First, we’d like to say thank you to everyone who has provided feedback on the Aave Will Win Framework proposal. The Temp Check process is designed to gather this kind of input so we can refine the proposal before moving to a formal ARFC vote after the Temp Check. In this post we’ll address the main, recurring questions raised in the thread so far.

Note: We will continue to gather feedback and follow up with responses throughout this process.

What is the difference between the Primary Grant and the Growth/Development Grants?

The Primary Grant of $25 million in stablecoins is to fund the ongoing cost of operating, maintaining, and advancing the Aave protocol, while also enabling continued innovation at the product layer. This includes ongoing protocol development and maintenance, research into future protocol versions, application security, ecosystem and integration support, governance implementation, legal and compliance coordination, operational infrastructure, and the other core functions required to ensure the protocol remains secure, competitive, and resilient.

Importantly, V4 introduces greater flexibility at the protocol level, enabling more opinionated product decisions to be embedded directly within the architecture. This represents a meaningful evolution in how Aave can compete, differentiate and monetise. However, that flexibility also increases the scope of ongoing work. Designing, implementing, managing, and iterating on these product-level decisions within the protocol requires sustained technical, operational, and strategic resources over time.

In addition, it’s important to build infrastructure and tooling around V4. Responsibility for building and maintaining that infrastructure would also need to be covered within this scope.

These costs are not dependent on the launch of any single new product. They represent the continuous effort required to run the protocol responsibly, expand its capabilities, and execute effectively at the product layer.

The 75,000 AAVE is separate from the operational budget. It is exclusively for employee alignment and retention. Hiring the best talent the industry has to offer requires compensation packages that compete with fintech, CeFi, and pre-TGE token offers. These tokens are structured with long-term vesting schedules, which is standard practice for long-term employee retention. Most importantly, under this framework any talent hired by Labs is working for the Aave Protocol and completely aligned towards growing it.

The Growth/Development Grants, totaling $17.5 million, are launch-based payments tied to specific new products. Each new product launch expands operational costs and requires additional spend, particularly during the go-to-market period. These products are competing in highly competitive verticals where user acquisition, marketing, distribution partnerships, and ongoing development and improvements are expensive. The grants cover these costs.

They are structured as separate payments, with six month streaming because they are contingent on delivery. If a product does not launch, the grant is not paid. Given they are streamed, the DAO also has oversight on these grants and can decide whether they are being used effectively.

We’d also like to note that the $10-30 million in annualized revenue from the CoW Swap integration is a day-one contribution from a single product. We will be adding more features here to drive more volume and fees with the release of Aave Pro interface including automated leverage, trigger and limit orders, and more. The proposal also directs 100% of the revenue from several additional product lines.

Why does the proposal request AAVE tokens, and what are the selling restrictions?

As mentioned above, the 75,000 AAVE tokens are for employee alignment and retention. Aave Labs competes for talent against fintechs, CeFi companies, and pre-TGE startups that all offer equity or token-based incentives. To hire and retain the best people in the industry, Aave Labs needs to offer compensation packages on par with these competitors.

The token grants are structured with long-term vesting schedules to support retention and long-term alignment. This means the tokens are distributed to team members gradually over time and are not intended to fund operational expenses. The two-year linear unlock at the DAO level flows into these longer-term individual vesting schedules, reinforcing long-term alignment and reducing short-term sell pressure.

Regarding governance, Aave Labs will not use any AAVE tokens received as part of this funding package to vote in Aave governance. The only time these would ever be eligible for governance use is when they are no longer in Aave Labs’ custody, which can be easily monitored by the DAO.

