Overview

In response to the ARFC proposing the listing of srUSDe PT tokens on the Ethereum Core instance of Aave v3, we have conducted a comprehensive analysis of the underlying Strata protocol. Specifically, the analysis focuses on the underlying economic design of the protocol, covering the system design, internal pricing dynamics of senior and junior tranches, along with yield distribution logic and historical performance of the assets. As the ARFC targets a future srUSDe principal token that has not yet been deployed on Pendle, this post focuses on Strata’s structural design and utilizes the most recent January-maturity PT-srUSDe as an illustrative case study for the expected pricing, liquidity, and implied APY dynamics of the next srUSDe PT. Once the next srUSDe PT is listed on Pendle and sufficient market data is available, we will follow up with specific risk parameter recommendations calibrated to that maturity under the Principal Token Risk Oracle framework.

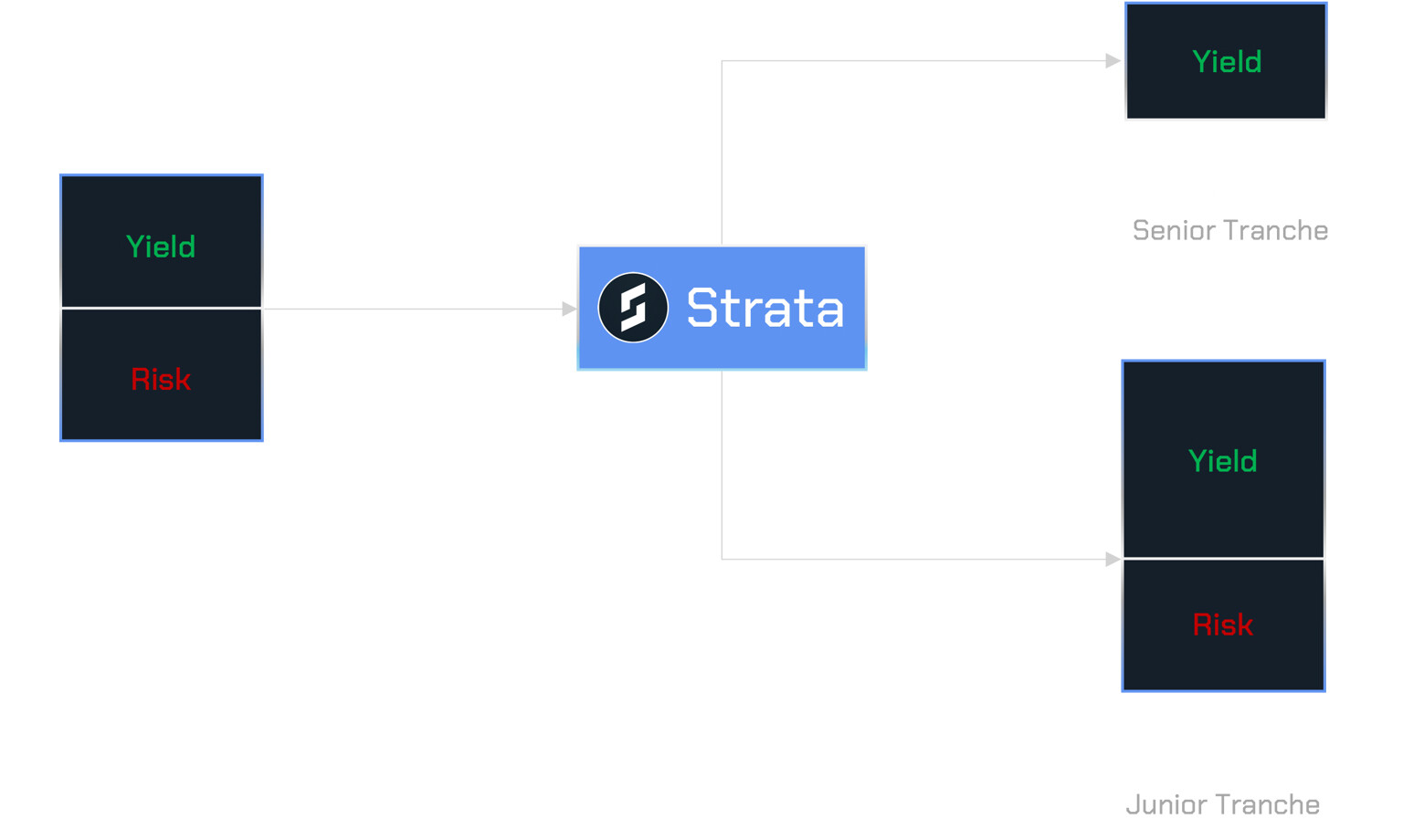

Strata Overview

Strata is a structured yield protocol built on top of Ethena’s staked USDe. The protocol introduces a two-tranche system that segregates yield and risk exposure into distinct instruments — srUSDe (the senior tranche) and jrUSDe (the junior tranche). Through this mechanism, Strata seeks to create differentiated risk and return profiles, offering a tailored approach to the risk and reward bundling.

At the core of Strata’s design is its Dynamic Yield Split mechanism, which governs the allocation of realized yield from the underlying sUSDe between senior and junior tranche holders. The mechanism references a benchmark rate, defined as the supply-weighted average yield across major USDT and USDC stablecoin lending markets on Aave; a TVL ratio, which represents relative shares of notional locked in senior and junior tranches; and a set of exogenously set risk premium parameters, which govern the allocation of yield between the instruments.

Yield Distribution

Risk Premium

srUSDe Yield

Hence, if the junior TVL ratio is at the 105% threshold and sUSDe yield is 0%, while the stablecoin supply yield on Aave is 10%, the runway for srUSDe would be 6.5 months. While such a scenario is unlikely, the current baseline of 5% supply rate would allow for 1 year of runway. As jrUSDe is bound to depreciate under such extreme scenarios, the yield of the senior tranche will be represented by the yield of the underlying staked USDe if the TVL of the junior tranche is to reach zero.

jrUSDe Yield

