Summary

We support @ChaosLabs proposed deprecation of low-demand volatile assets on Aave V3 instances. The rationale is compelling: in times of market stress, these assets exhibit large price swings, oracle desynchronization, and arbitrage opportunities, all of which pose outsized risks to the protocol’s solvency.

By marking these assets non-borrowable and reducing their LTV to zero, the protocol renounces modest revenue streams while significantly bolstering its resilience against exploit vectors and bad debt accumulation. In our view, this is a prudent trade-off: reducing tail risk should take precedence over marginal protocol revenue.

Long-tail assets volatility

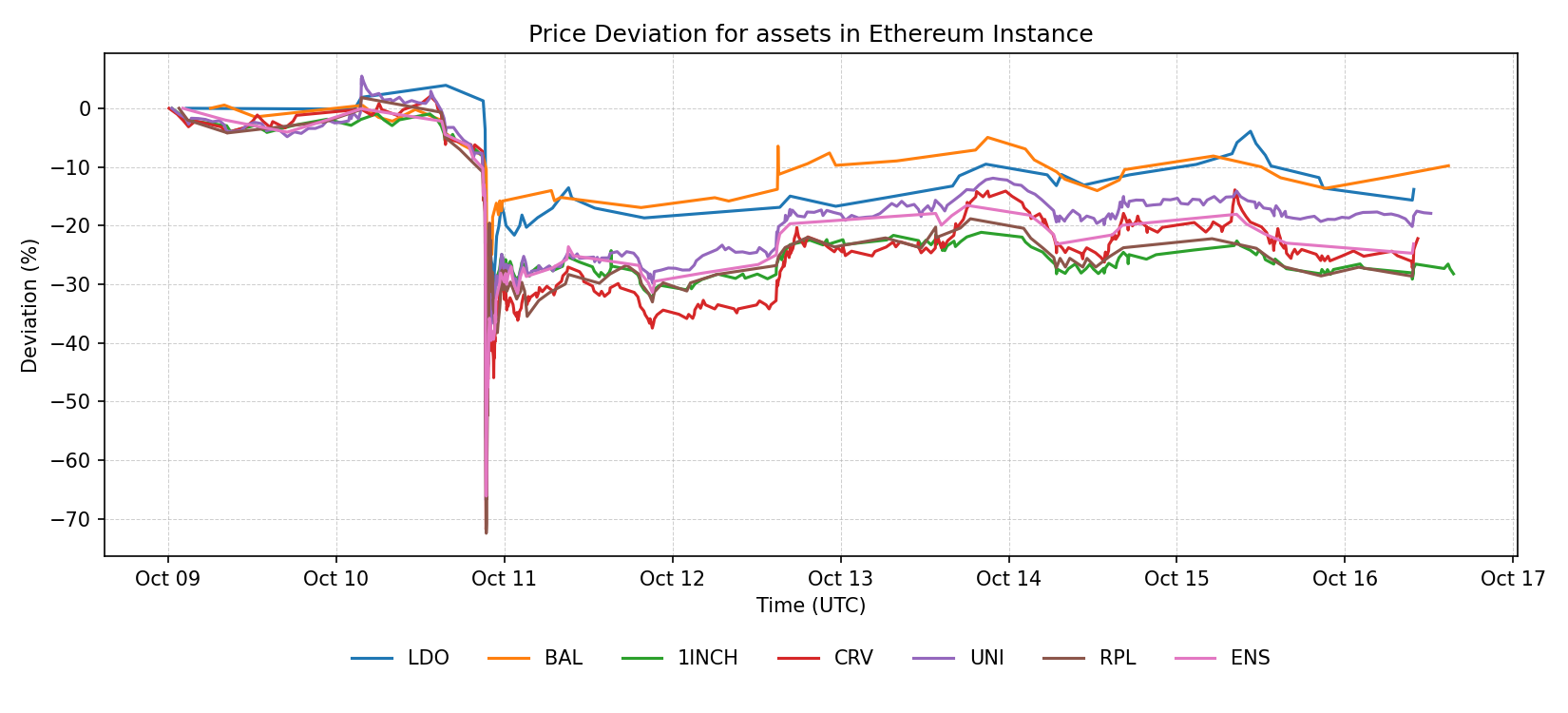

During the recent tariff-headline shock, Aave V3 Ethereum Core market experienced pronounced volatility and price dislocation across long-tail assets. Our analysis, conducted using Chainlink price feeds, shows that RPL suffered the largest drawdown, exceeding 70%, while CRV was the least affected at roughly 45%.

Source: LlamaRisk, October 20, 2025

Collateral asset demand

As of October 20, most of these asset reserves operate at very low utilization levels, typically below 30%, which means they generate minimal revenue for the protocol. Maintaining these assets as non-borrowable with an LTV of zero helps minimize the protocol’s insolvency risk and limits exposure to volatile, low-performing assets.

| Instance | Asset | Borrow Cap | Current Utilization | Uopt |

|---|---|---|---|---|

| Ethereum | RPL | 500,000 | 64.37% | 80% |

| Ethereum | CRV | 7,000,000 | 15.02% | 45% |

| Ethereum | BAL | 1,000,000 | 4.02% | 45% |

| Ethereum | UNI | 330,000 | 24% | 45% |

| Ethereum | LDO | 500,000 | 13.45% | 45% |

| Ethereum | ENS | 20,000 | 32.98% | 45% |

| Ethereum | 1INCH | 475,200 | 7.37% | 45% |

We agree with @ChaosLabs initial asset list proposed for deprecation and are ready to coordinate for a smooth and timely deprecation process across all affected markets.

Disclaimer

This review was independently prepared by LlamaRisk, a DeFi risk service provider funded in part by the Aave DAO. LlamaRisk is not directly affiliated with the protocol(s) reviewed in this assessment and did not receive any compensation from the protocol(s) or their affiliated entities for this work.

The information provided should not be construed as legal, financial, tax, or professional advice.