Sentence Rational

Accept FIDU, the LP token to Goldfinch’s Senior Pool - a senior, diversified basket of real world loans - as collateral on Aave V2’s Ethereum market.

References

Project: https://goldfinch.finance/

Whitepaper: https://uploads-ssl.webflow.com/62d551692d521b4de38892f5/631146fe9e4d2b0ecc6a3b97_goldfinch_whitepaper.pdf

Document Portal: https://docs.goldfinch.finance/goldfinch/

GitHub: https://github.com/goldfinch-eng

Smart Contracts: https://dev.goldfinch.finance/docs/intro

Chainlink Oracle: WIP

Audit Reports: https://dev.goldfinch.finance/docs/security/audit-reports/

Communities: https://gov.goldfinch.finance/ & https://discord.gg/HVeaca3fN8 & https://twitter.com/goldfinch_fi

Paragraph Summary

FIDU is an ERC20 token representing a Liquidity Providers [LPs] position in the Senior Pool on Goldfinch. This is similar to the cUSDC token you get for depositing USDC into Compound. Liquidity Providers [LPs], who provide capital to the Senior Pool that is automatically allocated across Borrower Pools, take on less risk by providing second-loss capital via senior tranches.

This proposal is to add FIDU as a collateral asset on Aave’s V2 Ethereum market.

Motivation

N/A - technical solution is the same as all other assets onboarded onto the Aave V2 Market.

Specifications

What is the link between the author of the AIP and the Asset?

Ecosystem Lead at Warbler labs, a founding development team supporting the Goldfinch Protocol.

Provide a brief high-level overview of the project and the token.

Goldfinch is revolutionizing the $1T+ global private debt market by first allowing credit funds and FinTechs to access cost-efficient crypto loans. Goldfinch provides crypto lenders with access to debt deals collateralized with real-world assets that have been historically inaccessible outside exclusive networks.

The Protocol is expanding financial access for thousands of individuals around the world via its Borrowers, spanning over 20 countries. Some of Goldfinch’s Borrowers include PayJoy in Mexico, QuickCheck in Nigeria, Divibank and Addem Capital in LatAm, Greenway through Almavest in India, and Cauris in Africa, Asia, and Latin America. You can view more Borrower Pools here.

FIDU is a “digital receipt ” that represents an LP’s supply to the Senior Pool. The Senior Pool supplies senior capital that must be fully paid back before Backers (first-loss capital) receive their principal/interest repayments. FIDU increases in USDC exchange value as interest payments are made to the Senior Pool and only decreases in the case of defaults where the assets recouped are below the value of the loan.

Goldfinch to date has maintained a 0% default rate across a currently ~$100m in loans deployed and over $1M in protocol revenue.

Warbler Lab’s Founders are two ex-Coinbase employees with a team of ex-Goldman Sachs, Morgan Stanley, McKinsey, World Bank, Binance.US, Airbnb, Meta, BlockFi, and more. Goldfinch has raised a $25M Series A, backed by a16z, Kindred Ventures, Coinbase Ventures, Variant Fund, IDEO, Bill Ackman via TABLE, Kingsway Capital, Stratos, and more.

Aave has the opportunity to onboard a diversified selection of senior secured debt positions collateralized by real-world assets across 20+ different geographies.

Explain positioning of token in the AAVE ecosystem. Why would it be a good borrow or collateral asset?

The key benefits for Aave are:

- Diversifying the collateral within Aave’s V2 Ethereum market.

- Generating a new type of financial product in DeFi through Aave.

- Massive demand from current and future FIDU holders.

Currently, most of the assets listed in the lending market are entirely on-chain, highly volatile assets that are quite prone to cyclical bull and bear markets, as well as tail risk events like the UST collapse, de-pegging of stETH, and Black Thursday.

The Goldfinch Senior Pool, through FIDU, provides the safest and most diversified way by which Aave can onboard real-world assets. FIDU is much less volatile, sourced from across 20+ countries, and thus its underlying lending positions are not exposed to one regulatory and economic regime.

