stETH Risk Assessment

Summary

Lido allows users to earn staking rewards on the Ethereum beacon chain without locking Ether or maintaining staking infrastructure. This is done through the stETH token. stETH tokens represent a tokenized staking deposit and can be held, traded, or sold.

Onboarding stETH to Aave would allow users to lend and borrow against stETH.

Motivation

There is strong interest in using stETH to earn additional yield with minimal IL risk. This is evident through the growth of the stETH/ETH pool on Curve Finance, which has become the 2nd most liquid pool on Curve with liquidity of $1.8 billion.

The addition of stETH on to Aave can work to attract a larger audience to both Aave and Lido. More ETH staked with Lido would subsequently benefit the decentralization and security of the Ethereum network, to the benefit of the community as a whole. stETH would likely bring new borrow demand to Aave as market participants look to borrow against their staked ETH or lend their stETH for a yield.

stETH Overview

Lido launched in December 2020. Lido allows users to deposit ETH and receive stETH. The deposited ETH is then pooled and staked with node operators selected by the Lido DAO. stETH represents the user’s staked ETH balance of the beacon chain along with staking rewards accrued or penalties inflicted on validators in the beacon chain. When transactions are enabled on the beacon chain, stETH can be redeemed for unstaked ETH and accumulated rewards.

stETH as DeFi collateral is beneficial for a number of reasons.

- stETH is almost as safe as ETH, price-wise: barring catastrophic scenarios, its value tends to hold the ETH peg well;

- stETH is a productive, yield-generating asset;

- stETH is a very liquid asset with over $1.8 billion in liquidity locked in the Curve stETH/ETH pool.

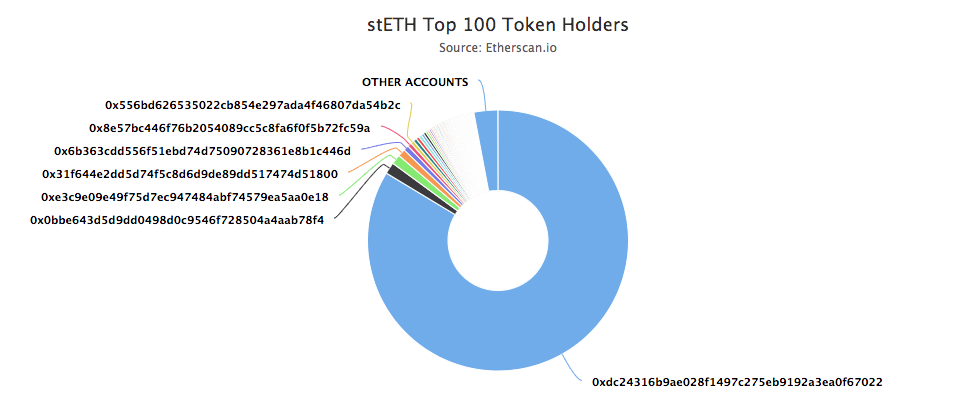

The current stETH supply stands at 309,075 - worth $1.1 billion using current stETH prices. stETH is held by 5,467 unique holders.

The Lido DAO consists of, amongst others, Semantic VC, ParaFi Capital, Libertus Capital, Terra, Bitscale Capital, StakeFish, StakingFacilities, Chorus, P2P Capital and KR1, Stani Kulechov of Aave, Banteg of Yearn, Will Harborne of Deversifi, Julien Bouteloup of Stake Capital and Kain Warwick of Synthetix.

The Lido treasury has been recently diversified and DAO members now include Paradigm, Three Arrows Capital, DeFiance Capital, Jump Trading, Alameda Research, iFinex, Dragonfly Capital, Delphi Digital, Robot Ventures, Coinbase Ventures, Digital Currency Group, The LAO and angels.

Audit

Lido has been audited by Sigma Prime, Quantstamp, and MixBytes (see Audit / Relevant Links).

Liquidity & Volumes

stETH is primarily traded on Curve’s stETH/ETH pool.

- The pool currently holds $1.8 billion of stETH and ETH.

- 82.5% of the stETH supply is in the Curve pool.

The price of stETH has remained relatively stable since launch in December 2020 ranging from a low of 0.94 to a high of 1.02 ETH. Initial instability arose due to relatively large withdrawals from Curve which disrupted the peg.

As liquidity in the stETH/ETH pool increased, we have seen more stability in the stETH peg.

Integrations

stETH is currently integrated across the following platforms:

- Curve Finance

- ARCx

- Yearn Finance

- SushiSwap

- Harvest Finance

Risk Assessment

Lido faces smart contract risks. To mitigate these, Lido has been successfully audited three times - by Quantstamp, Sigma Prime, and MixBytes (see Audits).

Lido is a DAO. Decisions in the Lido DAO are made through proposals and votes - community members manage protocol parameters, node operators, oracle members and more. The Lido staking infrastructure for stETH consists of 9 node operators, with a focus on decentralization.

Lido relies on a set of oracles to report staking rewards to the smart contracts. Their maximum possible impact is limited by the recent upgrade, and the operators of oracles are all well-known entities including Stakefish, Certified One, Chorus, Staking Facilities and P2P.

stETH is the most liquid staked ETH primitive with a $1.1 billion marketcap and $1.8 billion of liquidity in the Curve Finance stETH/ETH pool. 82.5% of the stETH supply is in the Curve pool. The pool facilitated $60MM+ in 24 hour trading volume.

stETH faces staking risks, specifically validator risks including slashing and hostage risks. To mitigate these, Lido works only with best-in-class validators with a track record of success. In addition to this, staked ETH with Lido is protected from slashing using the Unslashed Finance insurance protocol. At the time of writing, Lido is covered for 5% slashing on more than 400,000 ETH staked until June 22nd. To date, no slashings have been incurred.

To mitigate withdrawal risks, Lido staking went live on December 18th through a withdrawal key ceremony. Chorus One, Staking Facilities, Certus One, Argent, Banteg (yearn.finance), Alex Svanevik (Nansen), Anton Bukov (1inch), Michael Egorov (Curve/Nucypher), Rune Christensen (MakerDAO), Will Harborne (DeversiFi) and Mustafa Al-Bassam (LazyLedger) came together over a four-day event to generate threshold signatures for Lido’s withdrawal keys in a secure environment on air-gapped machines. Lido plans to move over to a fully non-custodial solution in the near future.

stETH is not traded on CEXs and thus the oracle has to use the Curve pool price and ETH price feed to determine the current price. Lido is working on its own price feed which is expected to launch in the next 2 weeks. Lido is also working with Chainlink to release an stETH price feed.

Proposed stETH Risk Parameters

- LTV: 70%

- Liquidation Threshold: 75%

- Liquidation Bonus: 5%

- Reserve Factor: 10%

A LTV of 70% is slightly higher than the 56% average LTV across non-stablecoin assets and 10% lower than ETH’s 80% LTV. This gives the protocol more room to safely liquidate stETH with a volatility profile similar to ETH.

Interest Rate Model:

UOptimal: 65%

Base: 0%

Slope 1: 8%

Slope 2: 100%

Relevant Links

Should stETH be added to Aave v2 with the proposed risk parameters?

- Yes

- No

- Yes, with different risk parameters