title: [ARFC] Polygon v2 - Parameter Update

Author: @TokenLogic - @MatthewGraham & @defijesus

Dated: 2023-04-19

Simple Summary

This publication presents an opportunity to help kick start the migration from Polygon v2 to v3 by capitalizing on the favorable conditions presented by the multi-token liquidity mining program on v3.

Abstract

On Polygon, there are two Aave deployments in production and the majority of the liquidity is deposited into the obsolete v2 deployment. With Chainlink expected to monetise oracles, v2 partially frozen and three communities actively distributing rewards on v3, this publication seeks to further encourage the migration of users from v2 to v3.

With a successful TEMP CHECK Snapshot vote, this publication has incorporated community feedback and presents three options for the community to select from. The key consideration is the upside realized by acting early during the liquidity mining campaign.

This publication parameter changes supportive of encouraging the migration of funds without putting any users’ positions at risk of liquidation.

Motivation

Currently, there are three communities distributing four tokens across Polygon v3.

- SD - Stader Labs

- LDO - Lido DAO

- MaticX & stMATIC - Polygon Foundation

This has led to Polygon v3 offering better deposit rates relative to v2. The charts below show the TVL for Polygon v3 since genesis, v3 for 2023 and v2 for 2023. During 2023 TVL in v3 is steadily increasing, the v2 markets TVL is more trending sideways with asset prices broadly trending sideways/higher.

Liquidity Mining (LM) on v3 is helping to pull users across and the migration tool from BGD further supports this initiative. At TokenLogic, we believe more can be done to migrate users and it is better to do this whilst LM is ongoing. This publication at its core seeks to accelerate the migration of users from v2 to v3 whilst LM is ongoing.

The TEMP CHECK received strong support from the community with 525k votes, 92.42%, in favor of implementing the change. This publication incorporated feedback from the comments on the previous governance forum post and now includes two additional reduced impact options for the community to consider.

Incorporating feedback from the community, TokenLogic is presenting three options to the community for consideration. Options 1) and 2) include adjusting the Uoptimal and Reserve Factor (RF) parameters where as Option 3 includes only adjusting the RF parameter:

- Option 1 - Adjust Uoptimal & RF Aggressive

- Reduce Uoptimal by 50.00% the difference between current utilization and Uoptimal value

- Increase RF such that deposit yield remains the same

- Maintain the same Slope2 gradient

- Option 2 - Adjust Uoptimal & RF Conservative

- Reduce Uoptimal by 33.33% the difference between current utilization and Uoptimal value

