Aave community,

At Delphi, we’ve been working closely with the Aave team over the past few months in order to help guide the Aavenomics design, oversee the transition to Aave 2.0 and participate in community governance. As part of this, we’ve been hard at work designing a new Aave token architecture which we believe will enable greater capital efficiency, innovation, and robustness.

You can read the full 32 page proposal here, but we’ve also included a shortened version below. The full report is more comprehensive, includes a lot of helpful diagrams as well as an example model to help illustrate our design in action, so we recommend you check that out instead.

We look forward to receiving feedback from the Aave community on this and iterating together towards the best solution.

Introduction

Aave has become a leading crypto credit platform, with $1.4B in deposits. Impressively, it has both achieved and maintained this without deploying liquidity mining incentives, meaning Aave depositors are loyal users that have chosen to stay despite the more attractive yields offered elsewhere. This is a testament to the quality of Aave’s product and community.

However, we ultimately see lending becoming a “balance sheet as a service” business. This is an extremely competitive market since anyone that has a balance sheet can effectively facilitate lending, as we can see by large tech companies such as Uber, Amazon, Google and many others recently making moves to begin offering financial services. Within the crypto space, upstarts such as CREAM have achieved traction by adding taking on more risk while larger projects such as Yearn and others have also made moves to enter the lending space with a “stablecredit” solution.

While large lending pools such as Aave command some network effects in terms of the superior interest rates they can offer, their current design with a single, undifferentiated capital pool also comes with drawbacks:

-

Capital inefficient by bundling different risks together and offering a blended return, appealing to a narrower capital base

-

Hampers innovation by increasing the potential costs of failed experiments as these can cause contagion and systemic risk.

-

Act as a target for nimble competitors who can either introduce incentives to facilitate vampire attacks and/or take more risks in moving quicker to add new, riskier products

Our goal with this proposal is to continue moving Aave towards being a credit protocol rather than a credit facility. We want Aave to be the go-to platform for launching, growing and managing money markets, taking advantage of Aave’s existing community, liquidity, and scale.

In this way, our goal is to create incentives that enable permissionless innovation to happen on Aave rather than via forks or competitors. With this, we also want to ensure the potential risks from this innovation are siloed off from the rest of the protocol to prevent contagion and systemic risk while allowing innovators greater ownership and potential upside.

Thus, innovators and their early backers are able to reap the majority of the rewards from their innovations, but they must also ultimately bear the risk of its failure. This should also lead to more efficient allocation of capital as Aave holders can select from a broader base of yield opportunities within the ecosystem depending on their particular risk appetites.

At the same time, we must balance this with ensuring these innovators both benefit from and contribute to Aave’s network effects and scale. Crucially, the system must be designed such that innovators cannot exploit Aave by leveraging it initially and later forking away from it, as this would be detrimental to the broader ecosystem.

Most importantly, this design should lead to a better product for users, as Aave is able to add new products faster while keeping the UX simple and ensuring the risks introduced by these new products are insured by those capturing the upside. This effectively enables Aave to leverage its existing liquidity to offer a bundled insurance and credit platform for users; a value proposition that few competitors can match.

Methodology

This proposal will focus on outlining the high-level token architecture and principles we propose could be used to achieve the previously mentioned goals of enabling permissionless innovation, siloed risk and network effects for Aave as an insured credit protocol.

We have purposefully omitted specifics around lower-level details and system parameters in an effort to ensure that initial discussions remain focussed on overall architecture rather than precise numbers. While a model is included, this should be seen as a way to help illustrate the concepts discussed rather than representing anything final or definite.

Provided the community likes the general direction of our proposal and we can come to agreement on the principles of the broader architecture, the Delphi team will set to work on fleshing out some of the important lower-level details. As a next step, we will construct a full model to allow for simulation of different scenarios, releasing this to the community for feedback. Provided this is agreed, the final step is to work on an implementation plan outlining the best way to initially launch this new system.

