Summary

LlamaRisk supports the onboarding of syrupUSDT to the Aave V3 Plasma instance. Consistent with our recommendation for syrupUSDC on Core, we advise adding syrupUSDT as a collateral-only asset, with its primary use case expected to be leveraged yield strategies through stablecoin looping. The key risks identified for syrupUSDT on Plasma include the absence of a timelock on syrupUSDT contract upgrades, on which the Maple team is actively working, with updates to follow.

Additionally, liquidity on Plasma is considerably concentrated: two EOAs together account for over 62% of all syrupUSDT liquidity, posing a potential risk of a liquidity crunch if either entity withdraws its funds. Moreover, Fluid is currently the sole DEX providing syrupUSDT liquidity, meaning that critical operations, including liquidations, depend entirely on the health of a single protocol infrastructure. Nevertheless, these factors largely reflect the nascent state of the Plasma ecosystem, where all deployments and liquidity bootstrapping have occurred within just two to three weeks.

Full Collateral Risk Assessment

1. Asset Fundamental Characteristics

1.1 Asset

According to the Asset Classification Framework (AAcA), syrupUSDT is classified as a yield-bearing stablecoin. It is backed by overcollateralized institutional loans underwritten and managed by Maple Direct. The current collateralization ratio stands at 162.4%, with BTC comprising 83.3% of the collateral. A portion of this backing is allocated to maintain readily available liquidity, equivalent to one-third of active loans, for redemptions. This liquidity is deposited across various DeFi protocols on Ethereum, including Aave. Consequently, the underlying yield is derived from both the active loans and the DeFi yield generated on the liquidity reserves.

syrupUSDT was deployed to Plasma on September 16, 2025, at the address [0xC4374775489CB9C56003BF2C9b12495fC64F0771](https://plasmascan.to/address/0xC4374775489CB9C56003BF2C9b12495fC64F0771).

1.2 Architecture

The primary architecture of syrupUSDT mirrors that of syrupUSDC, which was reviewed in detail during the syrupUSDC Core onboarding, and there have been no changes to its design or functionality. The core operations of syrupUSDT, including fixed-rate loan underwriting and liquidity management, are managed on Ethereum by Maple.

Issuance of syrupUSDT on Plasma is facilitated through Chainlink’s CCIP bridge, employing a lock-and-mint mechanism in which tokens remain locked in the LockReleaseTokenPool contract on Ethereum while syrupUSDT is bridged to Plasma. Conversely, transfers from Plasma back to Ethereum follow a burn-and-unlock mechanism.

Users can bridge syrupUSDT to Plasma via Chainlink’s Transporter, with the bridging process currently taking approximately 20 minutes. Bridging from Plasma back to Ethereum typically takes less than 2 minutes.

1.3 Tokenomics

The loan underwriting infrastructure for syrupUSDT resides on Ethereum; therefore, its supply on Plasma remains capped by the total amount of syrupUSDT minted on Ethereum, i.e., 400.2M. As of October 8, 2025, the total supply of syrupUSDT on Plasma stands at 344.6M.

1.3.1 Token Holder Concentration

Source: PlasmaScan, October 8, 2025

The top 5 holders of syrupUSDT on Plasma are:

- Fluid: 57.66% of the total supply.

- Euler syrupUSDT Vault: 29.69% of the total supply.

- Pendle YT syrupUSDT: 11.72% of the total supply.

- EOA 1: 0.27% of the total supply.

- EOA 2: 0.19% of the total supply.

The majority of syrupUSDT on Plasma is supplied to DEXs and lending protocols. While high utilization across DeFi protocols is generally positive, the concentration of activity within a few venues indicates that the syrupUSDT ecosystem on Plasma is still in an early and developing stage.

2. Market Risk

2.1 Liquidity

Source: syrupUSDT/USDT0 Swap Liquidity, Fluid, October 8, 2025

On Plasma, users can swap up to 10.63M syrupUSDT (worth $11.66M) for USDT0 with a maximum price impact of 5.16%, which corresponds to the point where the pool reaches its current ~$11M withdrawal limit on USDT0.