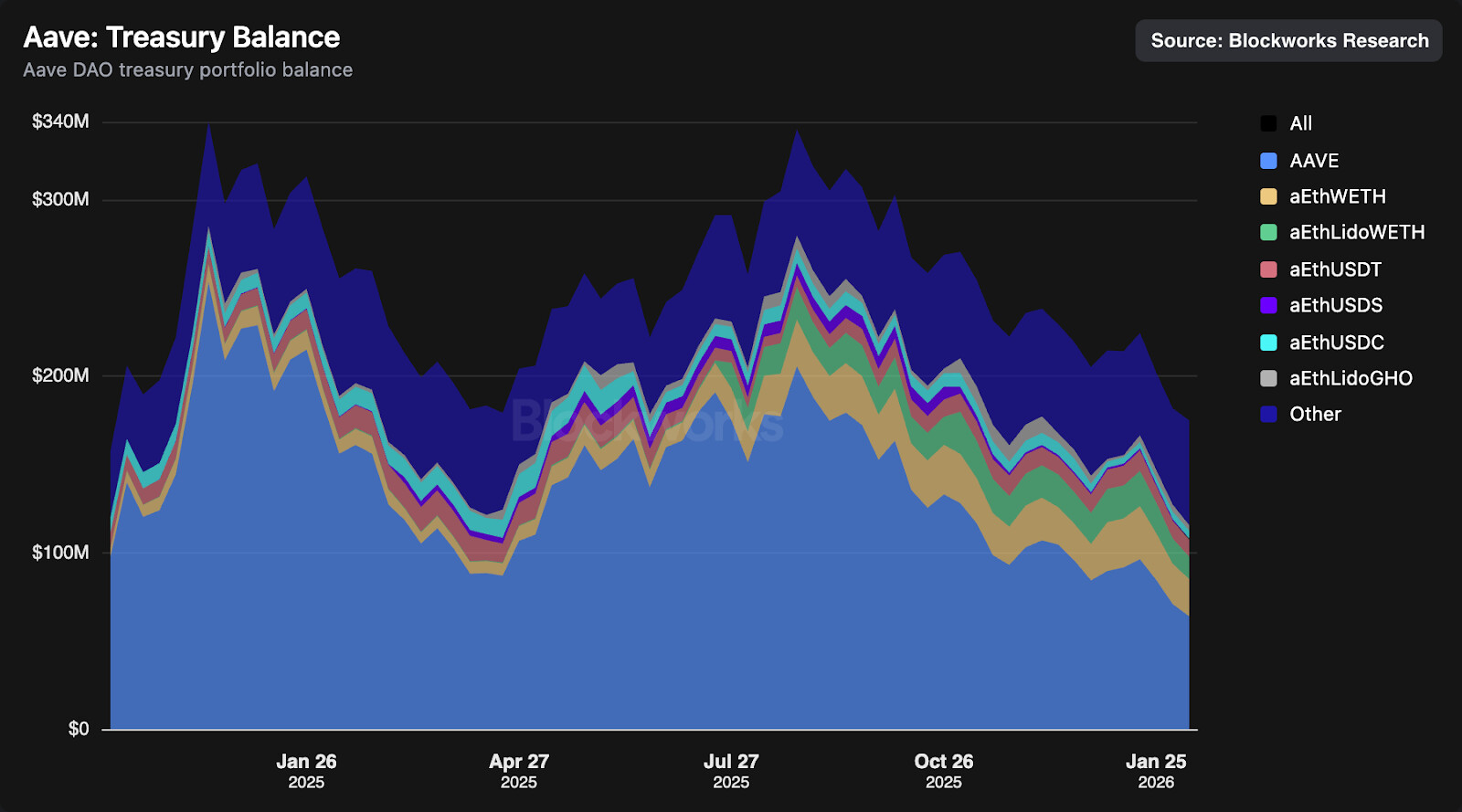

Is this budget justified? Why is it substantial?

While building in DeFi does have structural cost advantages, going after the mass market and competing for consumer and enterprise attention is a different game entirely, and the costs there are similar regardless of the underlying rails. User acquisition, marketing, partnerships, and distribution are expensive at consumer scale. Major fintechs spend hundreds of millions of dollars a year on sales and marketing alone. The benefit of this, however, is that they also make billions of dollars per year from this spend. Many fintechs have multiple revenue streams that bring in $100M+ per year.

The reason this matters now is that DeFi’s TVL peaked in 2025 at roughly the same level it reached in 2021, around $205 to $225 billion. New capital is not flowing into DeFi in large amounts. Aave captured a bigger share of the overall market during that period, but the market itself has not grown meaningfully. Without a strategy to bring new users, new collateral types, and new revenue sources onchain, the protocol risks stagnating as does the DAO’s revenue. This budget would aim to fund that strategy.

Can you provide more transparency on Aave Labs’ internal structure and cost allocation?

Aave Labs currently has 90 staff members, all focusing their efforts on Aave. The team is organized across several functions, with the majority focused on engineering and product development. A high-level breakdown of spend covers protocol and product engineering, go-to-market and growth, business development, legal and compliance, application security, and operations.

100% of the $25m budget funding will be used for product development, growth and support for Aave. To deliver the product launches and growth strategy, we estimate the $25m is split across the following:

-

Production and Protocol Development: ~65%

-

GTM, Marketing, and Business Development/Engineering: ~10% + Growth/Development Grant budgets

-

Security and Legal: ~15%

-

Operations: ~10%

Additionally, Aave Labs will not be working on any non-Aave revenue streams in line with the token-centric model.

We’d like to also note that Stani takes only a minimum wage salary as the legal requirement, and does not receive AAVE tokens.

Why are the Growth/Development Grant amounts similar for different products

The grant amounts for Aave App ($5M), Aave Pro ($5M), Aave Card ($5M), and Aave Kit ($2.5M) are based on their estimated go-to-market costs. When compared to the request to build Aave V4, or other protocols, it’s important to note that the DAO typically takes on the cost of the protocol’s go-to-market expenses as well. So these aren’t just the cost to build each product.