System Specification

High-Level Description

At a high-level, we eliminate the idea of a system-wide safety pool and replace it with sharded safety pools in the form of aDAOs that underwrite specific, pre-defined risks. Rather than Aave being one set of money markets governed by all Aave holders, Aave becomes an ecosystem with many different sets of money markets being governed by groups of incentivised $AAVE holders.

For comparison, this is a diagram of how Aave currently works:

This is a diagram of our new proposed system:

As we can see, rather than a single pool of Aave holders governing all Aave markets and a single safety pool backstopping all Aave markets as in the first diagram, we now have segregated capital pools (represented by “aDAO 1” and “aDAO 2”) governing and backstopping the risk for their own money markets (represented by “aDAO 1 Money Markets” and “aDAO 2 Money Markets”).

Similarly, rather than fees being paid to all Aave holders, each aDAO earns its own fees based on the performance of the money markets it operates. aDAO token holders (i.e. Aave holders who stake to a specific aDAO) are entitled to 80% of the fees generated by that aDAO. Aave holders who stake to the ecosystem reserve receive 20% of the fees earned by each aDAO as payment for providing the infrastructure, governing the system, and bootstrapping initial liquidity.

Note: These are preliminary numbers included for illustrative purposes and liable to change based on feedback and/or further research. It is even possible that rather than a fee share, Aave instead captures value via $aDAO token ownership instead.

Crucially, while the aDAOs govern and backstop risk for their own money-markets, the user interacts with the Aave front-end and smart contracts. Thus, although aDAO holders have certain predefined rights and obligations towards the money markets they govern, Aave itself controls the smart contracts and consequently the user relationship and deposits.

Overview

Lenders and borrowers have access to a wide range of products on Aave. In the background, these products are operated by different aDAOs which are themselves governed and backstopped by subsets of incentivised Aave holders. Aave holders can therefore deploy capital to a variety of opportunities within the Aave ecosystem, making decisions based on their specific risk-reward profiles. To realize this goal, we propose the following structure:

-

$AAVE holders can either:

-

Stake $AAVE into the ecosystem reserve, receiving $stkAAVE entitling them to govern the reserve and earn fees generated by it

-

Stake $AAVE into one or many aDAOs, receiving $aDAO tokens

-

If an $AAVE holder stakes $AAVE into aDAO1 he or she is locked up for a period of time and receives $aDAO1 tokens issued on a bonding curve with $AAVE as the reserve asset. Use of the bonding curve has many benefits, including liquidity and encouraging efficient pricing of aDAO risk

-

The exchange rate of $AAVE to $aDAO tokens depends on the bonding curve of that aDAO

-

The $aDAO1 holder now has governance power within aDAO1, including:

-

Determining key parameters described later on in this document

-

Determining how to allocate the $AAVE in their capital pool, including the safety pool (which must be put into safe investments such as Balancer pools) as well as $AAVE in the treasury

-

The $AAVE in an aDAO’s safety pool will be auctioned off to make depositors whole in the event of undercollateralized or delinquent loans. This is described in more detail later on in the document

-

$aDAO1 tokens can also be staked on other platforms, but while the $aDAO1 tokens are staked the holder cannot engage in governance

-

The $AAVE tokens are a backstop to the tokens that are lent within the aDAO (the tokens available on each aDAO are determined by the aDAO (ex. ETH, USDC, DAI etc.)

-

$AAVE is the reserve token for the Aave ecosystem, backing up all $aDAO tokens. In addition, it has ultimate governance rights over all aDAOs and over the ecosystem reserve, which will itself include $aDAO tokens

Ecosystem Stakeholders

The Ecosystem Stakeholders are the following:

● $stkAAVE Holder: Stakes their $AAVE, receiving $stkAAVE entitling holder to govern the ecosystem reserve, which receives 20% of the collective aDAO earnings and may own assets such as $aDAO tokens.

