title: [ARFC] Deploy Ethereum Collector Contract

author: @llamaxyz - @TokenLogic

dated: 2023-03-08

Summary

The purpose of this proposal is to hold 6 months of runway in v2 USDC and begin deploying a portion of the funds held in the Ethereum Collector Contract to earn yield.

Abstract

This publication presents a proposal for how Aave could deploy its Ethereum Collector Contract holdings to earn yield.

A six-month aUSDC stable coin runway is held on Aave v2 Ethereum to facilitate payment to the existing service providers. To accommodate this, several asset holdings are to be swapped to USDC and deposited into Aave v2. The cost of service providers grossly exceeds v2 aUSDC revenue.

A diversified portfolio spanning five protocols is presented outside of the existing veBAL and CRV discussions, [1]. Outside of the proposed veBAL holding, the maximum exposure to any one protocol is 34.5% (excl. Aave), spanning three individual allocations. The expected yield is 5.0% with the primary yield source being protocol inflation schedules, along with complementary swap and borrowing fee derived yield.

Motivation

This proposal presents the rationale for how the Ethereum Collector Contract is to be deployed. Do note, a separate proposal has been made for the Polygon Collector Contract, [2].

Guidelines

Llama views the Aave treasuries holistically in aggregate, rather than as individual isolated funds on each respective network. Do note, a previous Snapshot vote indicates each Treasury/Collector Contract holding is to remain on the respective network and not be consolidated on any one network.

Mitigating risk is our primary concern in managing the treasury, and Llama views risk through several different lenses, including (but not limited to):

-

Market Risk.

Market risk is inherent in any investment that trades freely on secondary markets. While it can’t be mitigated entirely, maintaining a portion of the treasury in productive stable coins will prevent excess volatility in dollar terms. -

Idiosyncratic. (position-specific) risk.

While idiosyncratic risk cannot be avoided entirely, it can be mitigated through prudent portfolio construction and diversification of protocols/ecosystems. -

Liquidity Risk.

Liquidity can be a risk during periods of network congestion or in the event liquidity is needed but not available for operational expenses. Thorough liquidity and exit risk analysis will be performed when determining if a strategy is suitable for Aave. -

Centralization Risk.

Some protocols present centralization risk. To help mitigate this risk, we’ll avoid overexposure to single assets. For example, to limit centralization risk of overexposure to one stable coin, we will use a basket of the most liquid/dominant stable coins. -

Smart Contract Risk.

Crypto assets have varying levels of infrastructural risks related to the Ethereum network and smart contracts. Smart contract exploits (e.g., inflation of the stable coin via exploitation of a minting function), use of admin keys, oracle risk, and more, can all destroy the value of an asset. To minimise smart contract risk, we will operate through on-chain proposals and deploy the treasury only into well-known and reputable assets. -

Oracle Risk.

Widely trusted and proven oracle feeds are strongly preferred, and Chainlink oracles are to be used wherever possible. Oracle exploits are one of the most frequent exploits within DeFi. Llama wants to ensure that any investment that utilises (particularly derivatives) oracles are set up with secure price feeds/data.

All strategies will undergo an internal risk assessment whereby each of the above risks are investigated and taken into consideration. This is performed as part of the screening process when considering various strategies for eligibility. Any known risks are to be clearly articulated in any proposal to Aave.

Quantitative Risk

Llama will actively monitor the following, among other, risk considerations:

| Parameter | Target |

|---|---|

| % of the liquid portfolio exposed to one protocol. Excl. Aave | 30% +/- 10% |

| Leverage | <20% |

| Correlations | Similar to Revenue Streams |

| % of portfolio exposed to one network | Similar to Revenue Streams |

| % of portfolio hedged | Where applicable |

Note: while the numbers above represent good targets, our overall internal approach to risk will evolve along with the market.

Currently, most of Aave’s future growth initiatives are somewhat connected to Balancer. Over time, we expect other strategic initiatives to evolve and we’ll be able to reduce our protocol exposure targets accordingly.

Overview

This section summaries the current Ethereum Collector Contract holdings and existing commitments.

