aip: TBA

title: Aave V2 - Liquidity Mining Program (90 days at 30% reduced rate)

status: Proposal

author: @MatthewGraham

created: 2021-10 25

Simple Summary

Liquidity mining incentives were introduced to Aave V2on the 26th April 2021 via AIP-16 and then voted to continue on the 24th August 2021 via AIP-32 for an additional 90 days. AIP-32 incentives are due to expire 22nd November 2021.

This ARC presents the community with the opportunity to continue offering stkAAVE incentives for an additional 90 days from when AIP-32 finishes, up to including the 20th February 2021. The incentives will be distributed at a 30% reduced rate, commencing the tapering of incentives on the Aave V2 market.

Stable coin / low vol assets receive lending and borrowing incentives, split 1:2, in favour of borrowers over lenders. Aave V2’s revenue is derived from interest paid by borrowers and borrowing demand drives lending yield through higher liquidity utilisation. High vol assets receive lending incentives, skewed towards assets more recently listed and communities that have static relationships with Aave, like Balancer and Chainlink.

Abstract

The intent is to recognise liquidity mining incentives played a large role in helping grow Aave V2 TVL, whilst being conscious that competitors continue to offer incentives APRs marginally exceeding what Aave is currently offering.

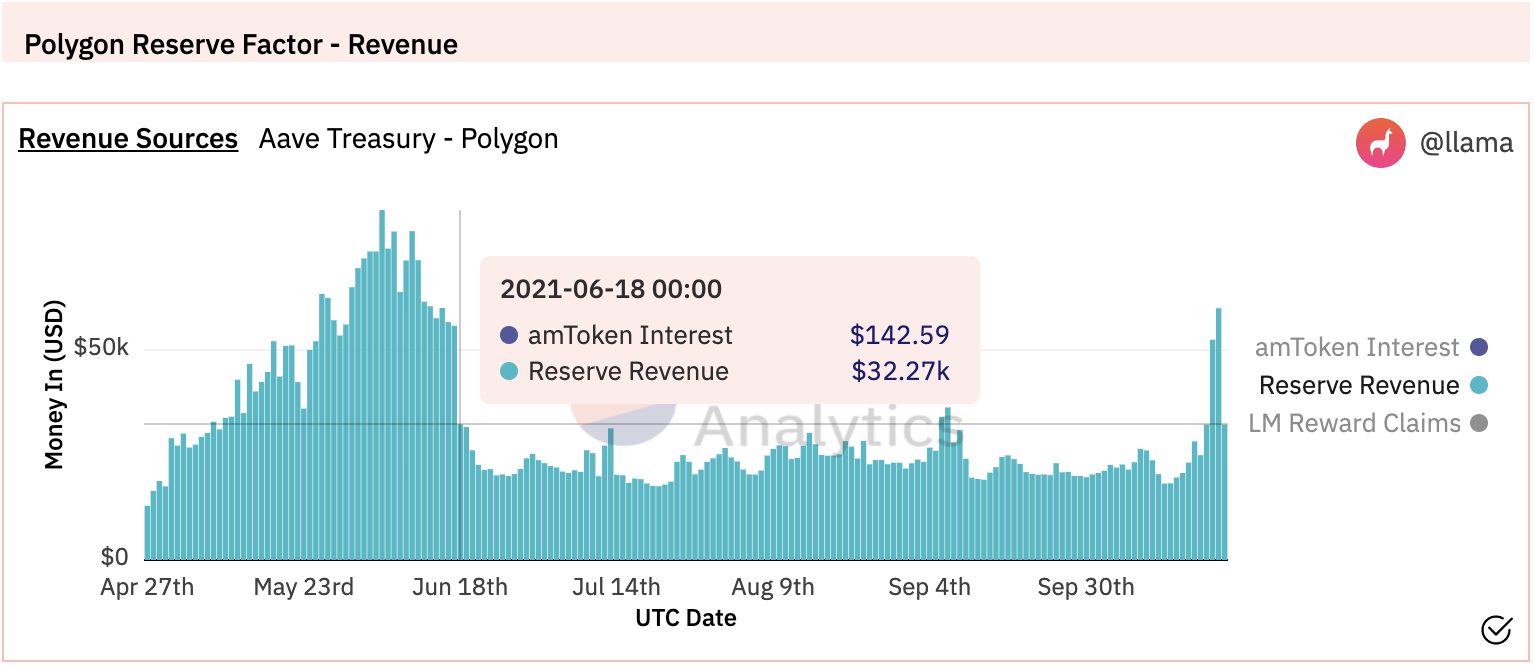

When incentives were reduced aggressively on the Polygon market, the daily revenue reduced significantly. There is a risk that by tapering liquidity mining incentives on Aave V2 too aggressively could trigger the same outcome as what was experienced on the Polygon market.

