TLDR

-

Blockworks is supportive of the the proposal as-is but believes some additional information on forward-looking projections could benefit AAVE DAO and prospective AAVE tokenholders

-

Aave is a growing onchain-native business and a nascent fintech platform. We believe that this strategic investment is likely to generate long term value, with a market expansion beyond crypto natives.

-

While the funding amount requested might seem large, is effectively low compared to fintech peers, and the treasury can absorb it without creating undue insolvency risk.

-

In light of this welcomed growth focus, we recommend reviewing some strategies, such as buybacks, to preserve additional runway and diversify the treasury.

Blockworks is generally supportive of the direction of the proposal. In our view it functions as a credible reset from the perceived Labs/DAO misalignment that’s weighed on sentiment and, more importantly, it lays down the foundations for AAVE to exit the “crypto” cohort and enter the fintech classification. Some of the specific numbers/mechanics may need rework, but the strategic intent is right.

We also understand the desire to split items into separate votes, but we think unbundling could be counterproductive. Crypto is increasingly competing with more attractive verticals (notably AI) for talent, capital, and allocator attention. In that environment, we think Aave needs a coherent barbell strategy:

-

Institutionalize the ecosystem, and

-

Push into consumer-facing distribution to sustain growth.

Fragmenting the package increases the risk of ending up with partial measures that don’t reach a strong end-state. We see Aave Card and the Aave App as major potential drivers of the consumer push, real “DeFi to daily utility”, and democratizing financial services for the masses. The vertical integration with the lending platform is a meaningful moat worth leveraging. The risk of unbundling is adding friction (governance/process) that slows shipping while competitors integrate similar rails and win via faster iteration and stronger distribution. Aave Kit and Aave Pro can multiply Aave’s core strengths by enabling third parties to build neo-bank style experiences on top of Aave rails, giving ability to scale distribution without the DAO needing to operate everything directly.

More than anything, we think better alignment between Labs and the DAO makes AAVE more appealing for investors, and for this reason a light Foundation managing IP rights is also a welcome initiative. But alignment alone won’t be enough in a world where allocators are more selective, and, over time, Aave likely needs stronger investor communication, clearer long-term positioning, and more deliberate institutional relationship-building. Still, this alignment is a foundational prerequisite, needed for what is next.

Crypto’s future looks structurally different from its past. Strategies that worked in prior cycles won’t drive the same success going forward given macro shifts, competition for mindshare, and changes in how capital allocates risk. Thinking of Aave as the DeFi protocol it has been so far is a severe mistake, and is worth instead analysing what grows means for a Unicorn fintech spun from crypto rails instead. We can in this sense analyse the numbers provided.

Aave is a growing onchain-native business and a nascent fintech platform.

Aave is entering a new phase of growth, going after a new class of users (fintech retail with Aave app and card, institutions with Aave Pro). While the lending infrastructure is extremely valuable and expanding with v4, the additional distribution of these apps would directly benefit the protocol and the revenues. The TAM of the traditional financial services market justifies the shift and the related investment.

In our opinion, while some more details are needed, the grant ask is proportionate to the goal and market benchmarks for crypto and traditional companies. Acquisition costs are the larger line item for growth-stage fintech companies:

-

Fintech B2C customer acquisition costs (CAC) are among the highest across industries, with 2025 benchmarks averaging roughly $1,450 for specialized Fintech/SaaS, while broader B2C apps often range between $70–$130

-

B2B and institutional acquisitions costs is even higher

By other market sources (like multiples.vc) we can estimate the global costs:

-

Ramp (pre-profit): $60M–$100M annual burn

-

Brex (growth phase): $80M+ annual opex

-

Revolut (pre-profit years): $100M+ annual operating costs

On the other hand, The current expenses for the DAO (e.g. the protocol) are in line with the market benchmarks.

| Column 1 | Column 2 | Column 3 | Column 4 |

|---|---|---|---|

| Lido (2026) | Uniswap (2026) | MakerDAO/Sky (2025 Est.) | |

| Annual Funding Ask | ~$60M for 2026 | ~\$70M Uni | ~$100M (including subdaos) |

| Primary Scope | Core Dev, Node Ops, Safety | Core Dev (V4), App, Card, RWA | Stablecoin, SubDAOs |

We also want to address the comments regarding treasury sustainability by first quickly checking revenue potential, and then quoting costs incurred by the DAO and the composition of assets held.

Regarding revenue, Aave made over $100M in 2025, mostly in reserve factor fees, and is off to a strong start in 2026 with annualized revenues of $120M, despite the broad market downturn. However, we estimate that, due to the general growth of the lending market and Aave v4 unlocking new revenue streams, we could end the year closer to $150M.

On the cost side, according to tokenLogic, current annualized costs are $141M. After this proposal, they should increase to around $190M, generating a potential shortfall between $40M and $60M that would have to be absorbed by the treasury.