Current Holdings

The table below shows the vast majority of the assets held in the Ethereum Collector Contract minus some smaller holdings.

| Asset | Quantity | Unit Price | Value |

|---|---|---|---|

| ETH | 104.54 | $1,565.79 | $163,687.69 |

| awETH | 1,195.79 | $1,565.79 | $1,872,356.02 |

| wETH | 10.31 | $1,565.79 | $16,143.29 |

| aUSDC | 2,307,926.13 | $1.00 | $2,307,926.13 |

| USDC | 297,352.31 | $1.00 | $297,352.31 |

| aDAI | 4,323,665.40 | $1.00 | $4,323,665.40 |

| DAI | 12,129.12 | $1.00 | $12,129.12 |

| aUSDT | 4,182,478.14 | $1.00 | $4,182,478.14 |

| USDT | 32,001.15 | $1.00 | $32,001.15 |

| BAL | 300,000.00 | $6.61 | $1,983,000.00 |

| aBAL | 9,191.56 | $6.61 | $60,756.21 |

| aCRV | 642,423.77 | $0.91 | $584,605.63 |

| CRV | 19,714.11 | $0.91 | $17,939.84 |

| aSNX | 89,010.77 | $2.82 | $251,010.37 |

| awBTC | 5.14 | $22,379.00 | $115,028.06 |

| aLINK | 12,138.23 | $6.87 | $83,389.64 |

| LINK | 142.01 | $6.87 | $975.61 |

| aSUSD | 14,555.93 | $1.00 | $14,555.93 |

| aGUSD | 13,379.44 | $1.00 | $13,379.44 |

| MKR | 12.94 | $951.76 | $12,315.77 |

| aBUSD | 11,617.28 | $1.00 | $11,617.28 |

| aTUSD | 10,699.60 | $1.00 | $10,699.60 |

| aYFI | 0.49 | $10,762.38 | $5,273.57 |

| aUNI | 441.72 | $6.24 | $2,756.33 |

| wBTC | 0.09 | $22,379.00 | $1,946.97 |

| TUSD | 1,604.09 | $1.00 | $1,604.09 |

| ARC aUSDC | 56,843.44 | $1.00 | $56,843.44 |

| RWA aUSDC | 17,702.86 | $1.00 | $17,702.86 |

| aFRAX | 5,322.28 | $1.00 | $5,322.28 |

| aCVX | 4,569.16 | $5.89 | $26,912.35 |

| aLUSD | 2,939.65 | $1.00 | $2,939.65 |

| aUST | 892,768.26 | $0.02 | $21,643.56 |

| Total | $16,509,957.75 |

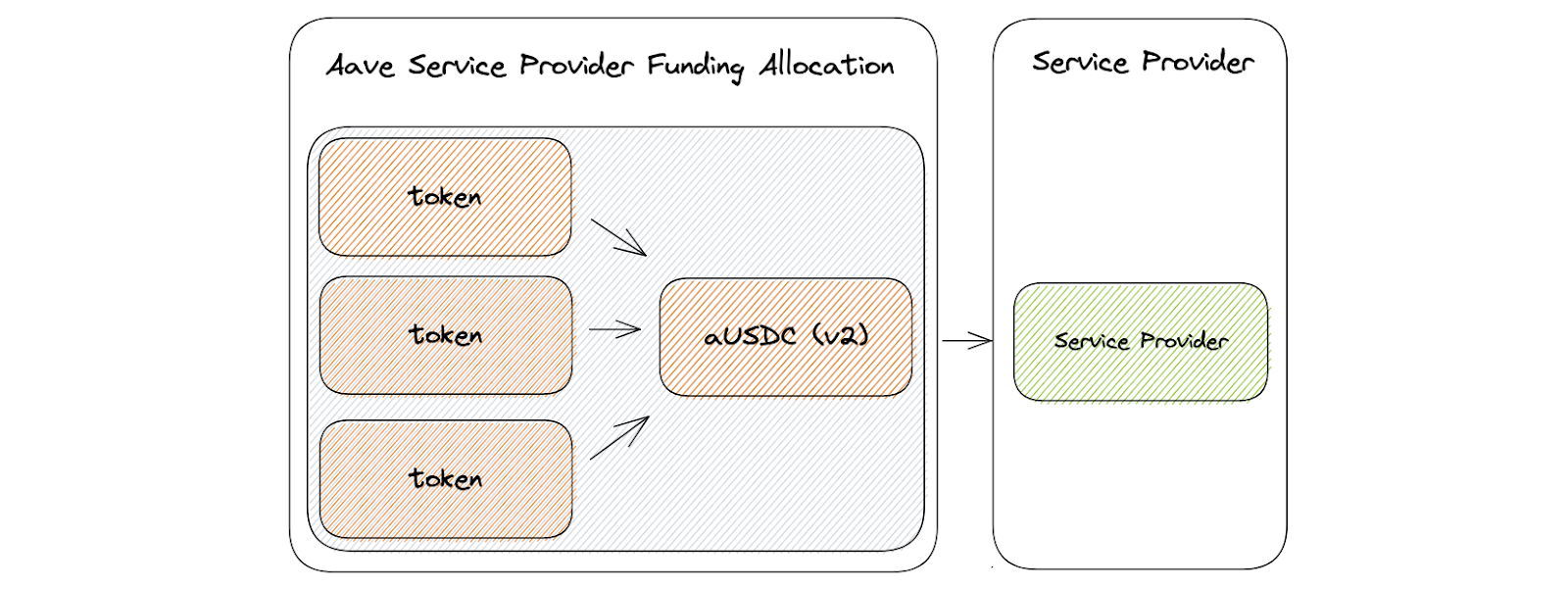

Service Provider Funding

Whilst deposits in Ethereum v2 are required for upholding Aave’s commitment to various service providers, minimal allowance has been made for the onboarding of additional service providers or retrospective funding requests as the values and timing are unknown. Llama will respond to each request as they emerge. Do note there are funds held passively on Aave v3 Ethereum.

For the purpose of this proposal, $4,290,000 is to remain in Aave v2. For context, over the last 6 months, the lowest aUSDC Aave v2 on Ethereum revenue was $49,160 and highest was $122,095.97. Aave v2 is not generating sufficient aUSDC-denominated revenue to support the service provider streaming contracts. Furthermore, Aave has insufficient v2 aUSDC holdings to fund the next 6 months with current v2 aUSDC holdings $2,307,926.13 versus $4,290,000 required.