- Increase RF such that deposit yield remains the same

- Maintain the same Slope2 gradient

- Option 3 - Increase RF

- Increase RF such that deposit yield is reduced by 20%

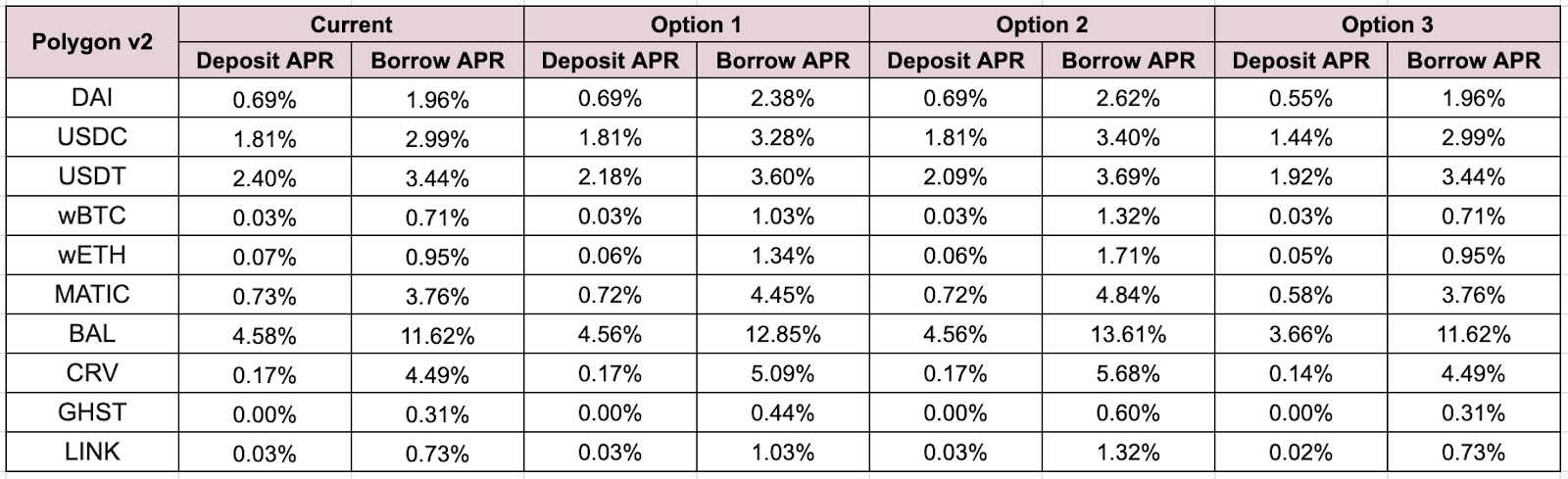

The below table compares the outcome of Option 1, 2 and 3.

Implementing any of the three options above will further encourage users to migrate from v2 to v3. Option 3 affects only deposit rates and thus increases the deposit rate differential between the markets as the borrowing rate remains unchanged on v2. Option 3 relies on depositors migrating liquidity, due to lower deposit rate, to increase the borrowing cost over time. Whereas Option 1 and 2 directly increase the borrowing cost for users whilst keeping deposit rates the same which encourages borrowers to migrate.

Option 1 and 2 - leverage strategies and simply deposit to draw a loan users will experience higher borrowing rates. Structured leverage products will experience increased vol decay (deposit yield - borrowing yield - rebalancing/recentreing costs). Do note, the feasibility of structured 2x leverage products is more sensitive to LTV & LT changes, as reducing these parameters can break the strategy. Reducing the Uoptimal and increasing the RF means structured products remain viable, however, like all debt positions, there are higher holding costs over time. Option 3 impacts these products less as the collateral type is not normally stable coins and more likely to be high vol assets which typically have very low deposit rates.

