Authors from Llama: @MatthewGraham, @AcceleratedCapital, @ahuja and @gmoney

Introduction

This document is intended to outline objectives, constraints, and governance mechanisms for the Aave treasury. It will serve as a strategic guide that:

- Plans for appropriate asset allocation and implementation (e.g. governance, constraints, manager selection).

- Establishes accountability.

- Offers an objective course of action to be followed during periods of market disruption when instinctive responses might lead to less prudent actions.

Having a governance document like this is vital to the success of the capital management program of a DAO. Since they are typically less structured and decision-making is community-driven, having guidelines can help the community assess new strategic decisions based on already agreed upon terms. This proposal will serve as the initial draft, but it should be noted that it is a living document, subject to change with the circumstances of the Aave treasury. It should be viewed as a guide of best practices, and amendments should be adopted by the community prior to making a capital decision in order to ensure the framework is properly considered.

Definition and Structure

These guidelines govern the investments associated with the Aave Protocol. It shall apply to the assets tracked by the Dune Dashboard here.

The Aave community is responsible for approval of and updates to this forum post. It is recommended that the Aave community maintain a DAO/Working Group/Committee dedicated to issues related to these guidelines, including identifying the need for updates and monitoring the portfolio of assets/strategies for compliance with these guidelines.

Governance

The Aave Treasury Management Committee (TMC) should meet quarterly to review these guidelines in light of prevailing circumstances. At these quarterly meetings, an opportunity should be made for the community to propose changes to these guidelines.

The TMC will be responsible for proposing policies to the Aave community that are suitable for achieving the strategic objectives listed below. When necessary, the TMC can identify and engage with outside advisors to help on strategic proposals, review the investment policies, and make recommendations to the community.

In order to keep the community apprised of the performance of the TMC, regular reporting on the investments held by the treasury will be provided. A monthly accounting of positions, calculation of performance relative to any applicable benchmarks, and any additional information necessary to inform the community members of the treasury’s progress will be made.

Investment Objective

The investment assets of the Aave Treasury are intended to:

- Preserve capital and fund ecosystem growth.

- Generate a total return sufficient to preserve the protocol in any market environment.

- Reduce the idiosyncratic risk of the concentrated AAVE position while maintaining exposure to the upside of the protocol.

To fulfill these objectives over the long term, the investment portfolio should seek to achieve a total rate of return in excess of operational expenses. This will ensure protocol longevity, provide flexibility on operations, and protect the purchasing power of the Protocol’s assets.

Time Horizon

The Aave Protocol, like other institutional investors (e.g. pension funds, sovereign wealth funds, endowments, foundations), has an infinite time horizon. The Treasury exists to serve the Aave ecosystem in perpetuity.

The investments held by the Aave Treasury should be made with a long-term perspective. As such, short-term investment performance shortfalls are not necessarily of critical interest unless they suggest failures in strategy execution.

Liquidity Constraints

The Aave Treasury’s liquidity constraints will be subject to ongoing operational expenses. As a best practice, it is recommended that the total allocation to illiquid investments (e.g. token lock-ups) remain below 50% of the investment portfolio, in line with the average endowment allocation to illiquid alternative investments. We would expect illiquidity to remain much lower than this maximum given the nature of DeFi.

In addition, we would recommend that at least 10% of the value of the treasury should be invested in assets that can be quickly liquidated without any significant adverse impact in value as a result of the liquidation (e.g. stablecoins).

Leverage Constraints

Since one of the goals of the Aave treasury is to maintain concentration in the native governance token, strategies will likely employ debt by borrowing stablecoins and other assets against AAVE. For this reason, it is necessary to identify specific metrics for managing risk when deploying leverage.

- Health Factor - Health Factor is crucial when determining liquidation risk. The Aave treasury should elect to manage any investment with a conservative Health Factor that has a very low chance of liquidation during periods of market volatility. A target health factor band will be presented with each investment proposal along with specific capital management practices necessary to ensure the Health Factor is maintained during a range of market conditions.

- Interest Coverage Ratio - Ideally all strategies are positive carry. However, each strategy will be considered both in isolation and holistically within a broader portfolio.

- Derivatives - The use of derivatives is intended to balance out the overall risk exposure of the portfolio. For example, hedging the downside risk of the Aave position with a put option could lower liquidation risk in the event of a severe downturn.

Metagovernance

Where possible, the Aave Treasury should exert the right to contribute to the value of Aave’s investments by participating in constituent protocol governance. The TMC will advise the community on metagovernance proposals when particularly applicable to the value of the Treasury’s investments.