| Asset | Quantity/Month | Unit Price | 6 Month Budget |

|---|---|---|---|

| USDC | 715,000 | $1 | $4,290,000 |

aUSDC streaming contract value of service providers:

- BGD $320,000/month, [3].

- Certora $157,500/month, [4].

- Llama $87,500/month, [5].

- Gauntlet $66,667/month, [6].

- Chaos Labs, $35,000/month, [7].

- Chaos Labs, $83,333/month, [8].

With respect to the second Chaos Labs streaming payment the following is extracted from the AIP text, dated November 2022:

- The payment streams will not start until 6 months after AIP approval with two incentive-based payments not included in this proposal but will be submitted after delivery. The DAO may terminate our engagement after 6 months prior to this stream initializing.

Due to the uncertainty around these payments, Llama has opted to include the larger $83,333/month figure when calculating a 6 months stable coin holding.

The 6 month budget will require USDC to be deposited into Aave v2 Ethereum as Aave’s expenses exceed its Ethereum v2 aUSDC nominated revenue.

To enable Aave to hold 6 months of v2 aUSDC expenses in the Collector Contract, the shortfall of $1,982,074 aUSDC is to be funded by converting the following holdings to v2 aUSDC.

| Asset | Quantity | Unit Price | Value |

|---|---|---|---|

| USDC | 297,352.31 | $1.00 | $297,352.31 |

| ARC aUSDC | 56,843.44 | $1.00 | $56,843.44 |

| aUSDT | 731,968.74 | $1.00 | $731,968.74 |

| aDAI | 731,968.74 | $1.00 | $731,968.74 |

| USDT | 32,001.15 | $1.00 | $32,001.15 |

| aUST | 892,768.26 | $0.02 | $21,643.56 |

| RWA aUSDC | 17,702.86 | $1.00 | $17,702.86 |

| aSUSD | 14,555.93 | $1.00 | $14,555.93 |

| aGUSD | 13,379.44 | $1.00 | $13,379.44 |

| MKR | 12.94 | $951.76 | $12,315.77 |

| DAI | 12,129.12 | $1.00 | $12,129.12 |

| aBUSD- subject to off boarding plan, [5] | 11,617.28 | $1.00 | $11,617.28 |

| aTUSD | 10,699.60 | $1.00 | $10,699.60 |

| aFRAX | 5,322.28 | $1.00 | $5,322.28 |

| aYFI | 0.49 | $10,762.38 | $5,273.57 |

| aLUSD | 2,939.65 | $1.00 | $2,939.65 |

| aUNI | 441.72 | $6.24 | $2,756.33 |

| TUSD | 1,604.09 | $1.00 | $1,604.09 |

| Total | $1,982,073.87 |

Do note, all the assets in the table above are to be converted to v2 aUSDC. Llama will also use this opportunity to swap several smaller <$1,000 holdings for USDC and deposit the funds into v2 aUSDC.