2.1.1 Liquidity Venue Concentration

Source: syrupUSDT Liquidity Pools on Plasma, GeckoTerminal, October 8, 2025

Nearly all syrupUSDT liquidity on Plasma is concentrated in Fluid’s USDT0/syrupUSDT pool, which holds a total TVL of $40.1M. The pool consists of $22.1M in USDT0 deposits and $18M in syrupUSDT. However, a withdrawal limit of $11M is currently imposed on USDT0, meaning users cannot sell more than $11M worth of syrupUSDT.

2.1.2 DEX LP Concentration

On Plasma, syrupUSDT liquidity is considerably concentrated, with 40% of the Fluid pool’s liquidity supplied by a single EOA, followed by another EOA holding 22.4%. This concentration poses a potential liquidity risk if either of these entities decides to withdraw its funds.

2.2 Volatility

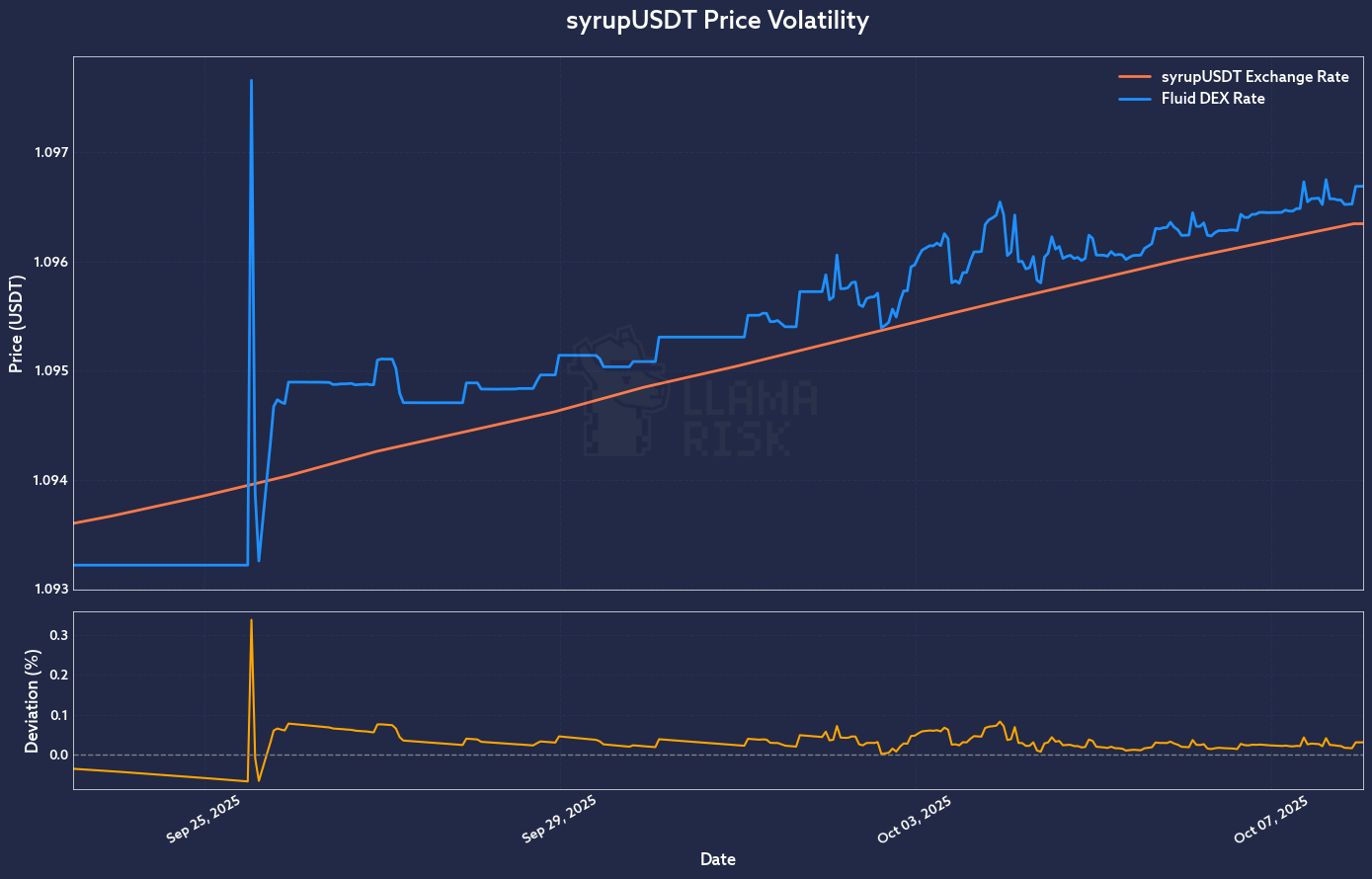

Source: LlamaRisk, October 8, 2025

Since launch, the syrupUSDT Fluid pool on Plasma has traded consistently within a 10 bps range, except for a single instance on September 25, 2025, when it experienced an upward deviation of 32 bps. However, as the pool has been live for less than a month, the available data remains insufficient for drawing high-confidence conclusions.