A Borrower Pool is the smart contract through which Borrowers borrow and repay capital. Once approved by Auditors, any Borrower can create a Borrower Pool and define the terms they want. Borrower Pool smart contracts have both a junior and senior tranche. Backers supply capital directly to the junior tranche, and the Senior Pool supplies capital to the senior tranche. When a Borrower makes repayments, the Borrower Pool applies the amount first toward any interest and principal owed to the senior tranche at that time, and then toward any interest and principal owed to the junior tranche at that time.

FIDU increases in price as repayments come into the Senior Pool. The Senior Pool is protected on-chain by 20% of junior capital. Which is generally further protected off-chain by an addition ~20% by the borrower. Thus the actual economic buffer is ~40%.

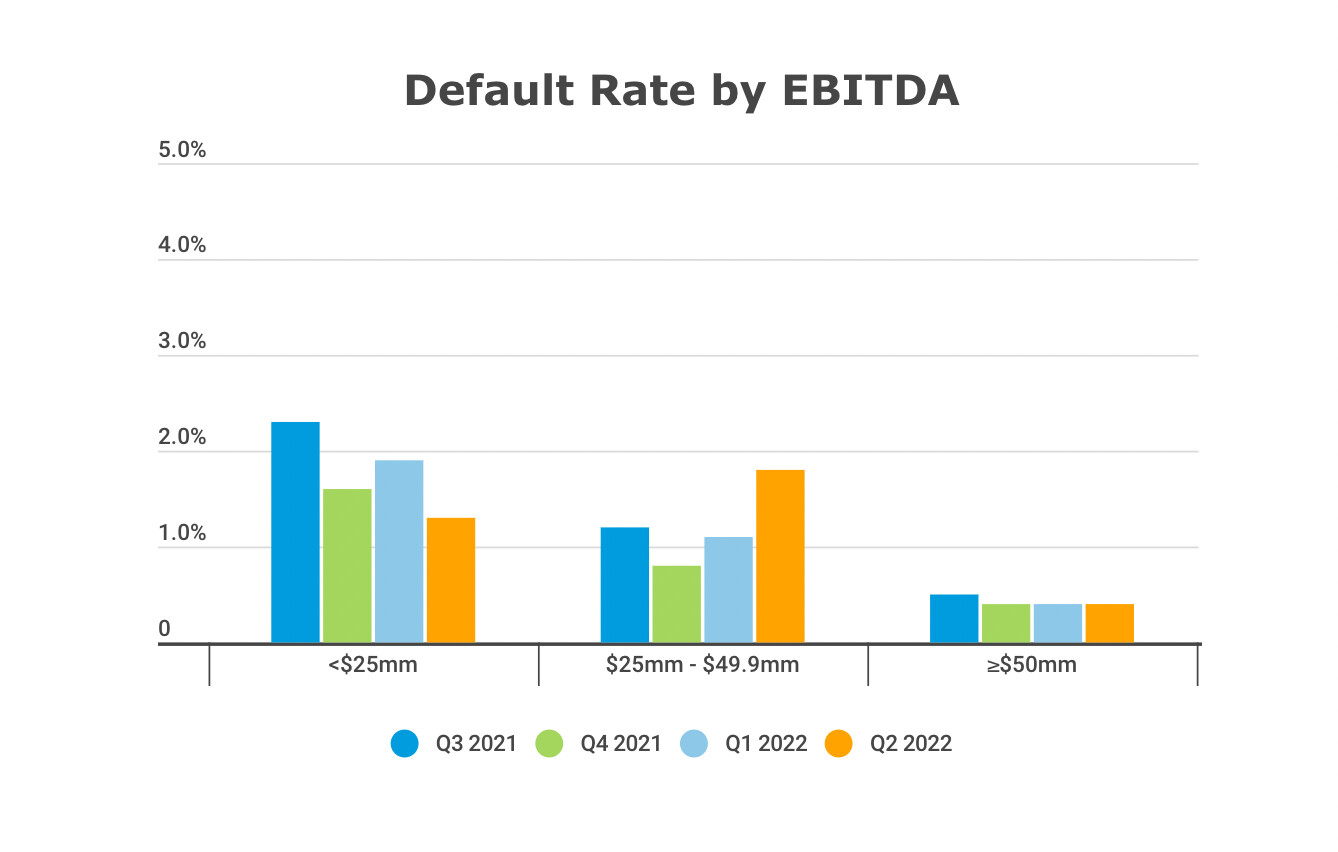

Even in such tumultuous macroeconomic times, the default rate on private credit remains at 1.18%. Do note that these are generic private debt default rates, and Goldfinch has historically had 0% default rates as our protocol sources and underwrites incredibly high-quality, low-risk borrowers with proven track records.

Source: Proskauer 2022 Q2 Private Credit Default Index

Borrowing FIDU itself would enable people to short private credit markets, which is the first product of its type in DeFi. Even in traditional finance, the ability to do so is limited for non-institutional investors.

Current and future Senior Pool investors will use stables to get liquidity on their FIDU positions without having to withdraw directly from the Senior Pool. LPs will borrow stables to take leveraged positions into the Senior Pool.

We expect this to de-risk investing in the senior pool for other LPs, give our bullish LPs a chance to take a levered position into our senior pool, and thus increase the amount of capital in the senior pool considerably, along with the market cap of FIDU. These effects will be significant as it is something we hear often from the Protocol’s current LPs.

Provide a brief history of the project and the different components: DAO (is it live?), products (are the live?). How did it overcome some of the challenges it faced?

Both Goldfinch the protocol and DAO are live. The FIDU token and the Goldfinch protocol both launched on January 2021.

So far the Protocol has deployed over $100M in loans with a 0% default rate. More data is available here: https://dune.com/goldfinch/goldfinch.