Launching consumer-facing products like the Aave App, Aave Card, and Aave Pro requires significant investment in user acquisition, marketing, and distribution partnerships. Aave Kit has a more targeted go-to-market (e.g. fintechs and institutions) and maintenance strategy and therefore a lower grant amount.

These are good-faith estimates and on the low end of what we believe will be effective. The use of these funds will be detailed in our quarterly reports to the DAO, which will include key performance indicators for each product. As streamed amounts, these totals would also come with DAO oversight. We will also include a commitment that any funds that are not spent will roll forward and be considered part of any future funding requests.

Why do the Growth/Development Grants cost more than V4 development?

The V4 budget of $12 million covers building the protocol itself. It does not include funding for ongoing growth, maintenance, or continued improvements to V4 after launch. For context, the DAO has historically funded V3 growth separately through incentive programs and partnerships, and may choose to do the same for V4.

Building a production-ready protocol and bringing consumer products to market are different cost profiles. Protocol development is relatively low capex but also low margin, since protocol fees flow directly to the DAO. Consumer-facing products require higher upfront investment in go-to-market and user acquisition, but they also create higher margin revenue opportunities that would go to the DAO under this framework.

The Growth/Development Grants cover go-to-market across four net new product lines, including user acquisition, marketing, and ongoing security, development, and maintenance. These are the costs of competing in crowded verticals, and they typically exceed the engineering investment. The DAO has historically funded growth separately from development, and this proposal follows the same logic.

What are the revenue deductions and how would it be limited?

As we point out in the proposal, “Revenue is defined as gross product revenue earned by Aave Labs, minus any direct revenue sharing paid by Aave Labs to external partners including revenue rebates, revenue subsidies, revenue sharing arrangements and any additional direct user incentives.”

These funds are not for salaries or operational costs and will be used exclusively to grow the underlying product. We will disclose additional user incentives spending in our quarterly updates and are open to defining a maximum revenue incentive spending percentage in future product-specific proposals.

Some existing partnerships include revenue share arrangements between Aave and the respective counterparty. In certain cases, a percentage of fees is passed directly to the partner at the integration level, meaning that portion of revenue is never received and therefore cannot be passed through to the DAO. In other cases, partners may receive rebates to satisfy minimum revenue-share commitments, or a defined share of vault yield fees.

These arrangements reflect standard commercial structures designed to secure valuable integrations and distribution. They represent negotiated trade-offs based on the strategic and economic benefits the partnership brings to the protocol.

Similarly, products like the Aave App or Aave Card carry transaction processing costs that scale directly with user activity. If these products are successful, those costs could grow significantly over time, potentially exceeding the size of the grant request itself.

In a traditional business model, these variable costs are incorporated into the fees charged to users to ensure the product remains profitable on a marginal basis. If instead all gross revenue from these fees is routed directly to the DAO, Aave Labs would still have to pay the growing costs, which could become very expensive, very quickly if adoption is strong.

This also applies to user incentives, such as cashback offers on the Aave Card, which may be necessary to drive adoption and remain competitive. Without the flexibility to fund these incentives at the transaction level, we risk not having sufficient resources to meet those obligations if the product scales successfully.

In summary, these outflows are not regular operating costs but are externally revenue-related payments.

We are committed to transparency around these outflows and how they evolve over time. Revenue reporting, including these revenue outflows, will be reported on the DAO. Most of the revenue deductions can be tied to independently, public and verifiable metrics such as transaction volumes and TVL. We will also work with the DAO on a solution to have a third party independently verify this data. However, we need the flexibility to make product-level decisions on fees and incentives to ensure fast execution, sustainable unit economics, and the ability to responsibly scale successful products.

Why would we shut down V3 in favor of V4 and is the timeline reasonable?

V4 is a strict superset of V3. At launch, it will serve V3 users with higher capital efficiency and more advanced features.

V3 configurations can be replicated within V4 where needed, preserving existing market experiences, while V4 will expand into new, currently inaccessible areas to drive additional demand.

That said, there is zero rush. V3 is stable, battle-tested, and will continue to be actively maintained and serviced until users are comfortable migrating to V4 at their own pace. Some of that migration will happen naturally as new partnerships and integrations are built on top of V4. The timeline proposed in the framework is open to discussion, and we want to emphasize that the migration can be very slow and steady. A separate proposal will follow for V4 protocol activation, and that vote will focus on the readiness of the code and launch parameters.

For similar reasons stated above in other questions in this response, we do think it’s important that Aave embrace and pursue innovation, which historically the DAO also agreed with voting to fund V4. So that’s why we believe it’s important to ratify the strategic direction behind V4.