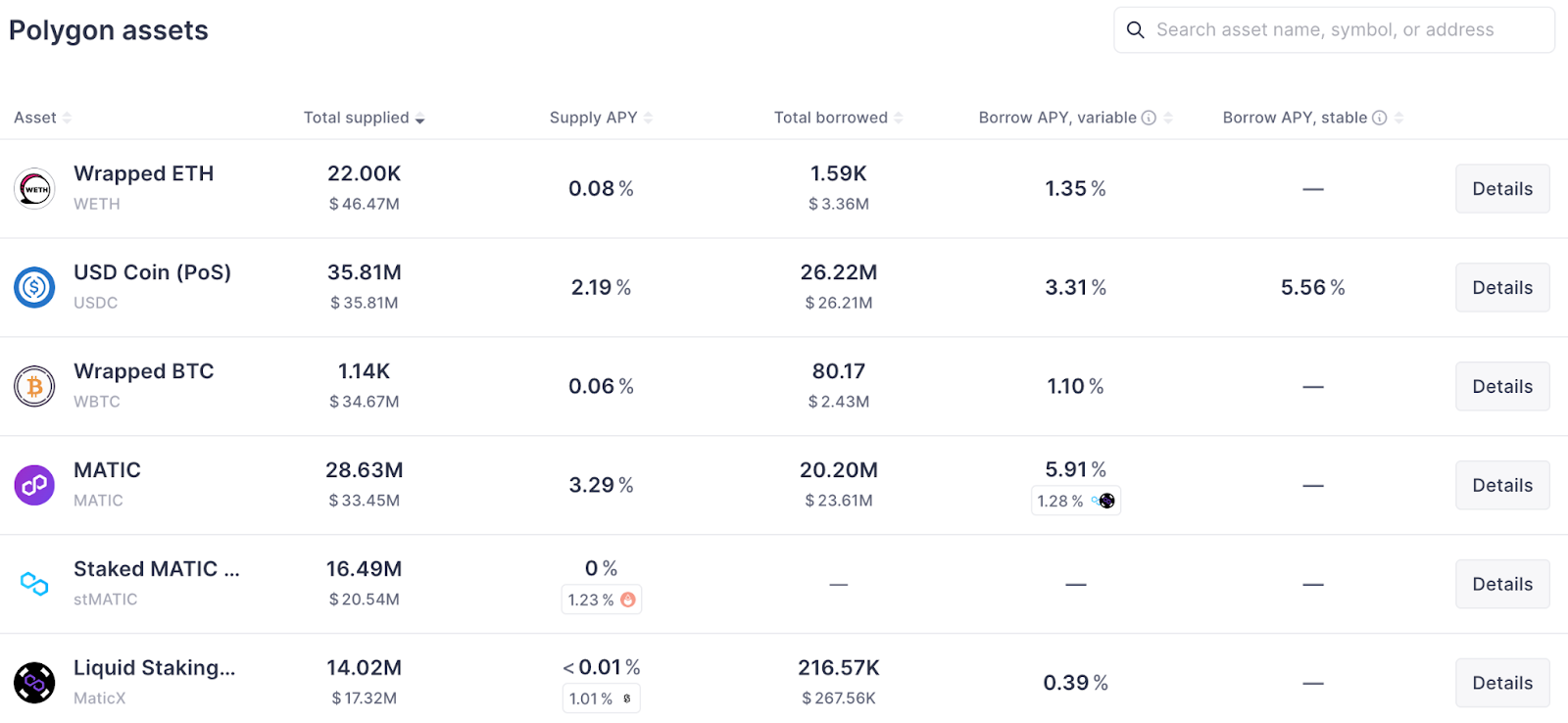

An example of Option 3, deposit wMATIC borrow USDC and swap for wMATIC for 2x leverage is affected by changing the RF as the deposit rate on wMATIC falls. But as wMATIC deposit rate is already low, 0.73% relative to 3.29% on v3. Increasing the RF from 20% to 36%, reducing deposit rate from 0.73% to 0.58%, 0.15%, will have less impact as increasing the borrowing costs on USDC from 2.99% to 3.40%, 0.41% via Option 2.

Uoptimal

Using Option 1 as an example, the revised Uoptimal parameter is the midpoint between current utilization and Uoptimal values. Ie: If utilization is 20% and the Uoptimal is 60%, then the proposed Uoptimal is 40%, the midpoint between the existing utilization and Uoptimal value.

Slope 2

By reducing the Uoptimal parameter, the gradient of the borrow rate between utilisations Uoptimal and 100% is lowered. In order to maintain the current gradient, the Slope2 parameter is revised higher. In the image below, Option 1, the Slope 2 parameter changes from 75% to 124% in response to the Uoptimal parameter being reduced from 80% to 60%. Notice how the red and blue lines are parallel during the second leg of the curve, this is because they have the same gradient.

Reserve Factor

As a portion of the interest paid by borrowers is directed to users who provide liquidity, by increasing the borrow rate, the deposit rate also increases assuming the reserves utilization remains unchanged. To counter the higher deposit rate, which encourages more deposits, the RF is increased. This redirects interest paid by borrowers to Aave instead of depositors.

Due to abnormally high USDT usage, 77.49% at the time of writing, this proposal suggests increasing the RF to be the average of proposed DAI and USDC RFs. The justification for this is to reduce the deposit rate of USDT, such that it encourages migration whilst avoiding reducing the Uoptimal such that borrowing cost increases substantially by shifting utilizing onto the more stepper portion of the yield curve. When utilization drops by a material amount, it would be prudent to reduce the Uoptiomal value in line with other stable coins.

Specification

The tables below detail the proposed parameter changes to achieve the outcome defined in the table above.

Prioir to any AIP submission the numbers should be updated in line with the strategy to avoid any un-favourable parameter configurations.

Next Steps

There will be a 1 week discussion window with a Snapshot to be posted on 26th April. Depending on the outcome of the vote, @defijesus will be working on preparing the payload.

Disclaimer

The author, TokenLogic, is only paid by Aave DAO via Butter as part of the Incentivised Delegate Campaign.

Copyright

Copyright and related rights waived via CC0.