- AIP-16: 2,200 stkAAVE per day from 26th April 2021

- AIP-32: 2,200 stkAAVE per day from 24th August 2021

- AIP-XY: 1,540 stkAAVE per day from 22nd November 2021

Based on the learnings from the Polygon market and reviewing the governance forum, this proposal reduces Liquidity Mining rewards by 30% over the next 90 days. For the following 90 days during 2022, the logic would be to continue further reducing incentives pending how the market reacts to the implementation of this proposal.

It is to the benefit of the protocol to incentivise borrows more than depositors. Conceptually, incentivizing borrows already increases deposit rates, so passive depositors still benefit significantly.

To encourage the depositing of high volatility assets, this proposal suggests incentivising the lending of newly listed assets and continuing to offer incentives on those that are strategically important for the Aave community. Offering incentives on newly listed assets is expected to kickstart the supply of liquidity.

Motivation

As a community member, liquidity mining has been great for bringing more users as stakeholders for the Aave Protocol and distributing the governance power to a wider more decentralised group of holders. Distributing stkAAVE means users also backstoppers of the protocol and automatically have skin in the game.

I would say that most liquidity that a liquidity protocol such as the Aave Protocol needs is stablecoins - incentivised as diversely as possible and also encouraging stablecoins that are aiming towards decentralization such as RAI, FEI and FRAX.

I would like to present to the community an opportunity to continue distributing stkAAVE at the same rate per day across the Aave V2 market with the intention of achieving the following:

- Grow Total Value Locked (TVL)

- Increase liquidity

- Attractive (low) borrow rates

- Increase the protocol income via growing the Reserve Factor

- Redistribute governance power towards users of the platform

As the value deposited within the Aave V2 market has grown from ~$5B to ~$21B and the $AAVE price has underperformed this growth, the incentive APR is lower now relative to the start of the prior incentive period.

On the 17th June 2021, the incentives on Polygon were reduced by 5x and revenue fell from $55.77K per day to $32.27K per day. This highlights the risk of reducing incentives to hastily. It is worth noting Compound is providing liquidity mining rewards similar to the existing 2,200 stkAAVE distribution level in terms of APR across key stable coin (low vol asset) markets.

Ref. Details: Phase 1 and Phase 2 Liquidity Mining on Polygon.

Specification

The below section outlines the proposed liquidity mining incentives to be applied from 22.11.2021 up to and including 20.02.2022.

Key changes from the previous liquidity mining campaign:

- 30% reduction in incentives to 1,540 stkAAVE per day

- New additions BUSD, FEI, FRAX, CRV and DPI have all been included

- Removed UNI and GUSD incentives

- Incentives are skewed in favour of borrowers over lenders for low vol assets

- Borrowing incentives are not offered for borrowers of high vol assets

- Distribution of stkAAVE is pro rata based upon deposit dollar value

The table below shows the intend stkAAVE distribution across the various Aave V2 listings. The overall number of stkAAVE distributor per day is the same and with a larger capital base, generating to a lower APR. The allocations are based loosely around the dollar value of deposits (lenders) and position users to borrow stables. The intent is to drive borrowing demand which will then lead to a higher lending APR. This is further encouraged by incentivising depositing of higher vol assets as collateral which will grow the TVL.

Original Proposal.

Note: TVL per token is as per the 10th November 2021.

Final Proposal

Note: TVL per token is as per the 21st October 2021.

Math: % of value deposited x multiplier then scaled to provide LM Allocation that totals 100%. Link here.

All gas costs incurred implementing the AIP that follows on from this ARC is to be reimbursed by Aave in the form of $AAVE.

Rationale

Below is a list of the key considerations made when designing the third iteration of Liquidity Mining for the Aave V2 market:

- Compound continues to offer liquidity mining incentives that marginally exceed those on Aave V2 marketplace. Thus, the risk is that if incentives are reduced aggressively capital migrates to another platform offering more compelling incentives.

- When the Polygon market aggressively reduced incentives, TVL and therefore revenue dropped significantly. There is a risk that similar behaviour could be experienced on mainnet.

- Borrowing is the key activity on Aave. Only borrowers pay a fee to use Aave’s liquidity and Aave’s portion of this fee accumulates in the Reserve Factor. Thus, borrowers technically provide more value to the protocol by:

- Increasing depositor interest

- Increasing reserve factor earnings

- Incentivizing borrows more than deposits reduces the maximum earnings from a “leverage loop”

- Aave V2 TVL is heavily composed of three main stable coins (low vol assets) USDC, DAI and USDT. In effort to support the largest revenue generating pools, incentives are skewed towards low vol assets.

- In an attempt to grow TVL and capture the less centralised low vol asset markets, incentives for lending and borrowing assets like RAI and FEI have been introduced and are treated in a similar fashion to existing more centralised low vol assets like USDC. Note, neither RAI nor FEI are listed on any other Tier 1 money market protocol.

