Introduction

RociFi is a protocol building the two key pillars of Web3’s future – on-chain credit scores and under-collateralized lending. The credit scoring is powered by our non-fungible credit score (NFCS), which ranks users according to their likelihood of repaying an under-collateralized loan. The scale is 1 to 10 with 1 being the best score and 10 being the worst.

For reference, NFCS is built using RociFi protocol repayment data and other DeFi protocols; including Aave and Compound. The depth and breadth of data allows the NFCS to be the clear leader in on-chain credit scores which has applicabilities to other lending protocols.

In particular, lending protocols like Aave could use RociFi NFCS to achieve better capital efficiency by offering higher LTVs to higher scored borrowers – generating greater revenues without a demonstrable increase in insolvency risk – akin to a micro-level Gauntlet.

The best part is that the NFCS API is open to any developer or protocol to call for real-time scores of any NFCS holder, thus they could integrate this score based on each protocol’s individual needs.

Revenue Increase

Below we provide comparisons of the revenue Aave and Compound generated historically and what they would have generated using RociFi NFCS scores for higher capital efficiency. The following LTVs used for revenue simulations are per score:

Aave

Using a simulation period from December 2020 to Aug 2022, we compare the estimated total and monthly gross revenue Aave would have earned with and without RociFi NFCS on Aave V2 (ETH, Avax, Polygon), and Aave V3 (Arbitrum, Optimism, Polygon, Avalanche, Fantom); assuming an APR of 8%.

Using RociFi NFCS would have generated revenue of ~$256,308,772 while without only earned ~$132,491,204. By being able to offer higher LTVs, Aave would generated an additional $123,817,568 in value (net of liquidations) with a negligible increase in insolvency risk.

Tokens Considered : [‘DAI’, ‘USDC’, ‘USDT’, ‘EURS’, ‘agEUR’, ‘jEUR’, ‘AAVE’, ‘LINK’, ‘WBTC’, ‘WETH’, ‘WMATIC’, ‘CRV’, ‘SUSHI’, ‘GHST’, ‘DPI’, ‘BAL’], these were simulated with the following LTV’s : [0.97, 0.97, 0.97, 0.97, 0.97, 0.97, 0.6, 0.5, 0.7, 0.8, 0.65, 0.75, 0.2, 0.25, 0.2, 0.2]. Note that Revenue simulations assume no default

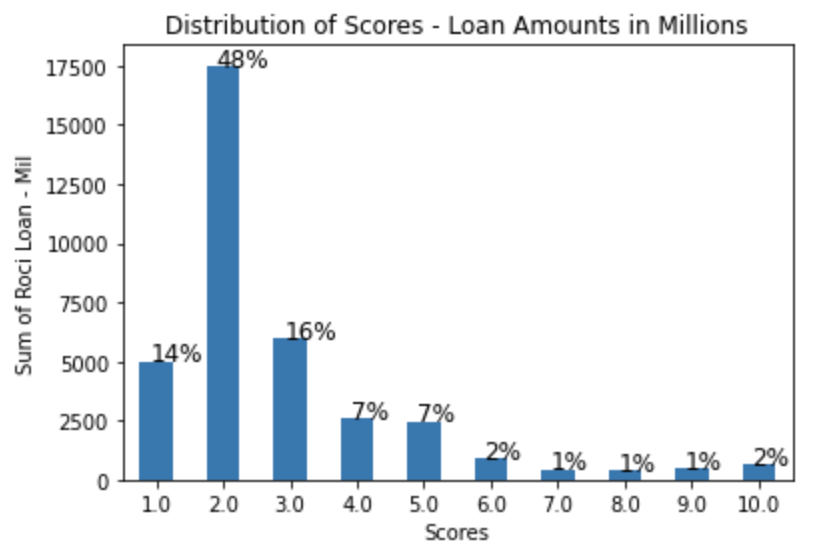

By scoring borrowers with the NFCS, Aave is able to achieve better capital efficiency by not penalizing responsible borrowers, enabling higher loan allocation to this subgroup, i.e. give good borrowers more loans and less to worse borrowers. This simple heuristic is illustrated in the distribution of loan amount by score chart below.

Using RociFi NFCS, despite higher LTVs, a heavy concentration of Aave loan volume went to the very best borrowers, i.e. credit scores 1-5, comprising 92% of total loan volume issued. Thus, increased revenue with minimal increase in insolvency risk.

Conclusion

Integrating onchain credit scores from RociFi NFCS allows existing lending protocols to offer more competitive LTVs, thus higher risk-adjusted revenues. Additional positive byproducts of adopting RociFi NFCS by protocols are (1) incremental revenue can be passed back to the community and (2) better product attractiveness via higher LTV for borrowers with lower rates, and higher supply rates to lenders.