2.3 Exchanges

syrupUSDT is exclusively traded on DEXs and is not currently listed on any centralized exchange.

2.4 Growth

Source: syrupUSDT Circulating Supply, Dune, October 8, 2025

To date, a total of 400.2M syrupUSDT has been minted on Ethereum, with the majority supplied on Ethereum prior to locking and migration to Plasma. Since syrupUSDT is currently issued only on Ethereum, its total supply growth on Plasma remains capped by the available circulating supply on Ethereum, which stands at 55.6M as of now.

3. Technological Risk

The technological risks associated with syrupUSDT on Ethereum, including smart contract risk, bug bounty coverage, and dependency risk, remain unchanged from our syrupUSDC Core onboarding review and are omitted here for brevity, as the underlying architecture is identical. On Plasma, however, an additional dependency exists on Chainlink CCIP due to its role in facilitating cross-chain syrupUSDT transfers between Ethereum and Plasma.

4. Counterparty Risk

4.1 Governance and Regulatory Risk

The regulatory risk has been previously discussed in detail as part of the syrupUSDC Core onboarding review. As there have been no material changes, that assessment remains applicable here.

4.2 Access Control Risk

4.2.1 Contract Modification Options

Here are the syrupUSDT controlling wallets on Plasma:

- Multisig A: 3/5 threshold Safe, admin of syrupUSDT contract.

- RBAC Timelock: Chainlink MCMS-controlled wallet, owner of the BurnMintTokenPool. Pool ownership will eventually be transferred to Maple, but there is no tentative timeline yet.

The following contracts power the syrupUSDT architecture on Plasma:

- syrupUSDT: ERC20 contract for the syrupUSDT token, deployed as BurnMintERC20, and is controlled by the Multisig A.

- BurnMintTokenPool: Pool implementation responsible for minting/burning tokens (syrupUSDT) on the destination chain (Plasma) and is owned by the RBAC Timelock.

syrupUSDT employs a role-based access control framework to manage sensitive functions:

| Controlling Addresses | Role | Functionality |

|---|---|---|

| Multisig A | DEFAULT_ADMIN_ROLE | Can change all privileged roles |

| BurnMintTokenPool | MINTER_ROLE | Can mint syrupUSDT on Plasma |

| BurnMintTokenPool | BURNER_ROLE | Can burn syrupUSDT on Plasma |

4.2.2 Timelock Duration and Function

No timelock has been deployed on syrupUSDT Plasma contract upgrades.

4.2.3 Multisig Threshold / Signer identity

Multisig A is controlled by the Maple team. The signers are:

- 0xdBdAc09AB7832cF93DDaFCf112fd082010E1394d

- 0x06aa475f597b9f404d6cF443A19392a2936a9A2E

- 0x46aEE00f1AF171d0d50BF3Db2FD93Da8a121d851

- 0x71F45a14d5e33dE6587F3C35f0F5dE8106386cfC

- 0x9C8238D93132EDacbf38fB3609257Da27498A535

Note: This assessment follows the LLR-Aave Framework, a comprehensive methodology for asset onboarding and parameterization in Aave V3. This framework is continuously updated and available here.

Aave V3 Specific Parameters

Will be presented jointly with @ChaosLabs

Price feed Recommendation

Chainlink’s syrupUSDT/USDT Exchange Rate feed, combined with the USDT/USD base feed and CAPO can be used to price syrupUSDT on Aave’s Plasma market.

Disclaimer

This review was independently prepared by LlamaRisk, a DeFi risk service provider funded in part by the Aave DAO. LlamaRisk is not directly affiliated with the protocol(s) reviewed in this assessment and did not receive any compensation from the protocol(s) or their affiliated entities for this work.

The information provided should not be construed as legal, financial, tax, or professional advice.