor for WETH-DAI, we revisit the formula and establish the LTV ranges based on cmax and cmin. It is crucial to note that the inverse relationship between c and LTV implies that cmax will determine the lowest LTV, and vice versa. This reverse engineering process is shown in Figure (4).

Fig. (4). Time-dependent Loan-To-Value for the ETH-DAI lending market. For simplicity all data for Borrow Cap, Liquidity and Bonus is constant and was taken from the current Aave v3 Ethereum set parameters

LTV - Borrow Cap simulations

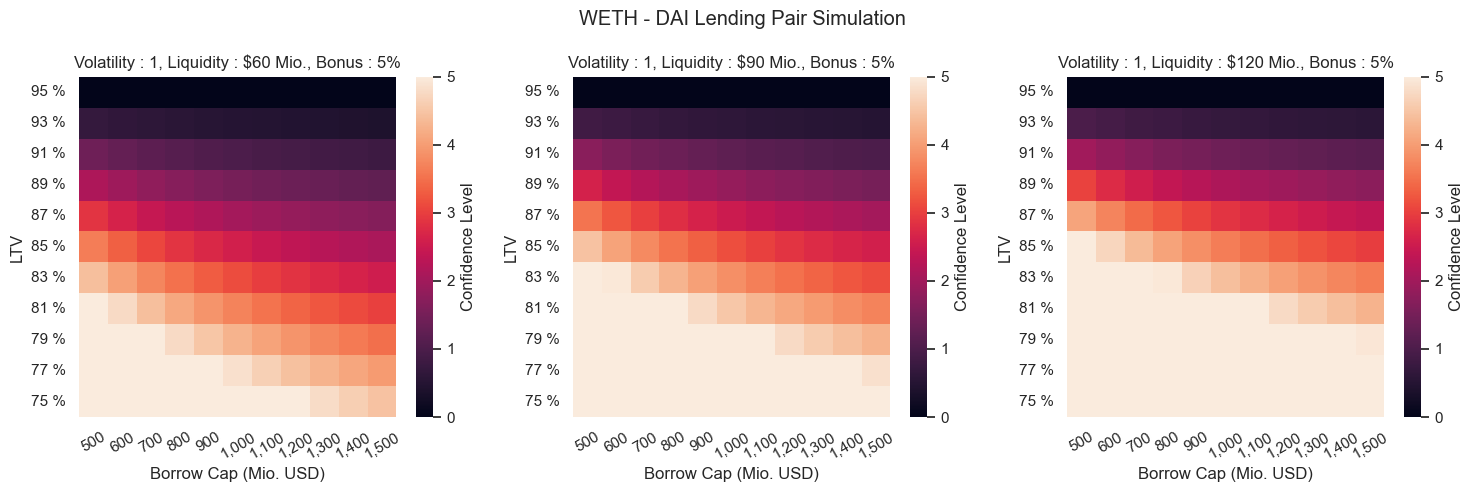

Now we focus on a simple simulation to show how different (LTV, Borrow Cap) pairs affect the values of the c factor. For the sake of simplicity we divided price volatility by the benchmark ETH-DAI. Results are shown in Figure (5).

Fig. (5). LTV,BC simulation for the WETH-DAI lending market. For we divided price volatility by the benchmark and kept Bonus constant. In this exercise, we observe how Liquidity affects confidence level factor c.

As mentioned by RiskDAO, we show that the LTV formula enables a decision on c instead of LTV. This process entails that, given a confidence level value, a smart contract could autonomously determine the LTV ratio of assets and dynamically adjust it over time. This process will reduce decision-making overhead and facilitate the emergence of an automated and permissionless lending market.

Historical DEX Liquidity

As illustrated in our simulations liquidity plays a huge role when choosing the confidence level factor. Needless to say, liquidity is not constant, therefore we compare on-chain liquidity* over time for some of the most liquid collateral tokens at Aave v3 Ethereum. To calculate asset liquidity we simply get the USD amount that an asset can be sold at a slippage equal to the asset’s liquidation bonus 𝛽. Then we normalize those values with their mean and smooth the results by using a 14 day rolling window.

Fig. (6). Normalized asset liquidity over time for some of the most liquid borrowable assets at Aave v3 Ethereum

Figure (6) exhibits that liquidity can be volatile over time even for these tokens. In the case of ETH we can see that liquidity moved from 60% to 150% of average in the last 18 months.This is even more extreme for WBTC and LINK. These results showcase the complexity of the problem at hand, and highlight the need for dynamical monitoring and revision of LTV values.

Confidence Level across different Lending Protocols

Finally, we compare Aave v3 Ethereum and Compound v3 markets using the LTV formula based on empirical data. Given the current market state, we can quantify the c factor for the same assets across the chosen protocols and for different assets within the same protocol.

Fig. (7). Comparison of computed c factors for chosen assets across Aave v3 Ethereum and Compound v3

The chart above shows that the c-factors are mostly aligned across the two protocols. However, there is a slightly more conservative approach at Aave with LINK and WETH with much more conservative approach with UNI.

Conclusions and Future Work

With this work tackle a multivariate and complex problem using a straightforward quantitative approach. Needless to say, choosing LTV values is a difficult task, but we could conclude that Aave is in general more conservative than Compound. We should also highlight that our research unveils the need for a more dynamic and proactive monitoring and risk management of the protocol, which will help improve user experience and revenue.