Where applicable, assets will be redeemed from Aave deployments and then swapped for USDC before being deposited into the v2 USDC reserve. The Collector Contract will approve and swap the various assets to USDC without the use of any intermediary swap contract being deployed. The aggregator most likely to be used is Cowswap or 1inch. This will be evaluated closer to the time of implementation.

Llama suggests all current and future service provider contracts migrate their respective streaming contracts to v3 Ethereum. When doing so, an amount of aUSDC should be redeemed from v2 and deposited into v3 for aethUSDC.

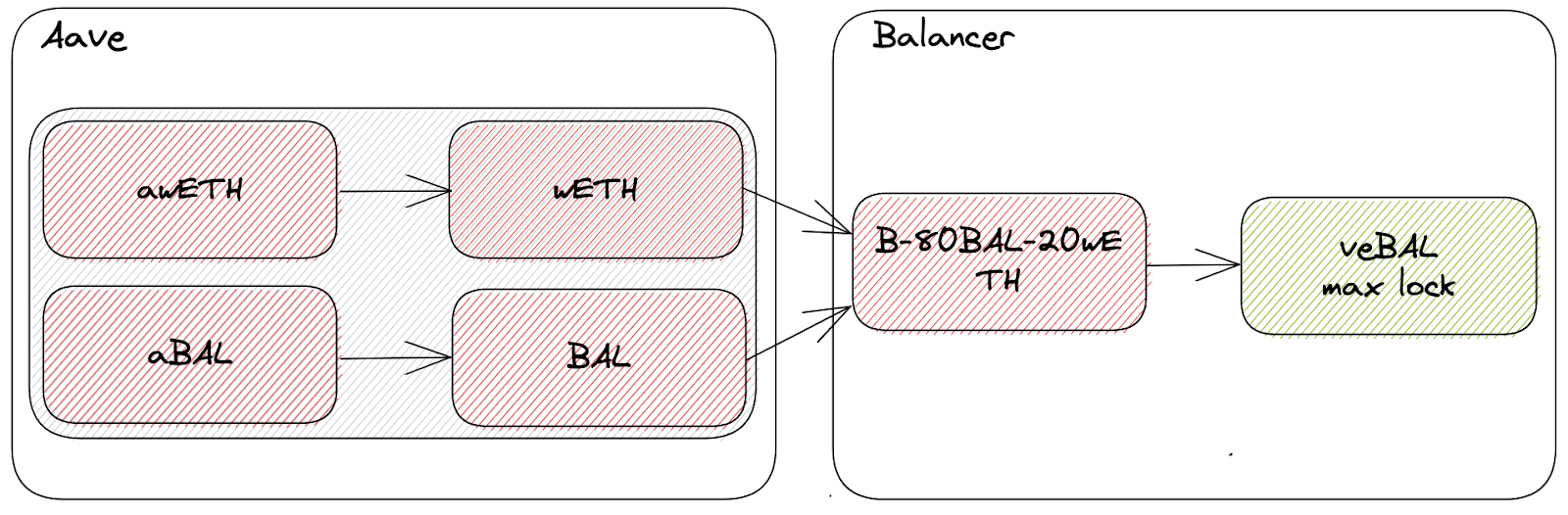

veBAL Funding

To acquire veBAL Aave must lock the B-80BAL-20WETH token which consists of both BAL and wETH, 80% BAL and 20% wETH. Aave holds $2,043,756.21 in BAL and aBAL on Ethereum at the time of writing. To complete the B-80BAL-20WETH acquisition, approximately $510,939.05 of wETH is required, or 24.90% of Aave’s combined wETH and ETH holdings at the time of writing.