How is the asset currently used?

FIDU is a USDC-based yield-bearing token that represents your position in the Goldfinch Senior Pool.

Staked FIDU receives GFI rewards. In a soon-to-come product update, FIDU and GFI can be placed inside Membership Vaults to access enhanced yield.

Emission schedule.

There is no emission schedule; when USDC is deposited into the protocol, FIDU is minted. When a USDC is withdrawn, FIDU is burned.

Token (& Protocol) permissions (minting) and upgradability. Is there a multisig? What can it do? Who are the signers?

Governance is managed by a community DAO and has the ability to perform maintenance functions and parameter adjustments to the protocol via decentralized voting, including:

- Upgrading contracts.

- Changing protocol configurations and parameters.

- Selecting Unique Entity Check providers.

- Setting the rewards and distribution of GFI.

- Pausing protocol activity in the event of an emergency.

- Managing the protocol treasury.

The DAO’s on-chain actions are executed by the Goldfinch Council, which is a 6-of-10 multisig with 10 members who represent all stakeholders of the protocol.

The members are:

- Gautam Ivatury, Managing Partner at Almavest, one of the early Borrowers on Goldfinch. Almavest provides debt capital to high-performing companies in a variety of sectors globally.

- Alexandre Liege, CEO of Cauris, one of the early Borrowers on Goldfinch. Cauris is a credit fund created to bring decentralized financing to fintechs in emerging markets.

- Deltatiger.eth, an early Liquidity Provider and Backer on Goldfinch. Designed Synthetix monetary policy and active participant in many other protocols, including core team and multisig at boot.finance.

- Andrei Ansimov, an early Liquidity Provider and Backer on Goldfinch. Also an early Flashbots contributor and active participant with many protocols.

- Manish Adhikari, Goldfinch Discord Community Manager, and blockchain enthusiast.

- Viktor Bunin, Protocol Specialist at Coinbase Cloud and active contributor to many crypto communities.

- Nat Robinson, Co-Founder & CEO of Leaf Global Fintech, a company using crypto to provide affordable financial services for refugees in Rwanda, Uganda, and Kenya.

- Mike Sall, Cofounder of Warbler Labs, which is part of the Goldfinch community and supports the growth and development of the Goldfinch ecosystem and broader DeFi space.

