Hi Aave ![]()

Llama has conducted an analysis on the performance of the Safety Module and we would like to share our findings with the broader community. We mentioned a few considerations for the community to discuss which can then be incorporated into a future proposal.

Introduction

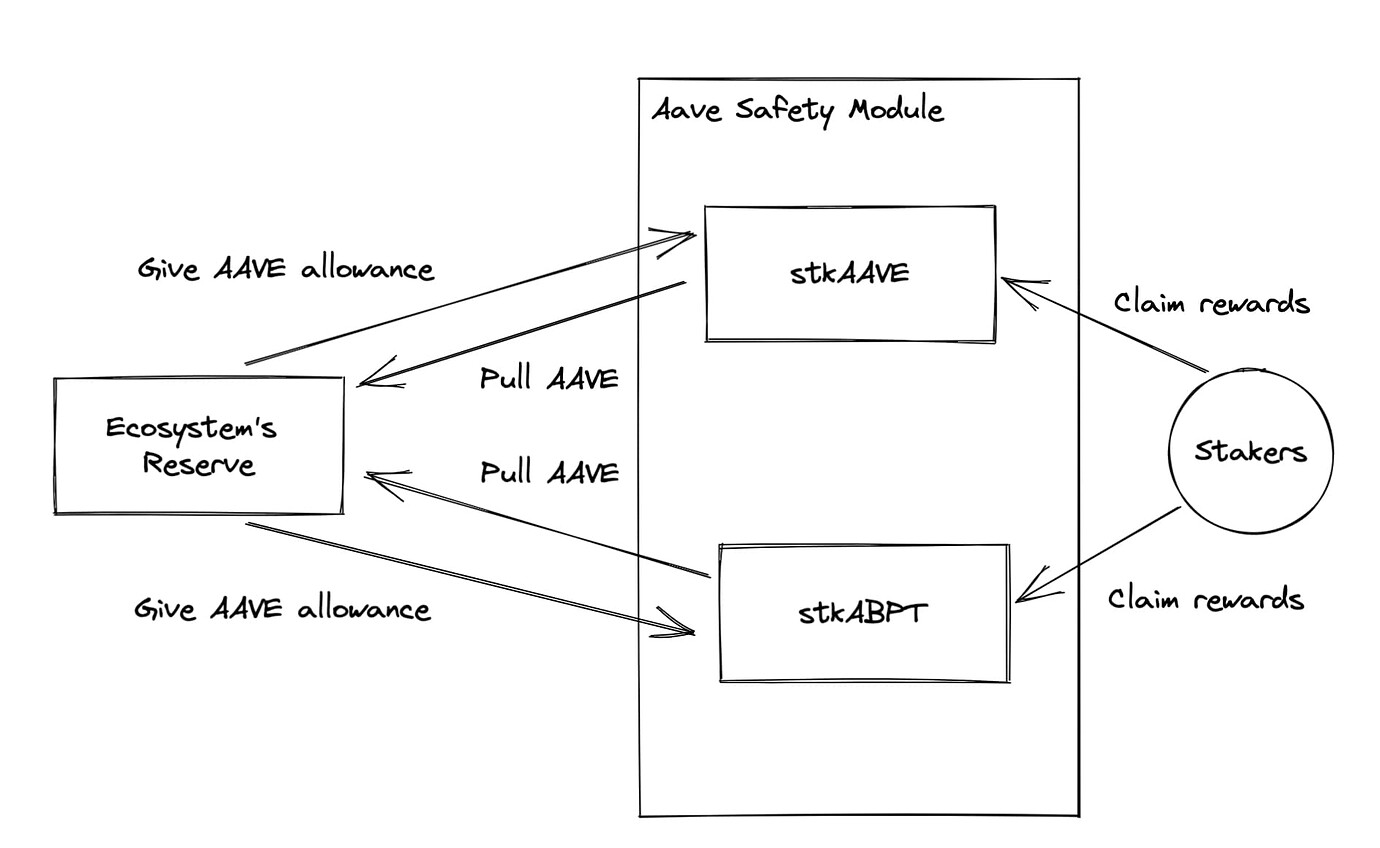

To start, as a refresher on the Safety Module (SM).

Two tokens can be deposited and staked in the SM. These are AAVE and the Balancer v1 80AAVE20wETH (ABPT) liquidity token. By depositing AAVE and ABPT in the SM, depositors receive stkAAVE and stkBPT respectively, along with yield nominated in AAVE. 550 AAVE are distributed daily to users who stake AAVE and another 550 AAVE is distributed daily to depositors who stake ABPT. In return for the AAVE yield, depositors are risking up to 30% of their capital by providing a backstop for the Aave markets.

Aave governance can in the event of a shortfall, auction off up to 30% of the assets held in the SM. A cool down period exists to prevent depositors from withdrawing their capital from the SM before the governance process auctions AAVE and ABPT to replace the funds lost by Aave users. If greater than 30% of the SM is needed, the Aave community has the ability to mint and auction new AAVE tokens on market.