| Asset | Quantity | Unit Price | Value |

|---|---|---|---|

| BAL + aBAL | 309,191.56 | $6.61 | $2,043,756.21 |

| awETH | 326.31 | $1565.79 | $510,939.05 |

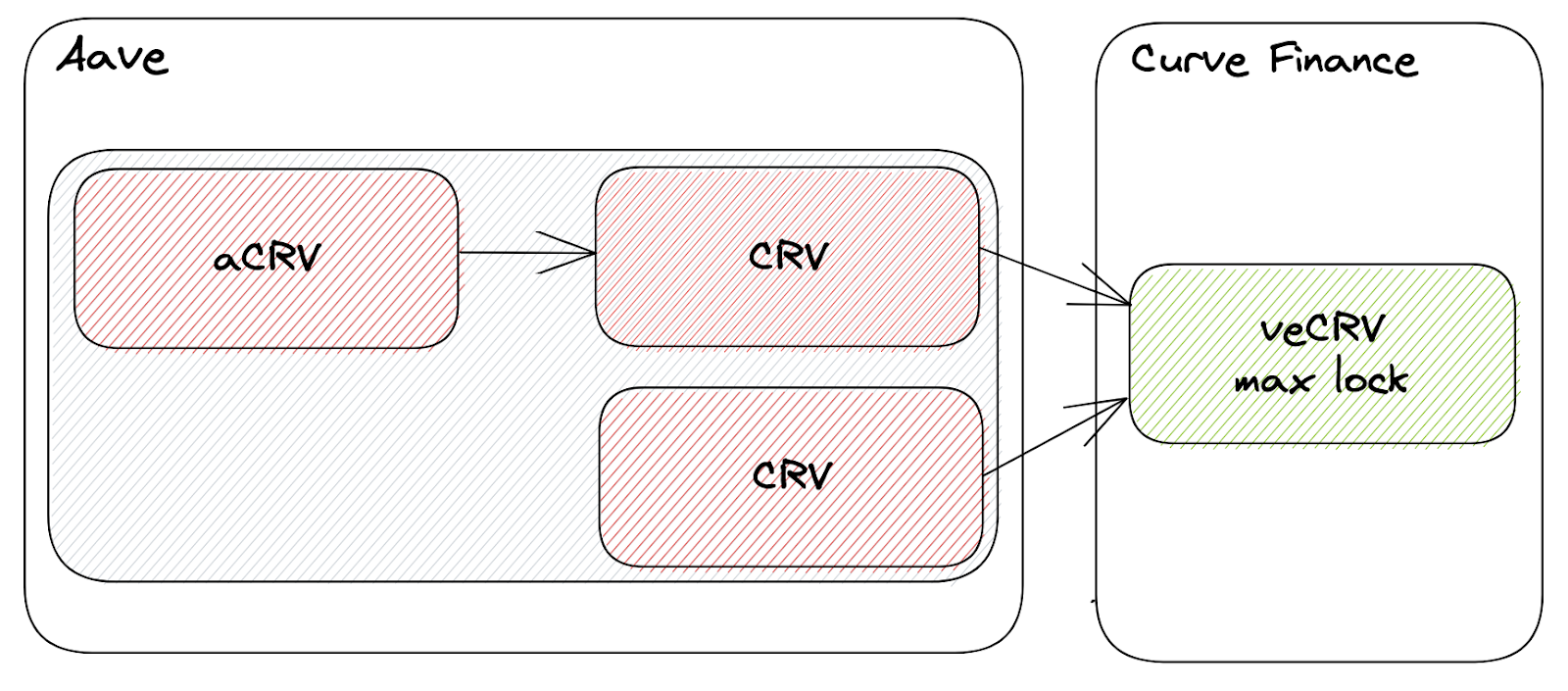

veCRV / st-yCRV / sdCRV Funding

Aave is currently discussing how to deploy the aCRV and CRV holding in the Collector Contract. Each strategy being considered includes all of the current aCRV and CRV holding in the Ethereum Collector Contract.

The strategy below reflects Llama’s preferred methodology for deploying Aave’s CRV and aCRV holding. All aCRV on Ethereum is to be redeemed, combined with the CRV holding, deposited into the Curve Finance voter escrow contract, and time locked for 4 years. Further information can be found here.

Available Asset Holdings

The below summaries the commitments outlined above:

| Summary | Value |

|---|---|

| Total Funds | $16,509,957.75 |

| Service Providers (6 months) | $4,290,000.00 |

| veBAL (incl. BAL and wETH) | $2,554,695.26 |

| veCRV/sdCRV/st-yCRV | $602,545.47 |

After putting aside 6 months of funding in v2 aUSDC, BAL and wETH for veBAL and the aCRV plus CRV holding for veCRV (or sdCRV or st-yCRV), the following assets remain available.

| Asset | Value |

|---|---|

| ETH | $1,541,247.95 |

| DAI | $3,591,696.66 |

| USDT | $3,450,509.40 |

| LINK | $84,365.25 |

| CVX | $26,912.35 |

| SNX | $251,010.37 |

| wBTC | $116,975.03 |

| Total | $9,062,717.01 |

Llama has excluded CVX from inclusion in the portfolio allocation below pending an outcome of the communities discussion around how the CRV position is to be deployed.

In the following Portfolio section, this publication presents a proposal for how these funds are to be deployed. Total value of the funds to be invested in the portfolio below is $9,035,804.66.