- Blake West, Cofounder of Warbler Labs, which is part of the Goldfinch community and supports the growth and development of the Goldfinch ecosystem and broader DeFi space.

- Andrew Huelsenbeck, Head of Operations at Warbler Labs, which is part of the Goldfinch community and supports the growth and development of the Goldfinch ecosystem and broader DeFi space.

Market data (Market Cap, 24h Volume, Volatility, Exchanges, Maturity).

All data as of 9/12/2022.

FIDU Market Cap: ~$70M.

24h Volume: 7-day average is $338,733.55.

Volatility:

Note that prices are drawn from the Curve pool and do not reflect the price on the primary market. Gaps emerge based on liquidity conditions for redeeming and minting on the primary market. Specific volatility measures will be listed below.

Exchanges: Curve. Also mintable and redeemable in the primary market.

Maturity: The FIDU token was launched on January 2021.

Do note that FIDU is not the governance token for Goldfinch. The governance token for Goldfinch is GFI and has a different set of metrics that the ones listed above.

Social channels data (Size of communities, activity on Github).

Twitter: 49.6k followers.

Discord: 40k members.

Telegram: 5,554 subscribers.

Contracts date of deployments, number of transactions, number of holders for tokens.

The FIDU token and the Goldfinch protocol both launched on January 2021.

Holders: 2,415

Transfers: 14,409

Technical Considerations

We do not expect any special consideration for FIDU versus other existing collateral types from a technical perspective.

For the benefit of the Aave community “Goldfinch” encompasses a few different things, which we should distinguish:

- The Goldfinch Protocol

- A set of smart contracts on the Ethereum blockchain, which together comprise a decentralized credit protocol for financing off-chain economic activity.

- The Goldfinch Interface

- The web app served at https://app.goldfinch.finance, providing a convenient way (but not the only way) to use the Goldfinch Protocol.

- Goldfinch Governance

- A governance system for governing the Goldfinch Protocol, built around the GFI token and the discussion forum served at https://gov.goldfinch.finance.

- Warbler Labs

- The company which initially developed the Goldfinch Protocol and the Goldfinch Interface.

Security Considerations

Security is of absolute, paramount importance in the development of the Goldfinch Protocol. To that end, Goldfinch engages external auditors to review all smart contract code. Warbler Labs also maintains its internal audit process for all smart contract code.

Since its inception, Goldfinch has published the report from every external audit in an open-source repo.

Additionally, there is a live $500k bounty here.

Furthermore, Goldfinch has an industry leading DeFi Safety Score of 93% which you can read about here. This is equivalent to other bluechip DeFi protocols like Compound and Yearn.

Risk Analysis

The overall risk profile for FIDU is: C. However, we think the asset is sufficiently different enough from others that the existing framework is a poor capture of the real risk of the asset.

Smart Contract Risk

The current smart contract risk score is greatly reduced because of the smaller number of transactions. Because FIDU represents a low volatility, yield generating LP token, it will naturally have a smaller number of transactions versus tokens that are more volatile and thus traded more frequently, or medium of exchange stable coins that are meant to be transacted.

A credible, 3rd party risk assessment here is produced by DeFi Safety. They have a report produced by the organization that assigns Goldfinch an industry leading DeFi Safety Score of 93% which you can read about here. This is equivalent to other bluechip DeFi protocols like Compound, Yearn, and Aave. Notably, it is far above other assets currently listed on Aave like Maker.

As such, we think A- represents a more accurate Smart Contract Risk score.

Counter Party Risk

Similar to the Smart Contract risk, the score is reduced due to the Holders metric. Because FIDU is a token that people get for actually using the protocol, and not a speculative token for traders, the number of holders does a poor job of representing what this metric is meant to represent.

The current metric uses number of holders as a measurement of decentralization as a proxy for governance power distribution over a protocol. As FIDU is not a governance token, it does not fit such a metric. The number of holders of FIDU are approximately the same as yUSDC, a similar LP token.

Because FIDU is totally permission-less and Goldfinch, the protocol behind FIDU, follows the best practices around DAO governance, we view a B+ as a more accurate Counter Party Risk score.