For more details on the SM, please check out this Aavenomics link.

Analysis

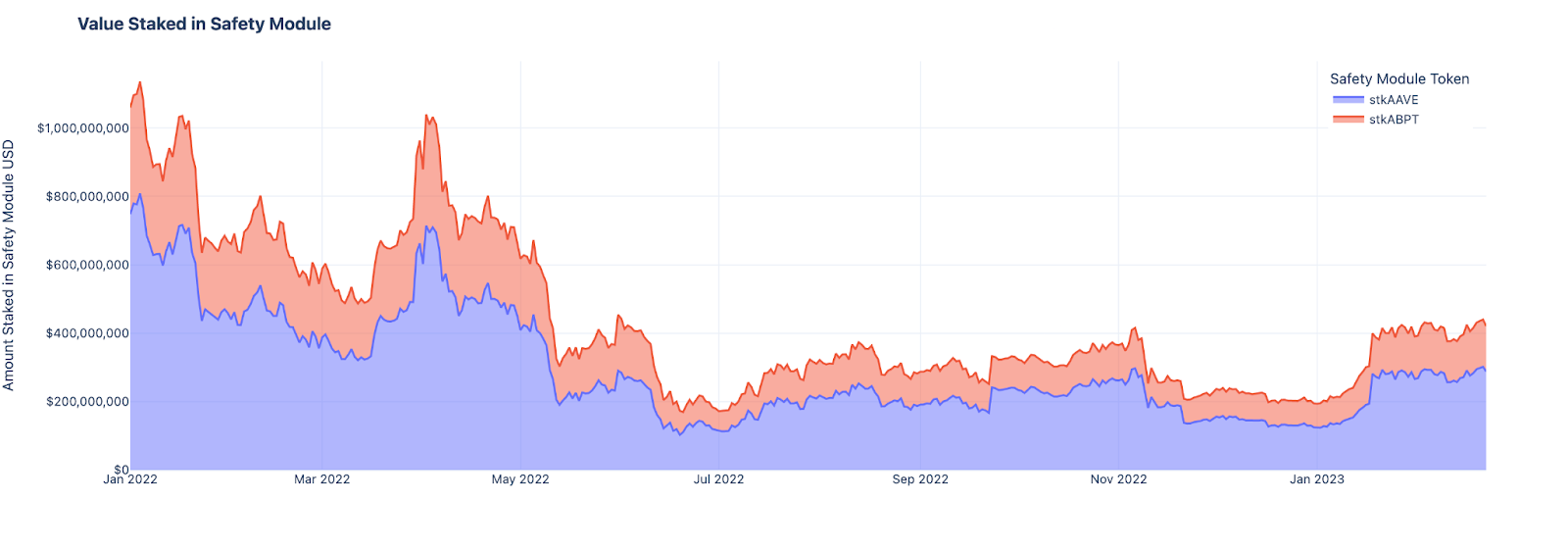

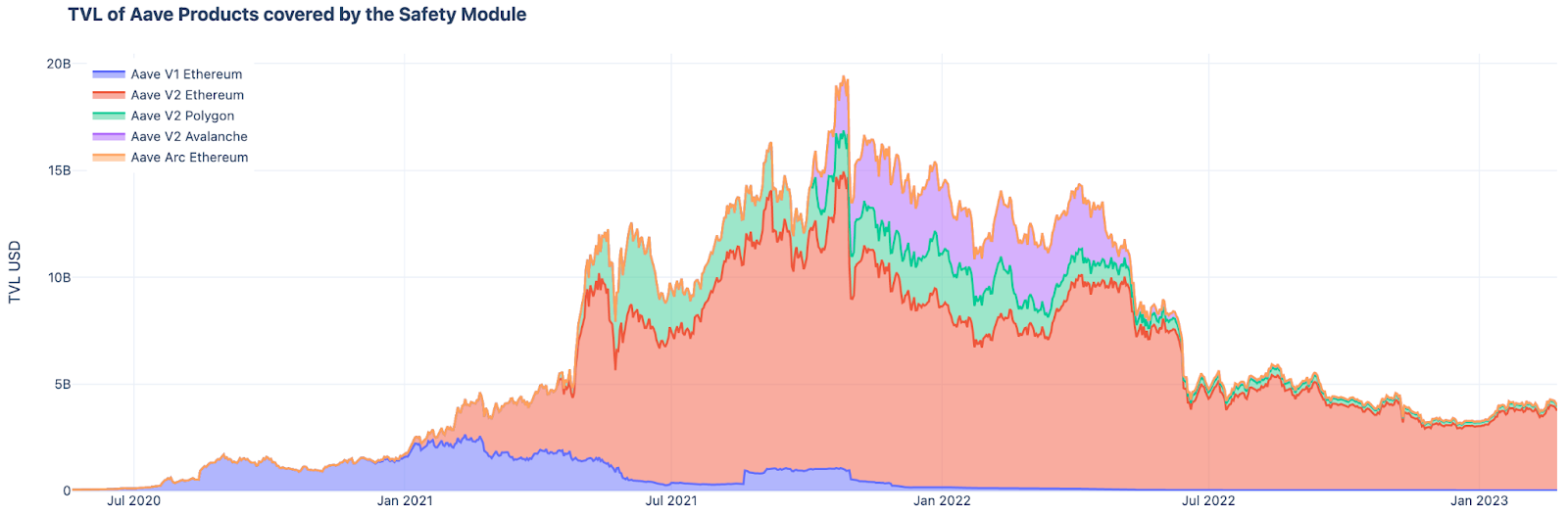

The image below shows the composition of the SM and indicates most of the Shortfall Coverage is provided by AAVE depositors. Do note that the ABPT is utilising Balancer v1 and Balancer v2 was launched early in Q2 2021.