Portfolio

Summary

The below summarises the performance of the portfolio:

| Summary | Value |

|---|---|

| Total Funds | $16,509,957.75 |

| Portfolio Funds | $9,035,804.66 |

| Portfolio / Total Funds | 54.73% |

| Portfolio Revenue | $451,921.84 |

| Portfolio APR | 5.00% |

Overview

This proposal will present a medium risk portfolio to Aave for consideration. The portfolio offers a higher return relative to depositing each asset into the Ethereum v3 deployment and consists of nine strategies generating an expected return of 5.00%.

| Holding | Asset | Value | Allocation | Yield | Income ($) | Risk Exposure |

|---|---|---|---|---|---|---|

| 1 | Aave v3 - aethUSDC | $2,237,859.85 | 25.000% | 2.25% | $50,351.85 | 50.00% |

| 2 | Aave v3 - aethUSDT | $2,036,452.47 | 22.750% | 3.02% | $61,500.86 | incl. above |

| 3 | Aave v3 - aethwBTC | $116,975.03 | 1.307% | 0.05% | $58.49 | incl. above |

| 4 | Aave v3 - aethwLINK | $84,365.25 | 0.942% | 0.00% | $0.00 | incl. above |

| 5 | Lido DAO - wstETH | $693,770.11 | 7.750% | 4.50% | $31,219.65 | 7.75% |

| 6 | Rocket Pool - rETH | $693,770.11 | 7.750% | 4.32% | $29,970.87 | 7.75% |

| 7 | Balancer - BB-A-USD | $1,342,715.91 | 15.000% | 4.00% | $53,708.64 | 34.50% |

| 8 | Aura - BB-A-USD | $1,342,715.91 | 15.000% | 4.73% | $63,510.46 | incl. above |

| 9 | Aura - SNX / ETH | $402,814.77 | 4.500% | 39.05% | $157,299.17 | incl. above |

| Total | $8,951,439.41 | 100.000% | 5.00% | $447,619.99 | 100.00% |

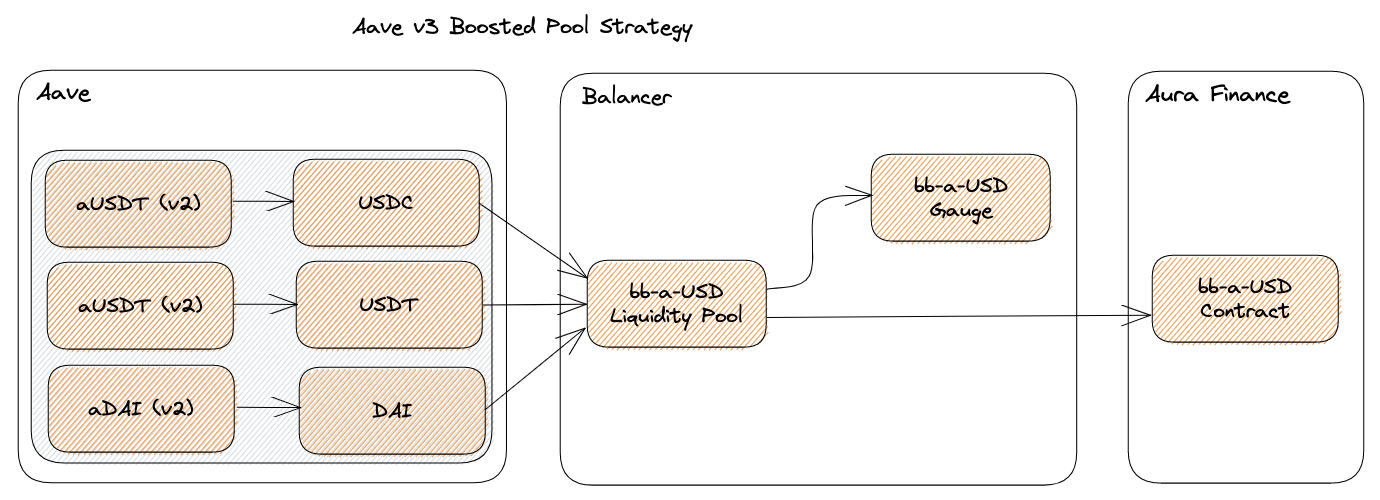

Aave v3 Boosted Pool, Balancer Gauge and Aura Finance Contract

The veBAL position will not have enough boost to maximise the return across all of Aave’s proposed Balancer liquidity positions. The veBAL Boost will be used to maximise Aave’s positions on Balancer. Once deposits in Aura Finance contracts generate more BAL emissions, Aave will deposit the BPT into the Aura Finance contracts.