Risk Management

The risk management framework for the Aave treasury will be considered holistically. Capital management decisions will take into consideration various external risks that any treasury faces, along with those external risks specific to the crypto ecosystem. In this section, a risk overview is provided along with a framework for managing both DeFi-specific and portfolio management related risks.

Risk Overview

- Credit Risk - This type of risk is specific to off-chain collateralized stablecoins but can also be present anytime there are assets being delegated to or managed by a counterparty. We intend to perform internal monitoring specific to any credit risks that may arise during the treasury management process.

- Market Risk - Market risk is inherent in any investment that trades freely on secondary markets. As discussed in the portfolio construction section, market risk will be managed within the portfolio construction framework with the goal of working toward the strategic asset allocation outlined below.

- Liquidity Risk - Liquidity can be a risk during periods of network congestion or in the event liquidity is needed but not available for operational expenses. Thorough liquidity analysis will be performed when determining if a strategy is suitable for the Aave treasury.

- Infrastructural Risk - Crypto assets have varying levels of infrastructural risks related to the Ethereum network and smart contracts. When the Ethereum network is clogged during periods of volatility or use, an asset may lose its liquidity since transactions cannot be processed in a timely manner or may be cost-prohibitive. Smart contract exploits (e.g., inflation of the stablecoin via exploitation of a minting function), use of admin keys, oracle risk, and more can all destroy the value of an asset.

Identifying and Managing DeFi-Specific Risk

In addition to the broad risks outlined above, there are also DeFi-specific risks to assess and manage when deciding on allocating capital to a particular strategy. Below are some DeFi-specific risks along with recommendations on handling them:

- Smart Contract - This risk is well known within crypto and the most widely accepted measure for measuring this risk is the combination of a high Total Value Locked (TVL) in the contract for an extended duration of time. This acts much like a bounty as a reward for anyone who can drain the funds. Past performance of similar contracts can be used as a proxy for assessing risk. Audits mitigate some risks and insurance can offset financial loss at a price.

- Admin Keys by protocols - Ideally, the treasury should steer clear of any protocol with admin keys. The only time it’s really acceptable is early on in a protocol’s life. If a protocol has admin keys, there should be a timelock in place before changes made by admins go into effect to limit potential risks.

- Oracle Risk - Widely trusted and proven oracle feeds are strongly preferred. Oracle exploit is one of the most frequent exploits within DeFi. We would want to ensure any investment that utilizes (particularly derivatives) oracles are set up with secure price feeds/data. For example, an options protocol using an ETH price feed for options pricing needs to use an oracle pulling ETH pricing from multiple exchanges; otherwise a bad actor could manipulate ETH price on one source exchange and impact the entire options market.

- Closed source protocols - Ensure that protocols we utilize are open source so that contract code can be easily inspected.

All investments and strategies are to undergo a risk assessment whereby each of the above risks are investigated and taken into consideration. Any known risk is to be clearly articulated in any proposal to the Aave community.

Portfolio Construction Framework

The goal of the asset allocation is to maximize the portfolio return relative to a predetermined level of risk with consideration given to the following core functions:

- Offset the risk profile of the existing Aave position by reinvesting generated capital into a diversified portfolio of less correlated and less volatile assets.

- Maximize total return relative to volatility of the return. This is done through diversification and also deployment of capital into productive assets (e.g., aTokens).

- Utilize derivatives where applicable to modify risk exposures to suit the needs of the Aave Treasury.

- When deploying assets productively, each additional layer of smart contract risk will be examined in an attempt to minimize contagion within the portfolio of assets.

Individual investments will be assessed for their impact on the total portfolio’s risk/return characteristics, rather than on the individual investment’s specific characteristics in line with Modern Portfolio Theory. For example, a high-risk investment isn’t necessarily precluded from a conservative, low-risk portfolio as long as it is properly within the total portfolio’s risk budgeting constraints. Oftentimes, assets of varying risk when combined actually reduce overall risk.