● $aDAO1 Holder: Earns 80% of the lending origination fees from aDAO1 as well as benefiting from potential price appreciation in $aDAO1. Backstops risk in aDAO 1

● $aDAO2 Holder: Earns 80% of the lending origination fees from aDAO2 as well as benefiting from potential price appreciation in $aDAO2. Backstops risk in aDAO 2

● aDAO1 lender: Lends from money-markets governed and backstopped aDAO1

● aDAO1 borrower: Borrows from money-markets governed and backstopped by aDAO1

● a aDAO2 lender: Lends from money-markets governed and backstopped by aDAO2

● aDAO2 borrower: Borrows from money-markets governed and backstopped by aDAO2

Benefits

This design has several benefits:

-

Capital Efficiency: Tranching risk increases capital efficiency, allowing $AAVE holders to have access to different yield opportunities based on their risk-reward profiles. Holders who want the least risk can stake to the ecosystem reserve which doesn’t backstop any risk, users who want low risk can stake to one of the aDAOs that underwrites high-quality assets such as stablecoins/BTC/ETH, and users who want higher risk can take idiosyncratic risk on more speculative or higher risk aDAOs.

-

Faster Innovation: This design enables Aave to move even faster than it already does. Rather than the global safety pool in which any new product introduces the potential of contagion and systemic risk, the tranched model ensures risks are siloed and contained among those who are both willing to bear them and appropriately rewarded for doing so. This means Aave can launch higher-risk, more experimental products while providing higher safety assurances to users and eliminating systemic risk.

-

Better Products: This results in a better product for users who not only have access to a broader variety of products but also have the comfort of bundled in insurance via the bonding curve capital pool. This capitalizes on Aave’s liquidity and security network effects, making it very difficult for smaller competitors to be able to match Aave’s product offering.

-

Open Platform: The ability for anyone to create aDAOs that manage money markets transforms Aave from a credit facility managed by a central entity to a credit platform/protocol in which anyone can permissionlessly spin up money markets. Would-be competitors who see a product gap in the market are encouraged to create aDAOs rather than compete directly, taking advantage of Aave’s existing liquidity and customer base to enable a better product and faster route to market.

Forming an aDAO

In order to form a aDAO, an Aave staker submits an Aave Improvement Proposal (AIP) which specifies the aDAO’s charter and key system parameters. We outline a full list of potential parameters along with descriptions of each one in our longer form proposal linked above.

After formation, any changes to the aDAO parameters are determined by $aDAO holders with the result being submitted to Aave for execution. Any change to a fundamental system parameter means those on the winning side are locked for a predefined time period while losers can exit the system.

Rather than voting for/against it, the AIP must instead attract a minimum quorum of Aave staked to it (e.g. 5%). Upon reaching this minimum quorum, the aDAO is automatically created, with staked Aave being converted into aDAO tokens on the proposed bonding curve and locked for some period of time (e.g. 3 months). Initially, we would recommend AAVE either set an extremely high quorum for creating new aDAOs, operate all new aDAOs itself, or at least retain some level of veto power in order to ensure the quality and legitimacy of aDAOs being created.

aDAO Bonding Curve, Treasury and Balance Sheet

Bonding Curve Design

We suggest $aDAO tokens are issued on a bonding curve with $AAVE as the reserve asset. For simplicity, we’ve assumed a linear bonding curve shape and that all aDAOs utilise the same bonding curve shape.

We recognize that a linear bonding curve is not the optimal design for various reasons. Determining the optimal bonding curve shape is beyond the scope of this paper and will be part of the workstream in phase 2 once the architecture has been agreed upon.

Capital Pool as Insurance

Similarly to Nexus Mutual, the capital in the bonding curve acts as the safety pool that insures aDAO’s money markets against both smart contract and economic risk. In case of delinquent loans or hack, $AAVE in the bonding curve is sold to make depositors whole, reducing $aDAO’s token price. This means Aave can now offer a bundled insurance & credit product to users, increasing its value and fee extraction potential.