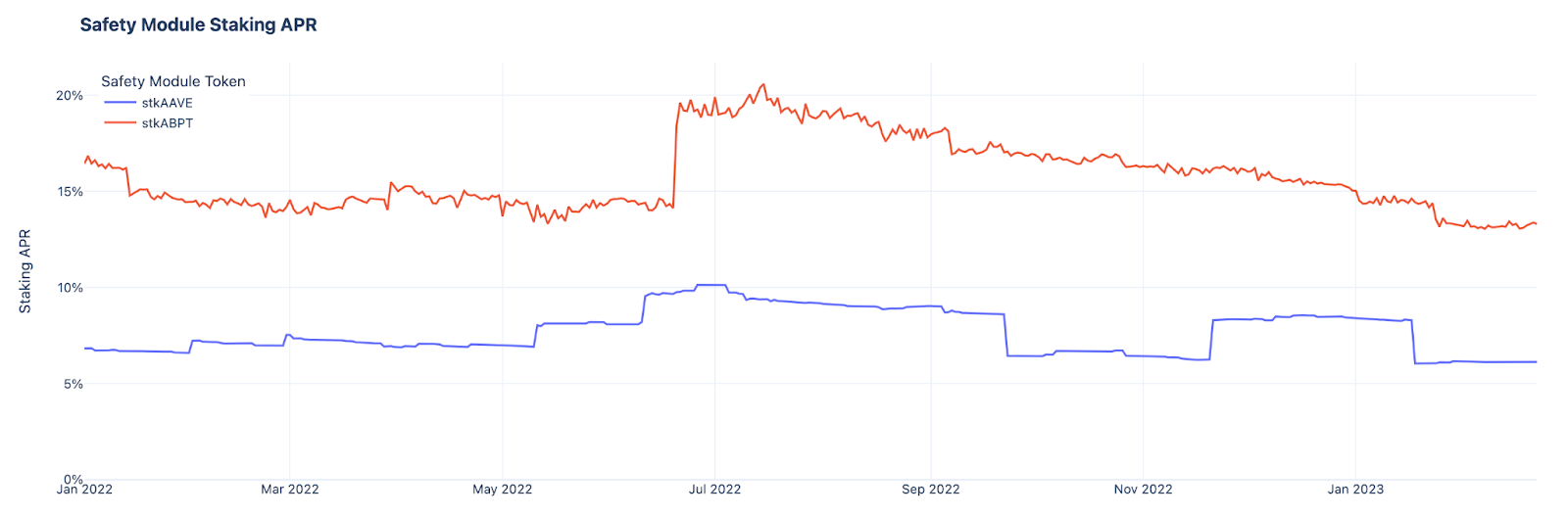

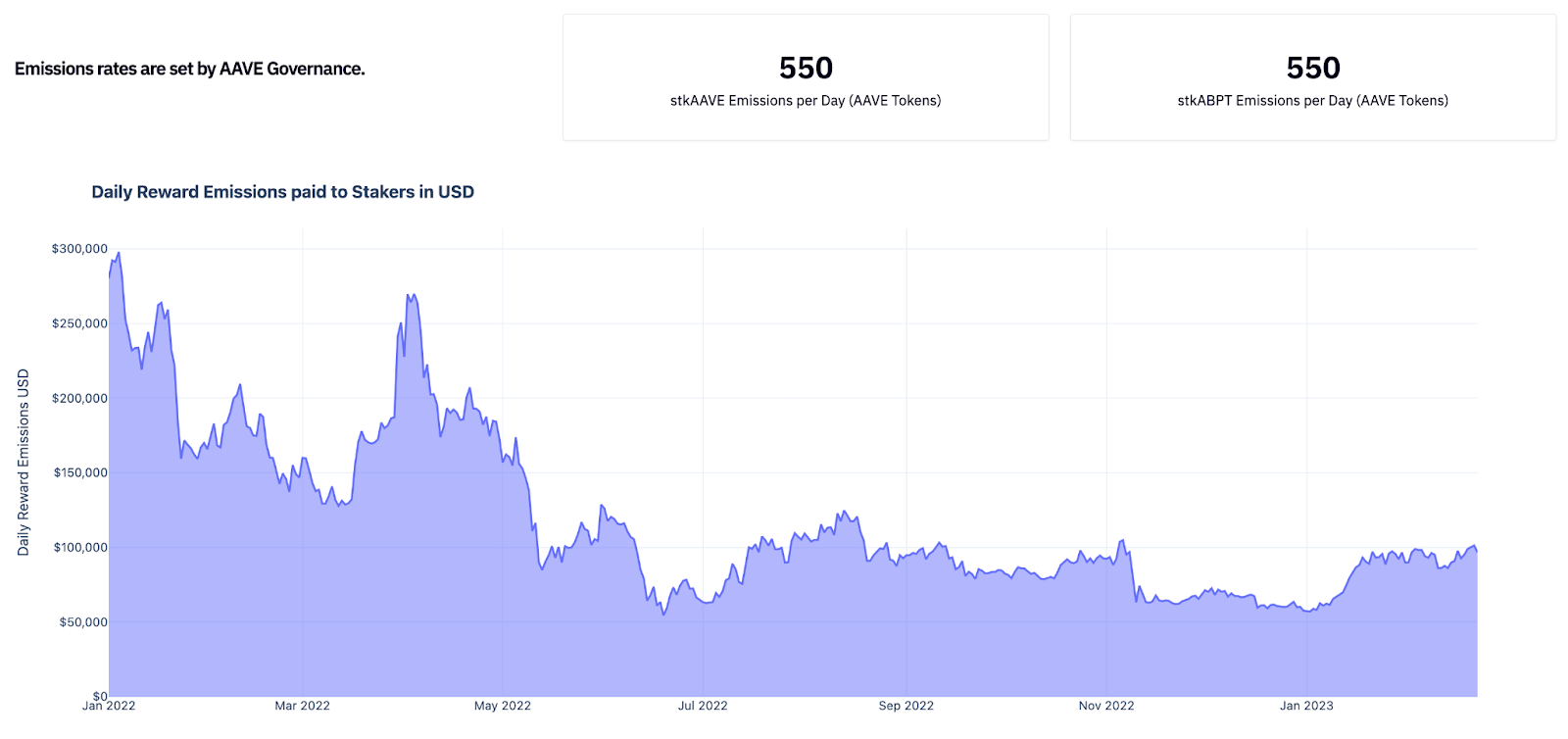

The SM provides around a 6.13% APY on stkAAVE deposits and 13.3% APY on stkABPT deposits. During June 2022, the AAVE emissions to stkABPT and AAVE deposits was renewed.

The annual spend, 398,200 AAVE, is worth $32.12M at $80/AAVE and is heavily dependent upon the price of the AAVE token. The chart below shows the daily expense being accrued by Depositors, ie: 1,100 AAVE/day x Spot Price, to be around $88,000 per day from mid May 2022 to mid August 2022.