Llama has already proposed depositing around $4.1m of liquidity into Balancer on Polygon. Aura is not yet deployed on Polygon. The publication proposes allocating a portion of the bb-a-USD BPTs into Balancer Gauges and Aura Finance contracts to maximise BAL emissions.

The bb-a-USD pool utilising Aave v3 is not yet created and therefore it is particularly difficult to estimate the yield and allocation between Balance and Aura Finance contracts. The new v3 bb-a-USD pool will be created by Balancer using the Bored Ghost Developing StataToken. It is expected to go live before the end of March 2023.

Provide Liquidity Balancer, Stake Balancer Gauge

The below strategies utilise Balancer liquidity pool contracts and deposit the BPT receipt token into Aura Finance’s contract. Aave’s veBAL holding, boost will be applied to maximise the yield on other Balancer liquidity positions. Aura Finance currently provides 1.45x boost on the SNX/wETH pool.

Aura Finances SNX/wETH contract offers 8.7% in BAL emissions and a total yield of 39.05%. An allocation of 4.50% ($402.81k) of the $8.96M portfolio generates around 35% ($157.30k) of the portfolio’s overall return.

Balancer Strategy Insight

Earn BAL and AURA

This strategy involves depositing Aave’s assets into Balancer Liquidity Pools and then staking BPTs with either Aura Finance or Balancer to maximise the BAL nominated yield. The BAL rewards are to be swapped for B-80BAL-20WETH and locked to grow Aave’s veBAL holding over time. Due to the continuous BAL inflation schedule, Aave’s influence within the Balancer ecosystem will fade over time. This proposal seeks to earn BAL rewards by providing liquidity on Balancer as a preferred strategy relative to continually purchasing BAL to avoid the veBAL holding being diluted over time.

The strategy encompasses three distinct pillars:

- Aave Collector Contract, where the assets are currently held

- Balancer Liquidity Pools, where Aave’s assets are deposited

- Staking the BPT with Balancer or Aura Finance

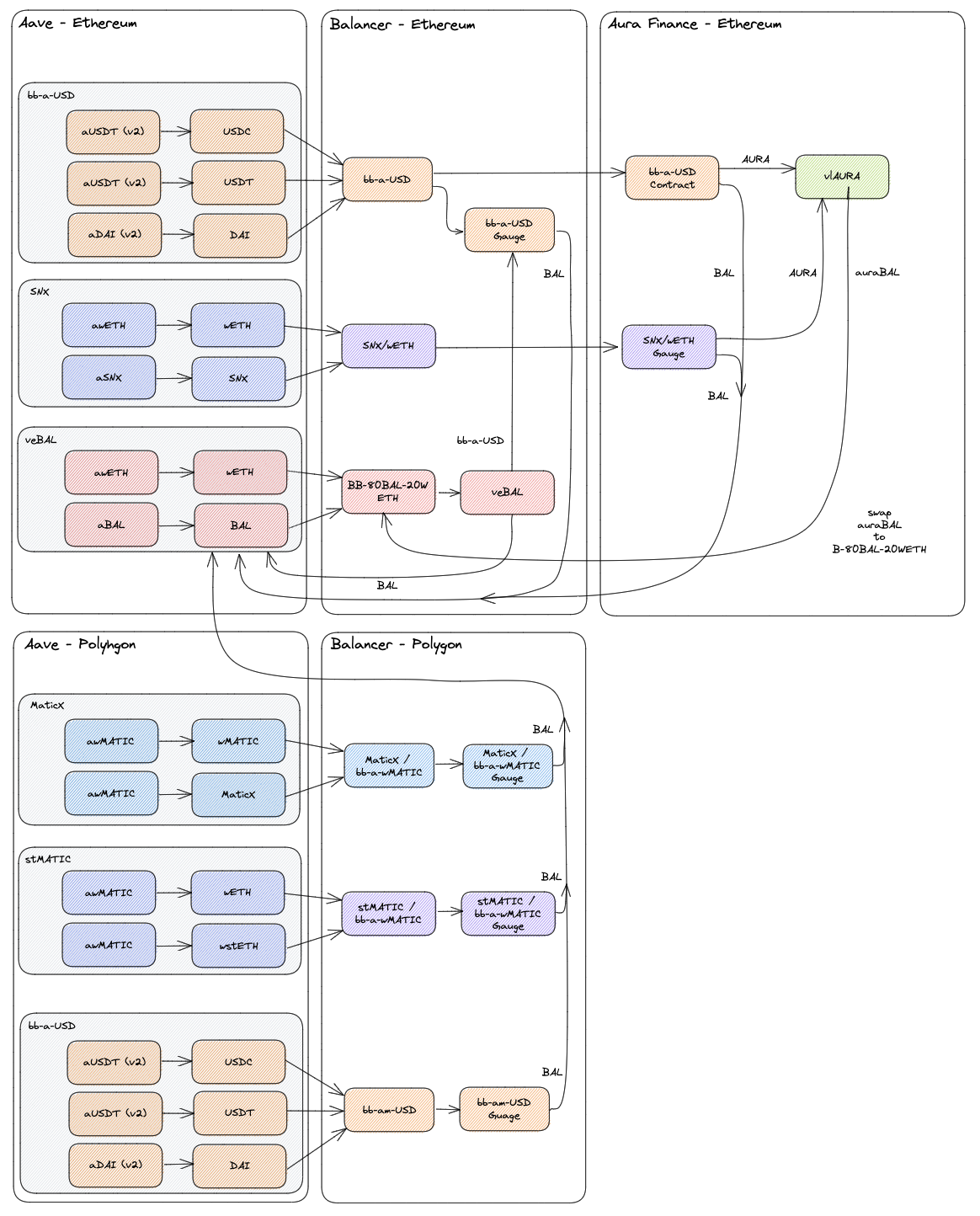

The flow of rewards are shown in the image below. Several functions will need to be added to the Collector Contract enabling the rewards to be claimed and the flows to occur as shown below. Llama will likely automate calling these functions on the Collector Contract similar to how existing revenue contracts are called.

The infographic above shows Aave deploying funds across two networks to earn yield. This proposal only includes the Ethereum funded aspect and shows the Polygon component for holistic context. The illustration shows some Ethereum BPTs deposited into Aura contracts and Balancer gauges. How much of each BPT is deposited is subject to market dynamics and may change prior to implementation. The strategy prioritises BAL emissions, which are influenced by the following:

- Amount of funds deposited into Aura Finance contracts

- Amount of funds deposited into Balancer gauges

- Size of each liquidity pool

- Aave’s veBAL holding size

- Amount of liquidity provided by Aave

- Boost applied by Aura Finance on each gauge

- Plus other more elaborate considerations, such as if Aave rents boost

Aura Finance is not yet deployed on Polygon, but does intend to launch after Balancer upgrades its gauge contracts in late Q1 / early Q2. Aave has the ability to pivot the Polygon strategy to include Aura Finance and Tetu contracts to earn additional yield. At the time of writing it is not possible to use Boost from the veBAL position on Polygon. This means if Aave optimises for yield, using Tetu and Aura Finance will likely lead to larger yields. This is something to consider in the future and may lead to a reallocation of the funds held on Polygon.

The returns from compounding are not included in the portfolio’s yield figure of 5.00%. This is due to the uncertainty of the timing and the variability of the yield which is unknown as the pools are not yet in production. The BAL generated from the following sources is routed to mainnet, and swapped for B-80BAL-20WETH. An equivalent 25% of awETH is redeemed, swapped to BAL and then B-80BAL-20WETH. This maintains a continuous BAL and wETH conversion to B-80BAL-20WETH which will then be deposited into the veBAL contract. The goal is to grow the veBAL holding and to better position Aave to boost GHO and Staked AToken adoption:

- aBAL revenue from Ethereum

- aBAL revenue from Polygon

- BAL from bb-a-USD

- BAL from SNX/wETH

- BAL from MaticX / bb-a-wMATIC

- BAL from stMATIC / bb-a-wMATIC

Next Steps

A Snapshot will be presented with NAE and ABSTAIN options. The NAE option signals for an alternative portfolio to be presented.

References

[1] [ARFC]: Deploy aCRV & CRV to veCRV

[2] [Discussion] Migrate, Consolidate and Deploy Polygon Treasury

[3] https://app.aave.com/governance/proposal/71/

[4] https://app.aave.com/governance/proposal/114/

[5] https://app.aave.com/governance/proposal/104/

[6] https://app.aave.com/governance/proposal/133/

[ARC] BUSD Offboarding Plan

[7] https://app.aave.com/governance/proposal/139/

[8] https://app.aave.com/governance/proposal/113/

[9] Deed - CC0 1.0 Universal - Creative Commons

Copyright

Copyright and related rights waived via CC0, [9].