The treasury is a separate pool of discretionary capital that $aDAO holders have governance rights over. This capital is not in the safety pool or bonding curve and can be used by the aDAO for ecosystem incentives, yield-generating activities, paid out to $aDAO holders or anything else as determined by governors.

The minimum safety parameter (which is also set by the aDAO governors) determines the mandatory ratio of capital in the bonding curve to system capacity. As the aDAO grows and $aDAO token supply expands, overall system capacity grows alongside it as there is more $AAVE backing the curve. This means, provided the risk is appropriately computed and reflected in the MSP, users will always have access to insured money markets as $aDAO supply should grow alongside system capacity. For $aDAO holders, this also means not all capital in the Bonding Curve will be liquid/withdrawable at a given moment in time since part of it will be a liability in the form of money market insurance for depositors. However, $aDAO holders always have a claim to the $AAVE in the safety pool. If they want to redeem, they will ultimately have to wind down the money markets in order to eliminate the insurance liability.

aDAO Balance sheet - Treasury and Capital Pool

In addition to capital in the bonding curve / safety pool, aDAOs may also build up treasuries which are governed by $aDAO holders. There are multiple ways to for an aDAO to build up a treasury:

-

Divert a percentage of $aDAO token purchases to the treasury

-

Divert a percentage of fees generated to the treasury

-

Charge a withdrawal fee for bonding curve withdrawals and divert a percentage of this fee to the treasury

-

Implement a low maximum safety parameter, meaning capital flowing into the bonding curve gets diverted to the treasury early on