Daily SM spend is $88,000 at $80/AAVE

Annual SM spend is $32,120,000 at $80/AAVE

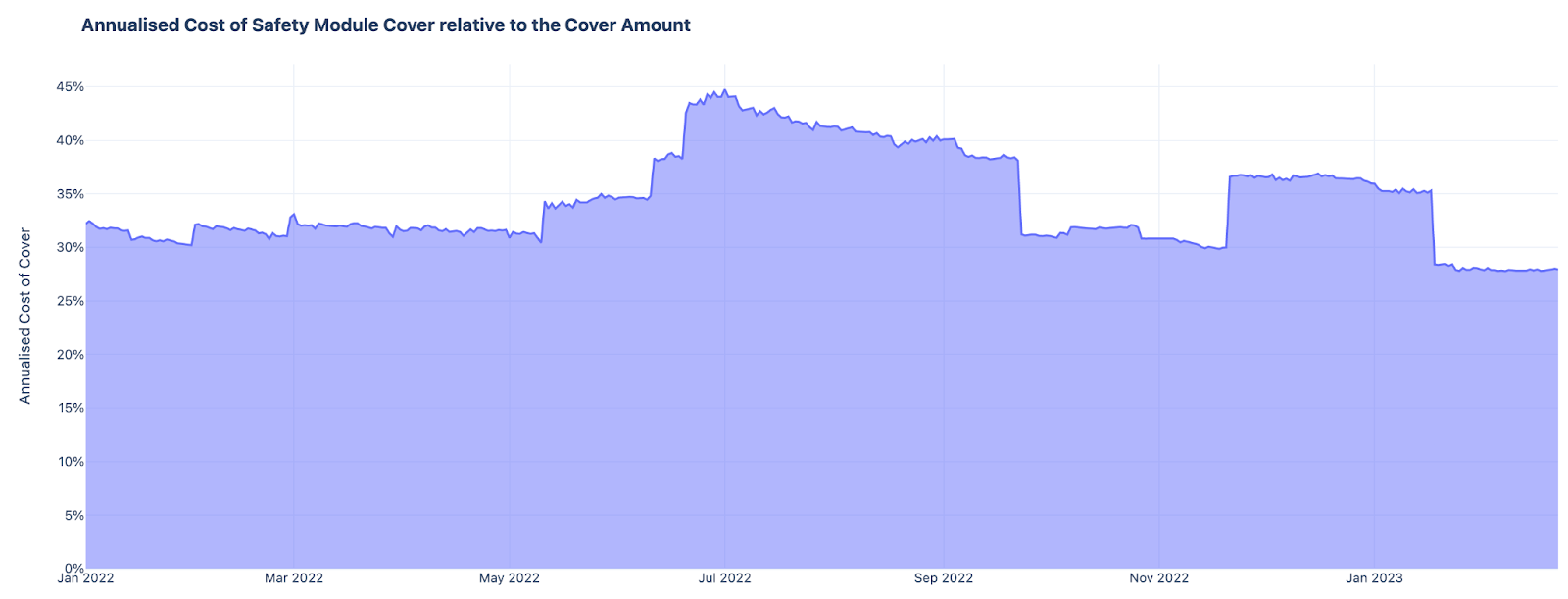

In return for 1,100 AAVE/day in SM emissions, the community receives $126.1M of shortfall coverage, defined as 30% of the funds deposited in the SM. The value of the Protocol Coverage is volatile, fluctuating from about $340M to $52M during 2022.

The combined TVL across these markets is $3.73B. Do note, this only includes the following deployments and does not reflect the recent Ethereum v3 deployment inclusion.

- Ethereum v1 market

- Ethereum v2 market

- Ethereum ARC market

- Avalanche v2 market

- Polygon v2 market

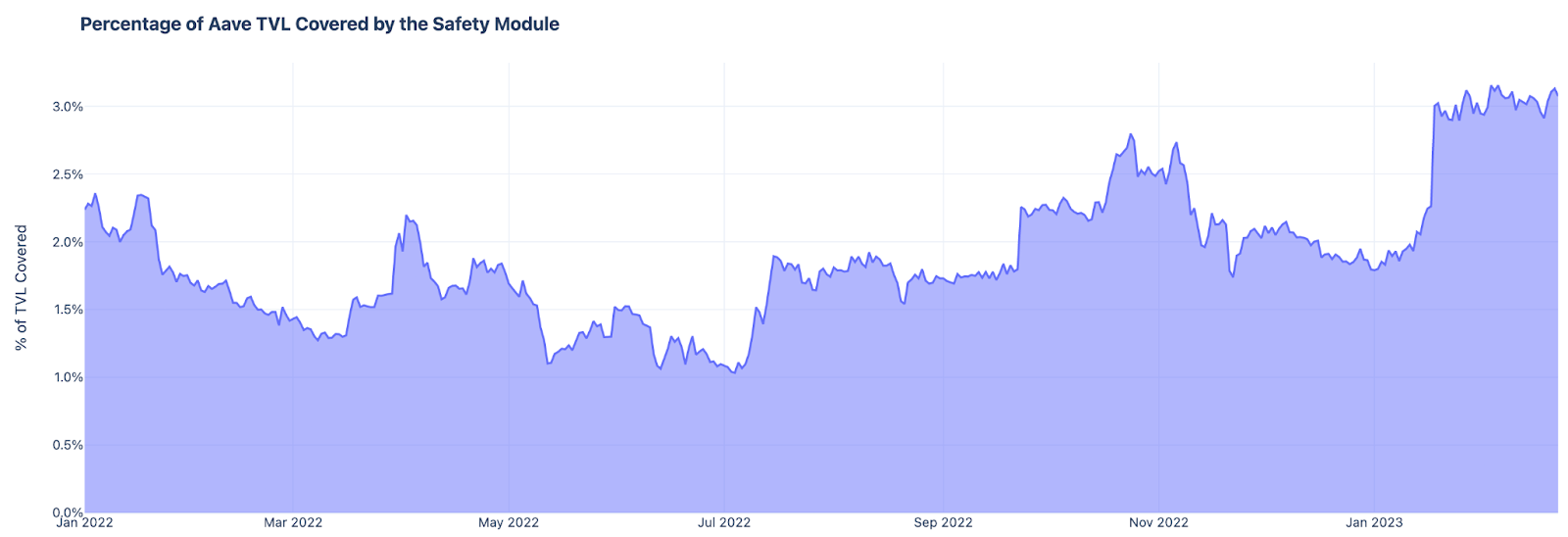

The “Percent of Aave’s TVL Covered by the Safety Module” chart shows below. It ranges from 1.0% to 3.0% of total TVL for the covered Aave deployments.