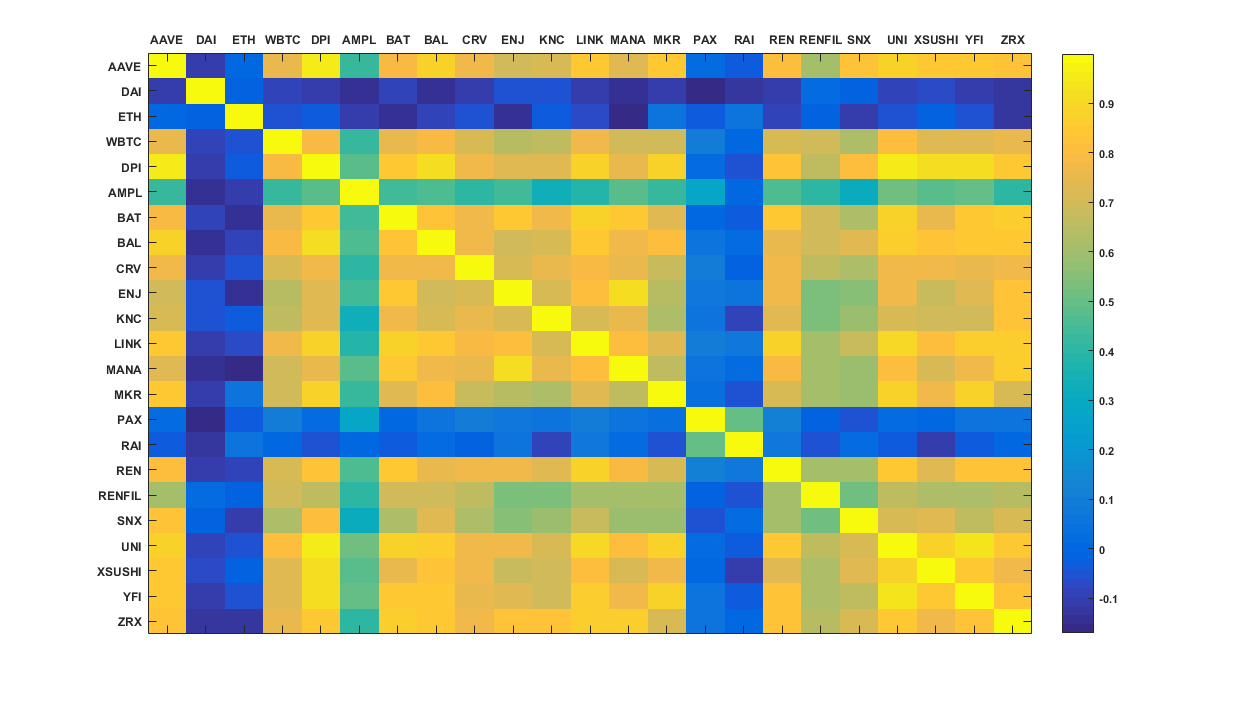

Since it is likely Aave will be implementing a strategy of borrowing against the native AAVE token to build a productive and diversified portfolio, it is helpful to understand the correlation of assets relative to the AAVE token. Below is the correlation of return from the assets currently supported on Aave. These correlation values are determined based on daily returns in the past 3 months. We use all of the price history available since the launch of the shortest lived token i.e. KNC. Monthly returns may be used to suppress daily fluctuation-related noise and better isolate the signal of interest i.e. correlation of returns. However, we are limited by the small amount of price/return history currently available. Note that DAI is used as a proxy for all stable coin assets supported on Aave (DAI, GUSD, USDC, USDT, BUSD, SUSD, TUSD).

Figure - Correlation matrix to capture correlation of returns of all assets supported on Aave. Historical returns used in analysis are limited by the project with the shortest history.

Strategic Asset Allocation

The asset allocation will be determined by considering where individual assets fall into a risk spectrum as identified here:

Using the framework above, we propose the following long-term strategic targets for the diversified portfolio separate from the concentrated AAVE position:

- Low Risk (50%)

- Per the correlation matrix above, the most immediate benefit to the Aave treasury is the introduction of a stablecoin allocation.

- The stablecoin allocation can be productively deployed throughout DeFi to generate a yield.

- If Aave elects to borrow against the AAVE token, it makes sense to primarily borrow stablecoins due to their lower risk profile. If these stablecoins are then deployed throughout DeFi, the Aave treasury would essentially be creating a collateralized debt position.

- Medium Risk (30%)

- The medium risk bucket is composed of assets that will typically be highly correlated to the AAVE token given the high correlations of assets in the crypto ecosystem.

- The goal of the medium risk bucket is to gain exposure to large-cap, high-quality crypto assets while helping to diversify some of the specific idiosyncratic risks of the AAVE token.

- High Risk (20%)

- This bucket will mainly include allocations to strategic partnerships and investments, and therefore may be relatively illiquid.

- The primary focus of this bucket will be to support the ecosystem.

We understand that building a diversified portfolio takes time, so instead these targets are provided as a framework for long-term allocations.

Rebalancing Guidelines

The TMC will periodically review the asset allocation of the portfolio to determine if any adjustments are necessary based on material changes to market conditions or Aave’s unique circumstances. Given the inherent volatility of crypto, the TMC will be active in rebalancing when necessary during periods of market stress to ensure constraints remain in effect (e.g. actively adjusting collateral to reduce risk of liquidation).