-

Receive a grant from the Aave ecosystem reserve

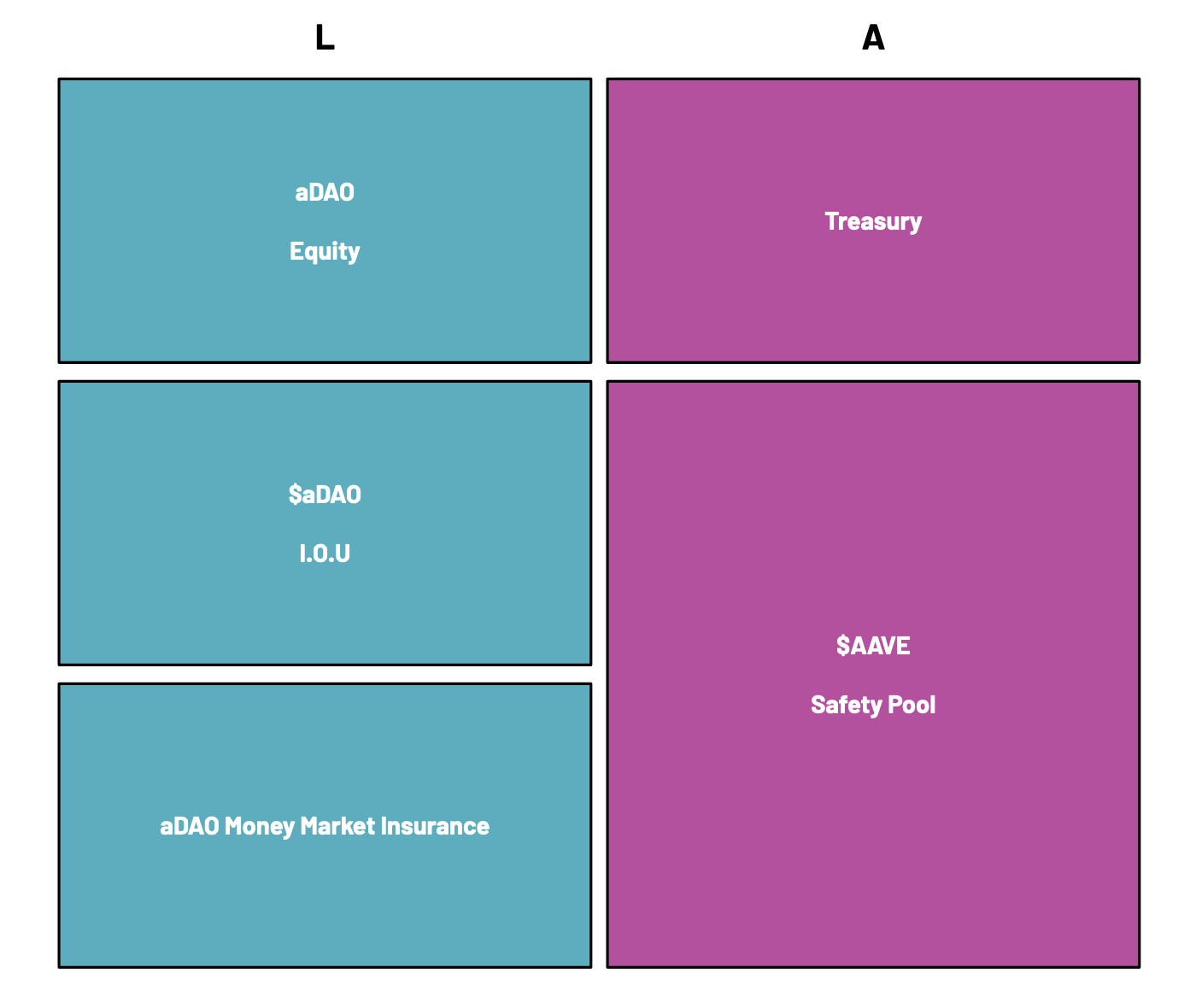

The aDAO balance sheet can thus be seen as follows:

An aDAO token’s book value is the excess capital in the safety pool above and beyond the amount necessary to satisfy the insurance liability (determined by System Capacity * MSP) plus the amount in the treasury.

As such, the bonding curve price can be rightly seen as the $aDAO’s token’s price floor, with the market price most likely trading above this. This is because the bonding curve price doesn’t take into account the additional $AAVE in treasury which $aDAO holders have rights to (aDAO equity in the balance sheet above).

Ecosystem Reserve and aDAOs

Governance

Ecosystem Governance

At a high-level, $AAVE holders who stake to the ecosystem reserve receive $stkAAVE which entitles them to govern the reserve and receive some yield from that. This should require a lock-up period and be the lowest yield available in the Aave ecosystem since $stkAAVE holders are not backstopping any risk. As mentioned previously, the ecosystem reserve should primarily be used to bootstrap the Aave ecosystem by investing and providing grants to aDAOs, although working capital can also be invested as determined by the governors.

In case of a hack, $stkAAVE holders may choose to use the ecosystem reserve to make depositors in an aDAO or aDAO holders themselves whole. However, it is not obliged to do so as each DAO is fully self-sovereign and liable for its own risks.

aDAO Governance

aDAOs are self-sovereign entities governed by $aDAO holders with a one-token-one-vote system. In order to govern the aDAO, only $aDAO tokens held for at least 7 days are able to vote on any proposal. We propose that voting power scales logarithmically with time tokens are locked for, rewarding longer-term holders with more governance power without leading to excessive concentration. To supplement this, we suggest a reputation system which is specified in more detail in our longer-form proposal.

We propose that any vote that alters a fundamental system parameter (i.e. one of the charter parameters outlined in the “Forming an aDAO" section) locks the winning side’s tokens for an additional 7 days after the vote finishes, with the losing side being unlocked immediately. This ensures that users are able to exit the system if the aDAO no longer operates by the charter they agreed to, with those proposing the change living with the consequences of their decisions.

While the aDAO is self-sovereign, it does not itself control the smart contracts of its money-market. Instead, any decision made by the aDAO is sent to the Aave DAO to ratify and execute. This ensures TVL always sits with Aave, maximising the ecosystem-wide network effects.

AAVE and aDAO Interactions

As a metaphor, the Aave ecosystem reserve can be seen as the holding company while aDAOs are the partially owned subsidiaries. The ecosystem reserve will hold $AAVE tokens and may also hold several $aDAO tokens. In addition, it receives cashflows from all underlying aDAOs, with $stkAAVE holders being in charge of allocating these cashflows to wherever they can achieve the highest returns.