The chart below shows the value of the AAVE emissions divided by 30% of the value staked in the SM. ie: the cost per $ of actual coverage. The yield ranges between 27.8% and 44.8%.

Annual $32.12M in AAVE emissions at $80/AAVE whilst receiving $126.1M of actual Short Fall coverage.

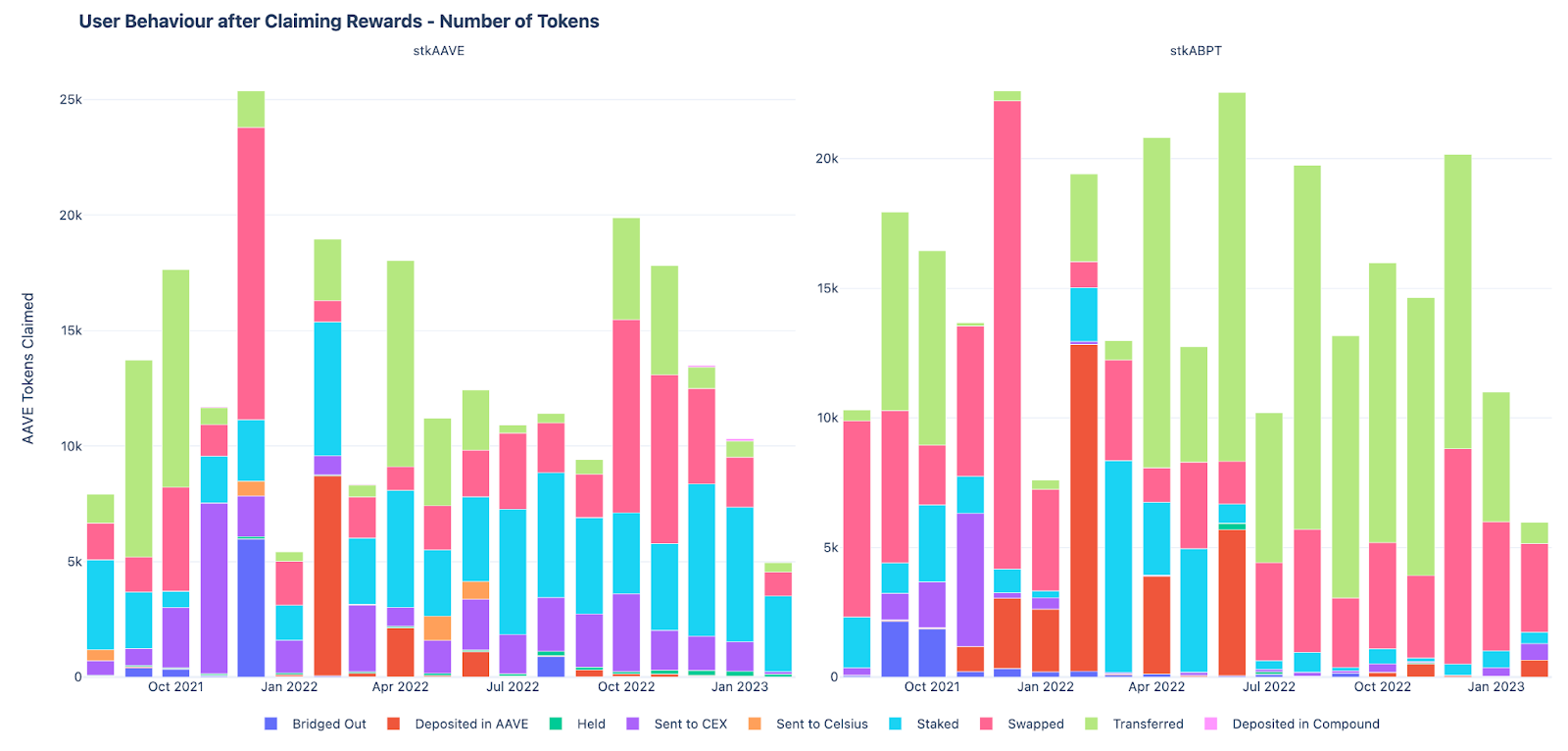

Diving a little deeper, the below chart shows the amount of AAVE being claimed each month varies greatly and that most of the AAVE is either transferred to another wallet, swapped for another asset or compounded by staking to earn more AAVE yield.