The chart above illustrates the regime shift inherent in Strata’s perpetual tranche instruments. Between October 15 and October 25, jrUSDe experienced pronounced depreciation as the sUSDe yield fell materially below the Aave stablecoin supply rate. The resulting yield shortfall was absorbed by the junior tranche, leading to a decline in its exchange rate. Following October 25, this dynamic reversed: jrUSDe began appreciating at a substantially higher rate, reflecting the leveraged upside that junior holders earn when underlying yields exceed the benchmark. This pattern is consistent with the economic design of the protocol, in which junior capital absorbs downside during unfavorable yield regimes and captures amplified returns during favorable ones.

Rate Sourcing

Such contract logic ensures that the benchmark reflects the liquidity distribution while remaining anchored to the yields of the USDT and USDC lending markets. To prevent abrupt or manipulated rate spikes, the contract applies strict bounds to the computed value; if the benchmark APR falls outside this range, the call reverts, and the prior valid rate is retained.

The sUSDe base rate is derived from Ethena’s vesting process. Unvested rewards accumulate and vest linearly over an eight-hour window, and the contract annualizes the remaining unvested amount relative to vesting time and total assets to produce an APR. If vesting has been fully completed, the base rate returns zero. This approach ensures the reported sUSDe APR reflects the immediate realized yield rather than a smoothed estimate.

While the historical performance of the asset is limited, we have replicated the rate computation logic from the AaveAprPairProvider contract in order to observe the APY dynamics on a longer horizon. As expected, the yield profiles of the senior and junior tranches outline similar dynamics to the recent period, where jrUSDe represents a leveraged bet on the positive spread between sUSDe yield and the Aave supply rate, while srUSDe, in large part, tracks the Aave supply rate with a meaningful premium obtained from the sUSDe yield. Within the simulation, the quantities of the minted reserves were assumed to be constant at a junior TVL share of 10%, which, as expected, resulted in mean junior tranche APYs of approximately 22% over the course of the year and, during several periods of extreme yield, in excess of 50% on an annualized basis. This indicates that, under the current fixed parameterization, the junior tranche is structurally over-incentivized.