The ecosystem reserve can interact with the aDAOs in a variety of other ways. These are specified in more depth in the “AAVE and aDAO Interactions” and “Ecosystem reserve and aDAO” sections of our longer form proposal.

Protecting from tail risk

While the system works well under normal circumstances, given that all aDAO safety pools/bonding curves are held in $AAVE, a sharp fall in $AAVE price could lead aDAOs to trade under the minimum safety parameter. While this isn’t ideal, it isn’t as bad as it sounds since unlike something like THORChain, there is no immediate way for this to be exploited by bad actors. Rather, it simply means the aDAO is not appropriately collateralised for the technical and market risks it is exposed to.

It’s also worth understanding that there are natural market forces that should help collateralise the safety pool. Assuming the price of $aDAO tokens have intrinsic value based on the discount future value of cashflows they generate and distinct from the $AAVE price, then as $AAVE drops in price, users are able to acquire the same amount of $aDAO tokens at a lower dollar price. This should encourage more $AAVE to flow into the safety pool to take advantage of this.

Nevertheless, crypto markets are rarely efficient and we thus propose a few additional layers of protection for the system:

-

aDAO Treasury: The first layer of defense for an aDAO is its treasury. We propose that if the amount of value in the safety pool drops below the minimum safety parameter, the treasury is automatically transferred into the bonding curve/safety pool.

-

Incentive pendulum: If after transferring the treasury into the safety pool, it still remains undercollateralized, then we propose the following incentive mechanisms:

-

Increase Staking Incentives: $aDAO pools issue $aDAO credit tokens, entitling users who come in to stake while the pool is undercollateralized to receive a larger amount of future $aDAO tokens

-

Reduce System Capacity: If neither solutions work, then we suggest creating incentives to reduce system capacity, perhaps by implementing an increased fee on outstanding loans to incentivize users to pay their loans back.

Implementation

Types of aDAOs

At a high-level, we believe aDAOs should be segregated by their risk-reward profile, perhaps based on Aave’s existing asset risk framework. This allows each DAO to be owned and operated by stakeholders with appropriate risk appetites. In addition to tranching risk, Aave can also use new aDAOs to enable risk siloed experimentation hubs such as the recently proposed DAO to DAO lending.

We suggest, at least initially, each aDAO should have an exclusive license over assets deposited into its protocol as well as the type of lending products it provides. Eventually, we believe it should be possible to open this up, allowing aDAOs to offer similar assets, competing on the way the particular combinations of assets they provide, the speed/quality of governance and/or the risk-reward provided.

Initial aDAOs

Initially, we propose all initial aDAOs will be operated by Aave itself, with the current money markets protocol being split into either one or multiple aDAOs, pending feedback from the community:

-

Single aDAO

-

“Aave Classic”: includes all existing money markets

-

Two aDAOs

-

Aave AA: includes the highest quality collateral ($BTC, $ETH, stablecoins), having a lower safety parameter and consequently lower yield

-

Aave AB: includes lower quality collateral ($YFI, $BAT, $ENJ, $REN, $KYBER, $LINK, $MANA, $MKR, $REP, $SNX, $WBTC, $ZRX)

-

Three aDAOs:

-

Aave asset-backed: includes asset-backed tokens such as stablecoins, WBTC and potentially others such as PAXG.

-

Aave AA: includes the highest quality collateral ($BTC, $ETH, $LEND)

-

Aave AB: including lower quality collateral ($YFI, $BAT, $ENJ, $REN, $KYBER, $LINK, $MANA, $MKR, $REP, $SNX, $WBTC, $ZRX)

Initial $aDAO Distribution

The initial aDAOs will likely be comprised of Aave’s existing money-markets. As such, the initial $aDAO token launch will have to use some fair distribution mechanism to avoid users rushing to frontrun the aDAO bonding curve on launch. We have some ideas around how to do this that we will flesh out at a later stage.