Market Risk

As Market Risk has much more direct, quantifiable metrics, we are okay with our current score. It is worth noting that the Market Cap is not a speculative one, but rather a correlation with the amount of USDC deposited into the Senior Pool.

The current volatility is driven by fluctuations in the secondary market. We expect to reduce that greatly through quick to come product initiatives like Withdrawal Mechanics and a more efficient DEX source.

As pointed out before, FIDU is protected by an actual economic buffer of 40% before it starts losing any value.

Adjusted Score

The adjusted overall risk profile for FIDU is: B.

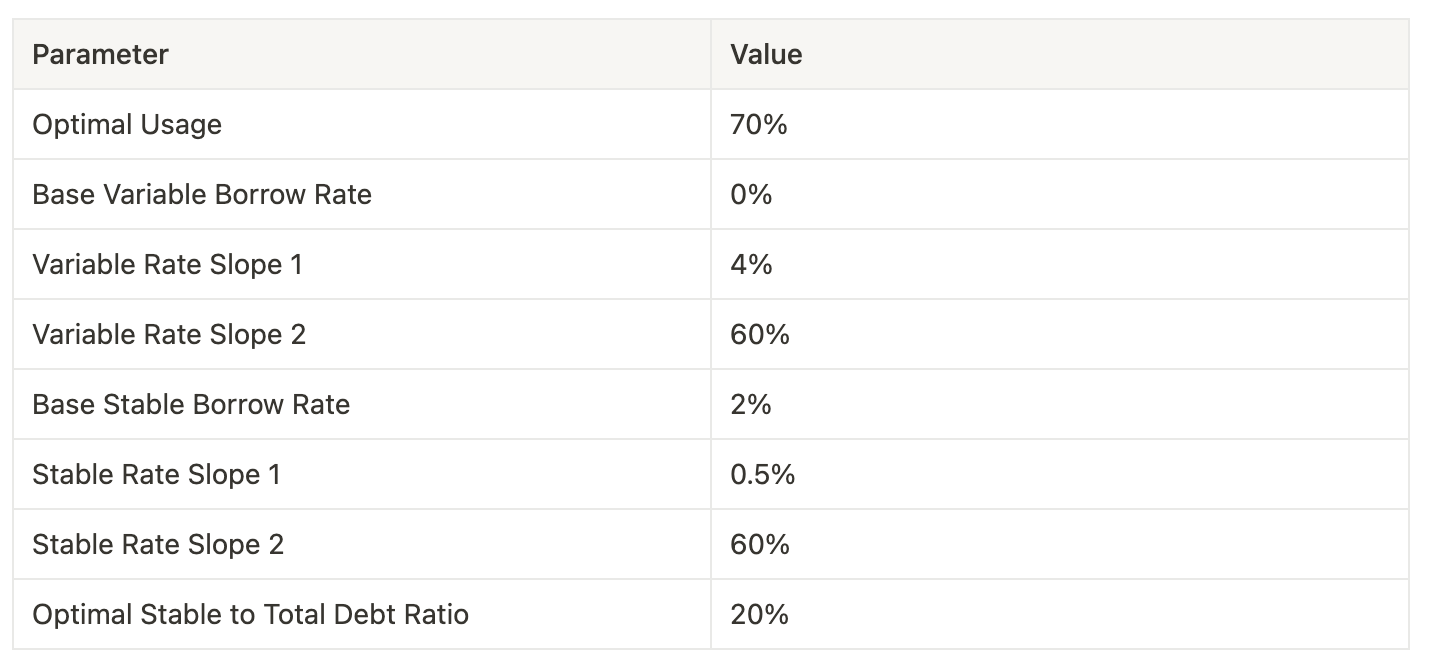

Parameters

Per the archetypes described here: https://docs.aave.com/risk/liquidity-risk/borrow-interest-rate, we view FIDU as most closely following Rate Strategy Stable One.

We adjusted the Optimal Usage metric to better reflect the market conditions of FIDU as compared to the example Dai.