Additionally, inspection of the Accounting contract shows that jrUSDe and srUSDe exchange rates are updated on an event basis: internal accounting is refreshed via updateAccounting, which is called on each mint or redeem operation. Such a configuration ensures minimal abuse of the yield distribution; additionally, the points distribution system also exhibits substantial robustness, with appropriate measures in place to minimize points sandwiching activity.

Mints & Redemptions

Strata supports minting and redeeming srUSDe against both USDe and sUSDe via the Strata UI and smart contracts, with srUSDe redemptions into USDe subject to Ethena’s 7-day unstaking period, while sUSDe redemptions are processed instantly. The protocol is designed with configurable redemption fees on senior and junior tranche assets, intended to dampen short-term arbitrage and speculative flow and to help stabilize tranche liquidity over time. In practice, these fees are currently set to 0 bps, and there appears to be no effective fee on direct srUSDe to sUSDe conversions. As a result, there is limited friction for yield arbitrage between srUSDe and sUSDe, which may facilitate fast repricing of the senior tranche yield but also reduces the protocol’s ability to discourage purely opportunistic, yield-seeking rebalancing. However, the team has indicated that redemption fees will be increased in the near term, which should reduce or eliminate the incentive to arbitrage the rates.

srUSDe Performance

Considering srUSDe as a standalone asset, its utility on Aave is fairly limited as the senior tranche entails a conservative and, to an extent, hedged exposure to sUSDe. For the yield-bearing class of stablecoins, the primary utility is traditionally centered around leveraged yield strategies, where users supply the yield-bearing asset as collateral, while borrowing non-yield-bearing stablecoins and recursively minting the yield-bearing asset, thereby increasing the notional exposure to the yield-bearing asset. By leveraging the spread between the yield of the collateral asset and borrowing costs, users can achieve substantial leveraged net yields. In the case of srUSDe, which, yield-wise, has two modes of operation: supply APY of the average of USDT and USDC, discounted sUSDe yield; both of which need to be considered to assess the utility of the token within the protocol.

In cases where the benchmark rate is lower than the underlying yield of sUSDe, the strategy is not profitable, as the benchmark rate represents the supply yield of stablecoins, which is a reserve-factor-discounted borrow rate of the same assets; hence, the spread on such a strategy would be strictly negative and leveraged strategies would be guaranteed to have a negative PnL.

On the other hand, during periods of elevated sUSDe yield, the senior tranche yield would be discounted by the risk premium; hence, utility-wise, in the short term the asset’s yield would not be competitive with sUSDe, due to the inferred discount.

Additionally, in scenarios where the junior tranche TVL approaches zero, srUSDe may be unable to deliver the Benchmark rate. In the absence of sufficient jrUSDe to absorb losses or fund the senior yield, srUSDe would effectively function as a deposit vault for sUSDe.

Therefore, the asset on its own presents minimal short-term utility on Aave, as both regimes are either unprofitable or dominated by alternatives. In the first case, srUSDe’s yield will be lower than stablecoin borrow costs. In the second operational mode, the yield will be at a competitive disadvantage compared to sUSDe. From a protocol-design perspective, these dynamics will be inherited by any srUSDe-based PT listed on Pendle: the PT’s implied yield will primarily reflect srUSDe’s yield accrual mechanics and incentives rather than offering fundamentally new risk–return characteristics at the underlying level.

While srUSDe represents a conservative instrument, which aims to expose investors to the staked USDe yield while providing protection in case of subpar performance by subsidizing the yield up to the weighted supply rate of USDT and USDC on Aave v3, the junior instrument presents an entirely different risk and return profile, as it effectively facilitates investor exposure to the leveraged spread between sUSDe yield and Aave weighted stablecoin supply.

Audits

Strata’s core tranche contracts have undergone a multi-phased audit process by three independent security firms. The initial round of audits was conducted in parallel by Cyfrin and Guardian, followed by a second phase performed by Quantstamp, covering the tranche accounting logic, yield-split mechanics, withdrawal flows, and supporting contracts. A list of public reports is available here.