Capital Efficiency and Risk Considerations

- We did consider introducing a high health factor >2 which reduces the appeal of gamification and recursive lending. However, the implementation was ruled out as too much work and increased centralisation of the incentive scheme.

- Recursive behavior does not significantly increase risk as it is typically looped within a single asset. The Aave V2 market is designed to accommodate high levels of borrowing and the risk parameters set in place ensure the protocol is in a healthy state. The risk within the protocol is not connected to liquidity mining, but to the overall proper risk parameter management.

Economics

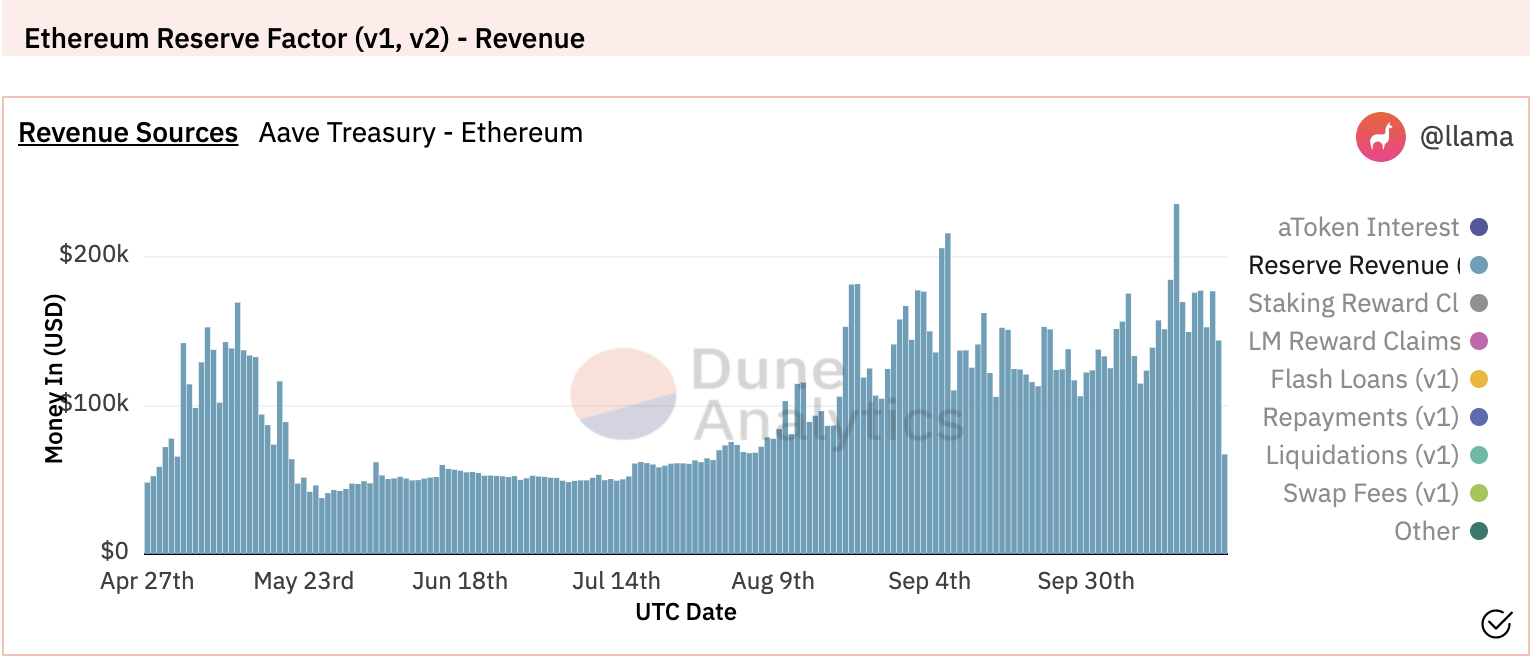

- Aave V2 markets daily Reserve Revenue is averaging around $170K per day. Daily aToken interest is around $3K per day.

- Liquidity Mining is estimated to cost $492,800 per day assuming 1,540 stkAAVE at $320 per token. Down from $704,000 per day assuming 2,200 stkAAVE at $320 per token.

- Ecosystem Reserve is worth around $700M with an AAVE price of $320.

- 90 days at 1,540 stkAAVE at $320 per token is $44,352,000 or around 6.33% of the Ecosystem Reserve.

- The Net spend is $29,052,000 per day after taking into consideration the daily Reserve Revenue and daily liquidity mining expenses. This does not take into consideration the 550 AAVE/day Safety Module incentives

- Daily Reserve Revenue is continually growing over time, any Reserve Revenue moving average trends higher from the middle of May onwards when the price of ETH dropped 60%.

Further details on the daily Reserve Revenue and Economic Reserve valuation can be found on the Aave Treasury Dashboard created by the Llama Community.

Copyright

Copyright and related rights waived via CC0.