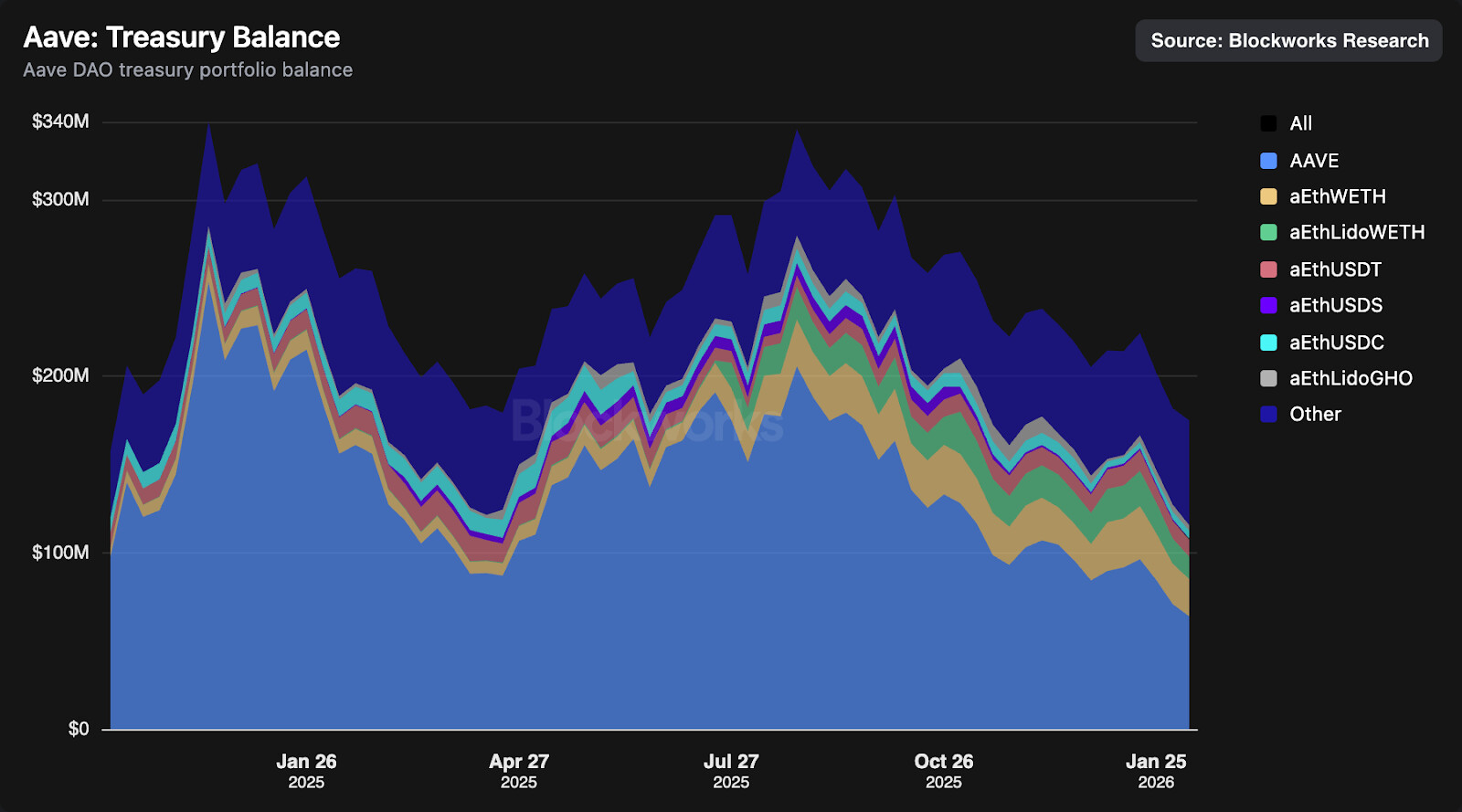

Finally, the treasury has a total value of $165M, of which $50M is in stablecoins. The total ask of roughly $50.7M is 30.7% of the entire treasury.

Taking into account the revenue flow we have today, the treasury is capable, in the near term, of absorbing these costs, leaving around 3–4 years of runway. Conservatively, we are not assuming additional revenues from new product lines. The implied burn multiple (cost / revenue) would be around 1.2–1.3, which is standard for companies over the $100M revenue mark that are still in growth mode.

One more critical thing is the consequent increased treasury concentration, as the stablecoin ask alone is 42% of the DAO’s non-AAVE reserves. While this is tangential to the current topic, it is worth at least trying to properly frame the costs incurred by the DAO so far in the context of a future that puts Aave into the fintech category and not in DeFi.

The Aave DAO spent about $35M on buybacks in 2025; due to the market downturn, the current value of the almost 160,000 AAVE tokens bought back is around $17M, showing a net loss of $18M so far, an amount that is 35% of the requested budget by the lab. As already mentioned in the past in our aavenomics post, Blockworks is generally against the buybacks at this stage in Aave’s growth journey, and especially mechanically executed ones that don’t have a strategic plan and strong KPIs behind them. We believe that buybacks are not a good investment for protocols in the growth stage; given the increased revenue alignment and the graduation of Aave into the fintech category (which bears further growth multiples ahead) we believe that potentially revising this plan could help soften the impact of this proposal without touching any DAO or service provider costs. Moreover, reducing buybacks would improve treasury diversification.

We do think there is margin to improve the proposal to better set expectations for the future. We would like Aave Labs to probably outline, in greater detail, what the next few years after the approval of this proposal would look like in terms of revenue projections to better contextualise what we see not as a cost, but as an investment from the DAO.

Recommendations

While supportive of the proposal as-is, we think that a multi-year plan that clearly outlines future revenue projections, associated costs, and the ultimate financial and strategic targets that will serve as the justification for this significant investment would benefit not only current AAVE tokenholders, but prospective AAVE tokenholders that want to better understand the business forward-looking .

Even if the proposal does not jeopardize treasury, we recommend reviewing the buyback strategy in light of the increased alignment between labs, DAO and tokenholders and increased funding needs. We don’t see runway as a potential concern, but increased treasury concentration in volatile tokens requires mitigation measures.