Across these reviews, auditors identified issues ranging from configuration and accounting inconsistencies to withdrawal behavior and strategy-level attack vectors. Public tracking of the findings shows the vulnerabilities have been addressed in commits and marked as fixed and verified by the auditor. Additionally, BGD will conduct an independent, in-depth technical review of the Strata integration and its interaction with Aave, providing its conclusions in a separate technical assessment.

Case Study: PT-srUSDe-14JAN2026

As the ARFC does not specify a concrete principal token for the upcoming listing, the most recent January-maturity srUSDe principal token, PT-srUSDe-14JAN2026, is used here purely to exemplify the expected dynamics of a future srUSDe PT. Please note that a separate, token-specific assessment and parameter recommendation will be presented once the next srUSDe PT is available on Pendle and has accumulated sufficient market history.

Performance

The implied APY of Pendle’s PT-srUSDe-14JAN2026 materially exceeds the realized yield of srUSDe, largely due to ongoing incentive programs. The current premium is approximately 4 percentage points: PT-sUSDe trades near a 6% implied rate, whereas PT-srUSDe is priced around 10%. At this level, the January maturity can attract considerable stablecoin borrowing demand. A user looping PT-srUSDe could capture a spread of over 6%, and with roughly 10x leverage, the net return may approach 60% under favorable market conditions. Such elevated implied yields, therefore, create strong incentives for leveraged borrowing activity if a comparable asset is to be listed on Aave v3.

Initial Discount Rate Per Year and Maximum Discount Rate Per Year

Based on the limited historical observed data and the pricing configuration of the PT-srUSDe-14JAN2026 market, our initial recommendations for the discountRatePerYear and maxDiscountRatePerYear would be as follows:

- Initial discountRatePerYear: 9.46%

- maxDiscountRatePerYear: 31.82%

For the forthcoming srUSDe PT, these values will be reassessed based on the observed term structure, liquidity, and volatility at that specific maturity, and may differ from the example above.

Liquidity Dynamics

With PT-srUSDe-14JAN2026, liquidity depends on both the underlying USDe markets and Pendle’s PT/SY AMM pool, and current depth is sufficiently strong. The plot below represents the liquidity available under 3% slippage as the market approaches maturity. As the market matures and moves closer to expiry, the slippage associated with selling PT becomes less extreme. This trend is especially pronounced for assets with higher expected implied yield fluctuation, as they tend to have more variance in liquidity concentration. The market currently facilitates swaps of up to $30M with slippage limited to 3% or less.

The SY liquidity in PT-srUSDe-14JAN2026’s AMM has stabilized at $30M, indicating a substantial liquidity depth, and has remained at that level since.

While these liquidity dynamics are specific to the January 14th-maturity principal token, they provide a reasonable baseline for the order of magnitude and slippage profile that can be expected for a subsequent srUSDe PT, subject to re-evaluation at the time of listing.

Recommendation

Chaos Labs supports, in principle, the listing of a future srUSDe-based PT on the Aave v3 Ethereum Core instance under the Principal Token Risk Oracle framework with the dynamic linear discount-rate oracle, conditional on the specific maturity, liquidity profile, and market conditions at the time of listing. While listing the senior tranche instrument itself is not expected to expand stablecoin borrowing demand significantly, a sufficiently incentivized srUSDe PT can present substantial potential: Pendle market data for PT-srUSDe-14JAN2026 shows a materially higher implied APY than srUSDe. Since standalone short-term srUSDe looping is either inefficient or unprofitable, incremental demand for any future srUSDe PT is likewise expected to come primarily from the incentivized PT market.

Additionally, to ease the unwinding frictions, we aim to recommend including sUSDe in the E-Modes as an alternative collateral, thereby increasing debt stickiness within the associated market. Separately, listing an srUSDe PT will expose Aave to additional smart contract risk, as much of Strata’s on-chain infrastructure is unique and novel. A comprehensive technical assessment by BGD is therefore crucial, and proceeding with any srUSDe PT listing should be conditional on a positive technical review.

Disclaimer

Chaos Labs has not been compensated by any third party for publishing this recommendation.

Copyright

Copyright and related rights waived via CC0