[ARC] - ERC4626 Strategies as Productive Collateral

Status: Discussion

Author: @llamaxyz, @MatthewGraham @Dydymoon

Created: 24-10-2022

Summary

@Llamaxyz is proposing the introduction of a new productive collateral type that allows users to earn the rewards of other protocols by depositing into Aave v3 Reserves.

With the support of the community, Llama will develop ERC4626 strategies that enable Balancer v2 and Curve Liquidity Provider tokens to be deposited as collateral. Users will earn the rewards from the respective Aura Finance and Convex Finance gauges whilst being able to draw a loan against the productive strategies.

This new type of collateral is expected to drive borrowing demand for listed assets and generate additional revenue for Aave DAO by sending 5% of the earned rewards to the DAO.

Introduction

To support the continued growth of Aave, new types of collateral are needed to unlock emerging segments of the market. Llama proposes onboarding productive assets that are supportive of enhancing capital efficiency through unlocking new utility for user funds.

Currently, there is $4.4B deposited in Convex Finance and Aura Finance, and when Optimism enabled liquidity mining on Aave v3, Total Value Locked (TVL) on Aave increased almost 13x from $36M to $460M. Llama seeks to create the new type of collateral standard and onboard the first BPT and crvLP as collateral on the Ethereum v3 Liquidity Pool.

The new collateral type will be listed with SupplyCaps in place, borrowing disabled, and eMode created to shape how users interact with the new pools.

Motivation

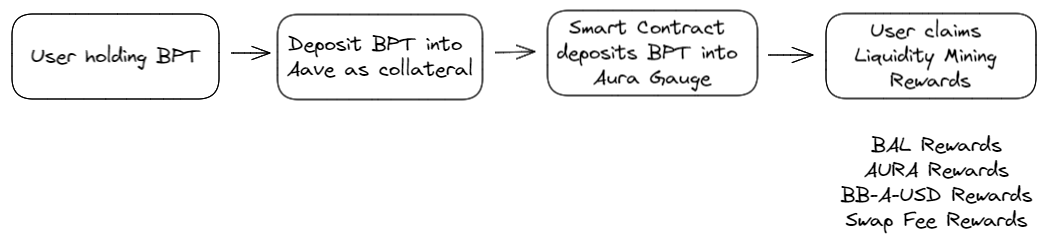

To understand how this strategy works, we will first walk through an example that demonstrates the user experience. In this example, the user deposits a BPT into Aave and claims rewards generated by the Aura Finance Gauge.

The use,r having already invested in a Balancer v2 Liquidity Pool, deposits the BPT into the Aave Reserve and receives back aBPT. The Aave Reserve receives the user’s BPT and deposits it into an Aura gauge. The rewards generated from staking the BPT in the Aura Finance gauge are claimable by the user without needing to redeem the BPT deposit. When the user claims the rewards, 5% are sent to the DAO and 95% to the user.

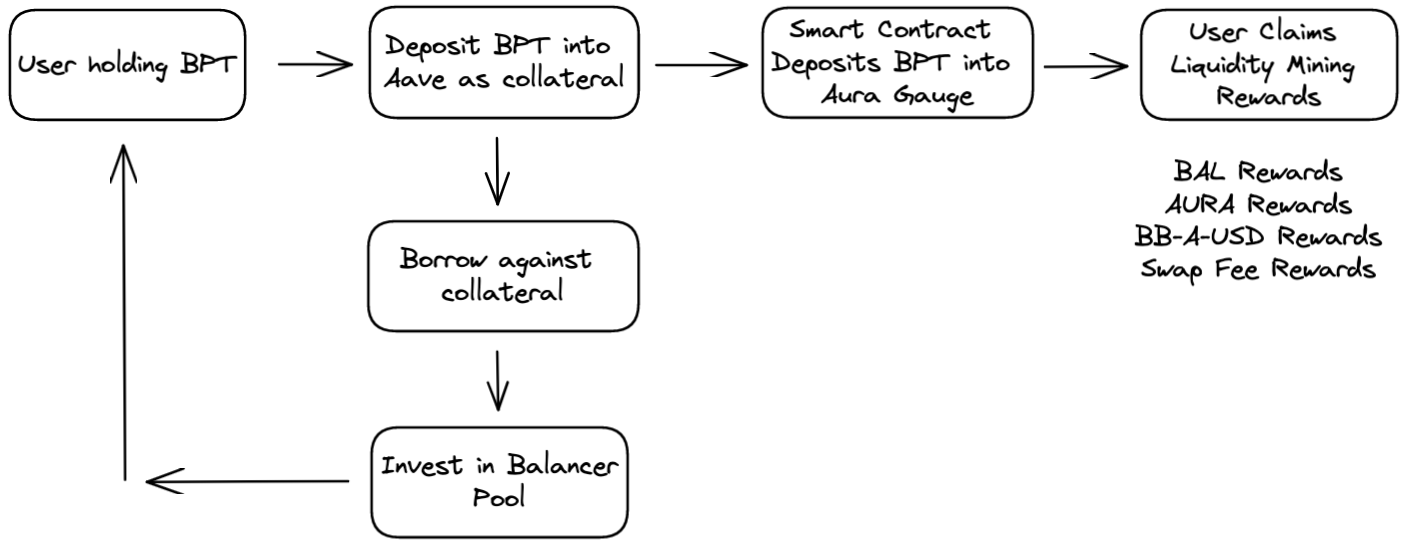

The productive strategy can also be used as collateral.This creates much more utility for BPTs as users can then borrow against the productive strategy. Apart from levered farming of rewards, users can create buy-now and pay-later strategies that utilize future incentives to pay back the loans. This also creates an opportunity for other communities to build automated strategies that manage rewards and collateralization ratios for users that further streamlines the user experience.

The DAO can decide if pools such as Balancer Boosted Aave Pool (bb-a-USD) and future GHO pools, (bb-a-USD / GHO) can be listed as collateral. Leverage in this application would exhibit similar recursive behavior to that which is occurring on Optimism and could lead to significant volumes of GHO entering circulation over time. If this was to occur, it would have a positive effect on the DAO’s revenue.

It is important to note that, although this proposal mentions Balancer and Aura Finance, the same concept applies to Curve and Convex. The initial deployments are to utilize Aura gauges, with a Convex integration to follow.

Next Steps

A Snapshot will follow this ARC to determine whether the community would like to move forward with creating this new type of collateral.

If the community votes positively for the development of the upgrade to enable the new type of productive collateral to be onboarded, Llama will set about designing and creating the upgrade. Llama will commit to following best practices and working closely with other stakeholders within the community in developing the new collateral type. In the lead up to deployment on the Aave protocol, further governance approval will be required.

In the future, the community will also be able to decide via Snapshot whether to provide retroactive funding to reimburse the cost associated with the auditing of the new collateral type and how much funding to provide.

A separate Snapshot proposal will emerge where the initial asset listing will be proposed, with contributors such as Gauntlet and others potentially playing a role. Upon agreeing on the initial asset to be listed and whether audit costs are to be reimbursed, an on-chain vote will be submitted for governance approval to transfer funds and introduce the upgrade. This loosely follows the methodology presented in the GHO proposal.

Conclusion

This ARC is focused on introducing and getting community feedback on introducing Aave’s newest productive collateral to the protocol.

We look forward to hearing community feedback on all aspects of this proposal.