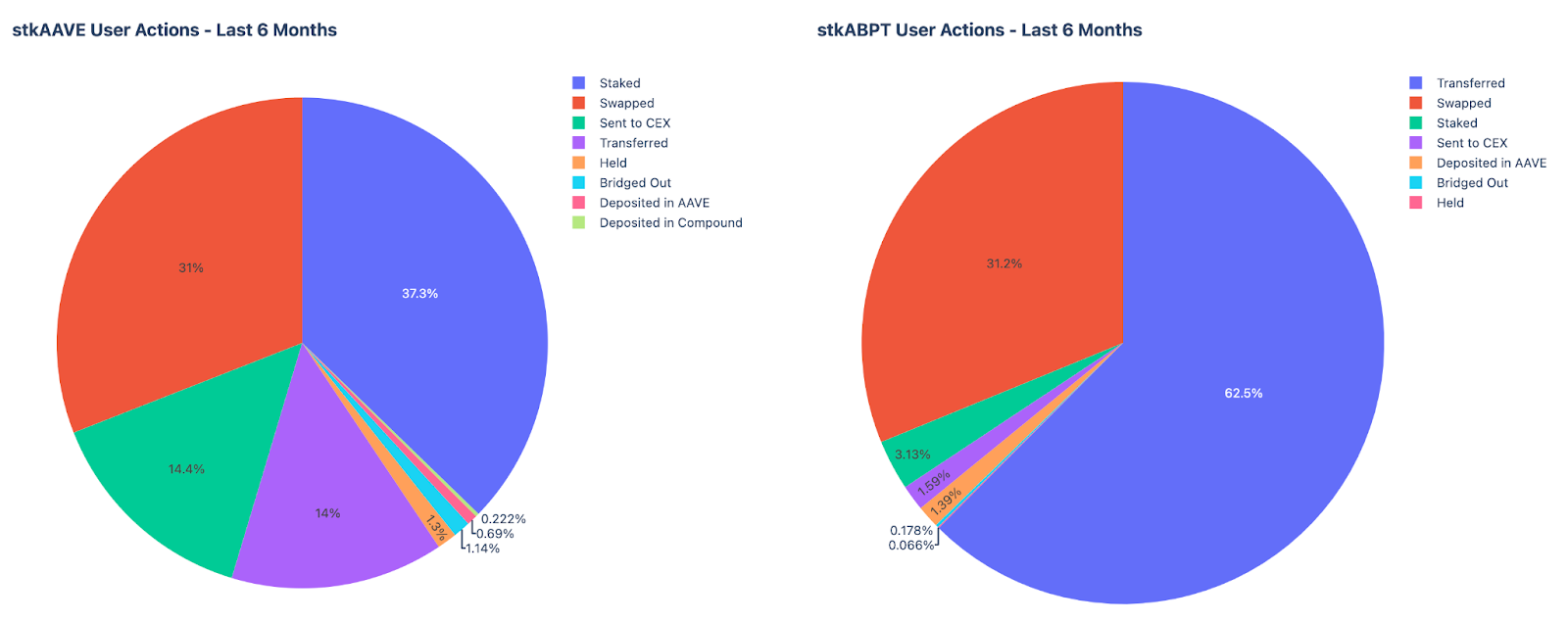

The charts below show the next action taken by depositors who receive AAVE from the SM. 37.3% of AAVE claimed by stkAAVE depositors is staked and compounded. 53.9% of AAVE emission received by stkABPT holders is transferred to another address. 31.4% and 38.4% of AAVE received by stkAAVE and stkABPT holders is swapped, sold, on market.

Discussion

(LST = Liquid Staking Token)

The below summarises well known topics relating to the SM within the community:

- SM is over exposed to a single asset, AAVE

- Auctioning AAVE in the event of a Shortfall can lead to front running, which can have an adverse effect price, causing a greater amount to be auctioned

- Introducing additional, or alternative assets, into the SM will reduce the dependence on a single asset

- Increasing the amount (30%) auctioned off in a shortfall event will increase Protocol Coverage, but may require a higher yield to compensate for risk

- Introduction of Snapshot has increased the overall governance process duration

- Extend the Cool Down period to be realigned with Governance process duration

The below summaries the notable findings from this analysis:

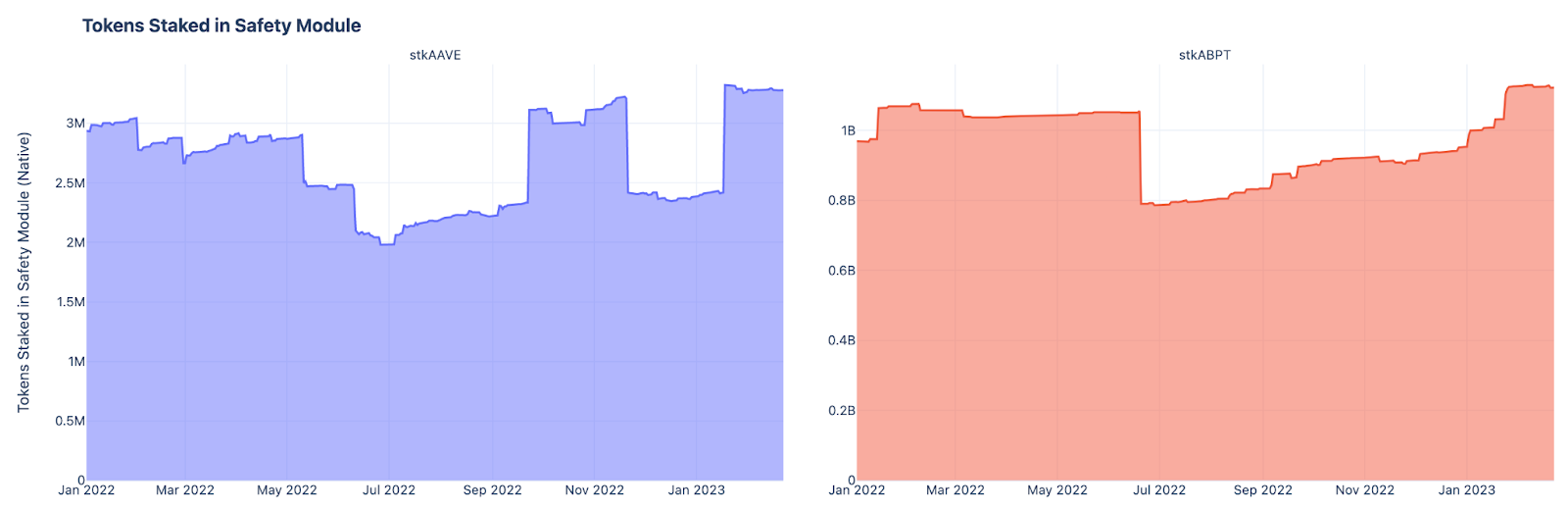

- Assets held within the SM are volatile and broadly aligned with TVL

- Dollar value of Protocol Coverage fluctuates with the broader market

- 30% shortfall coverage is not scalable and greater capital efficiency is needed

- Overall spend on SM is high relative to DAO’s revenue

- Annualised SM spend - $32,120,000 at $80/AAVE

- Annualised Revenue - $16.3M

- Notable portion of SM emissions are being sold on market indicating users prefer yield in an alternative asset

- Balancer v1 is obsolete and the ABPT pool requires migration to Balancer v2

- Opportunity to revisit the 80AAVE20WETH composition of the pool

- Balancer’s tokenomics has changed, Aave SM incentives should be additional to Balancer / Aura gauge yield.

The following bullet points introduce concepts for discussion in the comments section below:

-

Include non AAVE emissions - Eg: GHO, to reduce sell pressure on AAVE

- A portion of the GHO revenue can replace or complement AAVE emissions

- Potential to reduce AAVE sell pressure, especially if depositors can choose what token is to be received. This is similar to cvxCRV staking.

-

Shortfall coverage tiers - Auction off varying portions of deposits in the event of a Shortfall. Examples: 30%, 45% and 60%. Aave can elect to offer higher yield for higher Shortfall coverage. The type of assets included, amount (ceiling) and composition can all be controlled by Aave governance.

- Reduce AAVE weighting when migrating from Balancer v1 ABPT to v2 and introduce additional pools which could lead to price arbitrage triangles like shown below. (This is an idea, for discussion, not a recommendation). More importantly introduce GHO pools to the SM and reduce the composition of AAVE in each pool.

- Realise synergies with bootstrapping adoption of GHO whilst encouraging greater GHO liquidity. Ie: GHO/LST

-

Develop an equivalent contract which enables deposits into the SM to earn rewards from Curve, Convex, Balancer, Aura and others. This is to showcase something that could be done but would introduce a lot of risk surface area. The community does need to consider the holistic Aave exposure to one protocol from a risk perspective.

-

Introduce a Bad Debt budget backed by assets held in the Collector Contract that acts as the first source of liquidity for excessive debt repayments.

Next Steps

Depending upon feedback in the comments, the two topics that can be progressed via their own ARFC proposal in the near future:

-

AAVE liquidity pools

- Pivot away from AAVE/wETH (80/20)

- Migrate to Balancer v2

- Consider core pool status on Balancer (>50% pool is productive, ie: LST)

- Create an AAVE pool on another DEX

- Future AAVE/GHO or GHO pools considerations

-

Introduce a Bad Debt budget

- Nominal amount of annual budget allocated to paying down excessive debt

- Guidelines for how /when this would be called upon, ie: avoid SM Auction as excessive debt is less than Bad Debt budget

- CRV bad debt was $1.7M, initial budget of $2M could be considered

Thank you for taking the time to read this discussion post and learning more about the Aave SM. We look forward to reading your comments below and welcome your feedback.

This post was prepared by Llama contributors: DeFi_Consulting (@MatthewGraham), @Dydymoon, @scottincrypto and @schlabach.