Potential aDAOs

In terms of new aDAOs, there are many potential ideas here. Broadly, the goal should be either to either group together assets with similar risk-reward profiles or allow for experimentation with new kinds of products.

In addition to the aDAOs already mentioned above, these are some other potential ideas for aDAOs:

Risk-tranched

-

Aave asset-backed: Money markets for asset-backed tokens such as stablecoins, $PAXG, $WBTC, $REALT tokens, etc. In addition to traditional risk parameters such as liquidity, volatility, etc, risk framework should include custody risk, technical risk, and others.

-

Aave yTokens: Money markets for yield-bearing tokens including $YUSD, $YETH, $crUSD, $pUNIUSDC, etc

-

Aave BBB: CREAM competitor operating money markets for the long-tail of more illiquid, volatile tokens such as $UNI, $wNXM, etc.

Experiments

-

Aave uncollateralised: Money markets for uncollateralised stablecoin lending. This could have more stringent KYC requirements, operate using open law agreements and/or experiment with on-chain credit history, reputation or prediction markets.

-

Aave DAO2DAO: Money markets for DAO to DAO lending. This could be bootstrapped by Aragon and leading Aragon DAOs.

Risk Framework

Given the fact that aDAOs will be segmented primarily by the risk-reward they provide, combined with the importance of setting an accurate safety parameter for each aDAO to ensure system integrity, it’s extremely important to have robust risk frameworks to assess the risk being taken on by each aDAO.

These can be based on the existing Aave risk asset framework, but we also recommend this is supplemented with specific frameworks for different kinds of assets such as asset-backed tokens which may require bespoke analysis around things like custody risk. We also recommend standards are created to classify the riskiness of different assets in order to be able to accurately group them into the correct risk bucket and corresponding aDAO, as well as to be able to estimate what an appropriate safety parameter looks like.

The goal should be to first settle on a metric that accurately reflects system capacity, i.e. the risk weighted credit exposure that a certain aDAO is taking on. Then, each aDAO will define its safety parameter in relation to that metric, based on its charter and targeted risk-reward ratio.

User Experience

While the aDAO system may seem complex, we believe the majority of this complexity can be abstracted away from users. Provided all aDAOs are appropriately collateralised (which should be guaranteed by the governance process), users don’t care how the money markets are secured and governed, they just care about the variety, quality, and safety of the products they use.

As such, we propose all aDAO money market smart contracts are owned and operated by Aave and displayed on the app.aave.com website, similarly to how any new market would be displayed. Users interact with the money markets as normal and need not be aware of what aDAO is governing those particular markets.

Proposed Roadmap

We propose the following phased roadmap:

-

Phase 1 - System Architecture

-

Discuss the high-level system architecture presented in this document

-

Implement any changes presented by the community

-

Phase 2 - Specification

-

Determine lower-lever system specifications with goal of arriving at a minimum viable design: the simplest design that allows for the system to launch and begin testing assumptions in production. This will include:

-

Bonding curve shape - Model out different bonding curve shapes based on existing Aave data

-

aDAO Risk Framework - Determine the best way to calculate “system capacity” and MSP across the ecosystem

-

aDAO parameters - Model out different withdrawal fees, treasury parameters, etc to figure out optimal initial aDAO design

-

Phase 3 - Implementation

-

Determine the best way to implement the system, including:

-

Which aDAOs to launch first

-

How to conduct $aDAO initial distribution

-

Potential aDAOs to launch later

-

Phase 4 - Additional workstreams

-

Reputation - Design reputation system to be used across Aave ecosystem

-

Ongoing monitoring - Ongoing monitoring of aDAO system health, including determining what metrics to track, etc.

.) Maybe a couple of videos – 1x high-level, 1x detailed – and jumping on the Delphi podcast would help?

.) Maybe a couple of videos – 1x high-level, 1x detailed – and jumping on the Delphi podcast would help?