Proposal: Add support for wstETH on Optimism Aave V3

References:

Project: https://lido.fi/

Whitepaper: core/README.md at master · lidofinance/core · GitHub

Github: lido-l2/contracts/optimism at main · lidofinance/lido-l2 · GitHub

Documentation: https://docs.lido.fi/

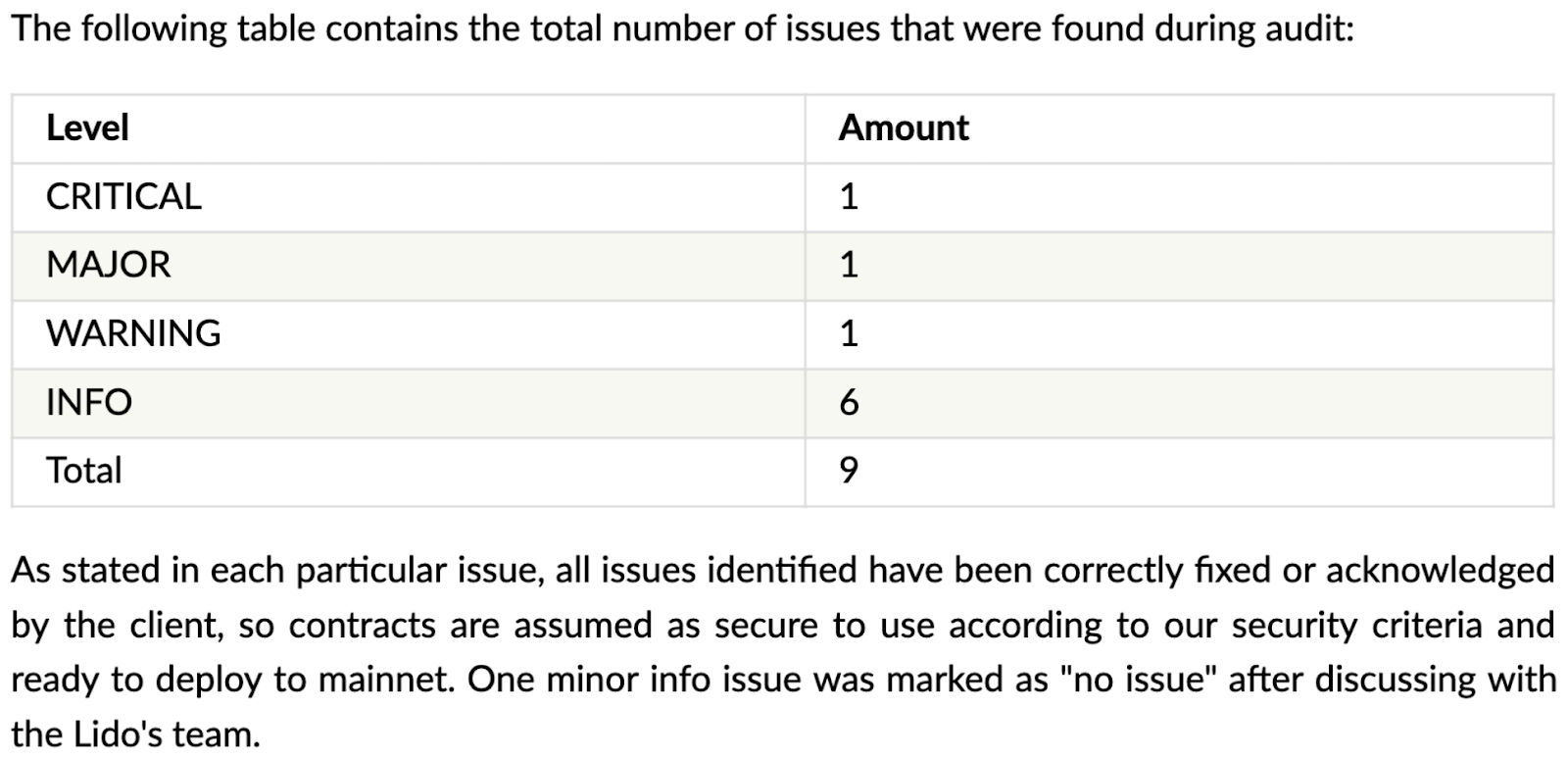

Audit: https://github.com/lidofinance/audits/blob/main/Oxorio%20Lido%20L2%20Smart%20Contracts%20Security%20Audit%20Report%2007-2022.pdf

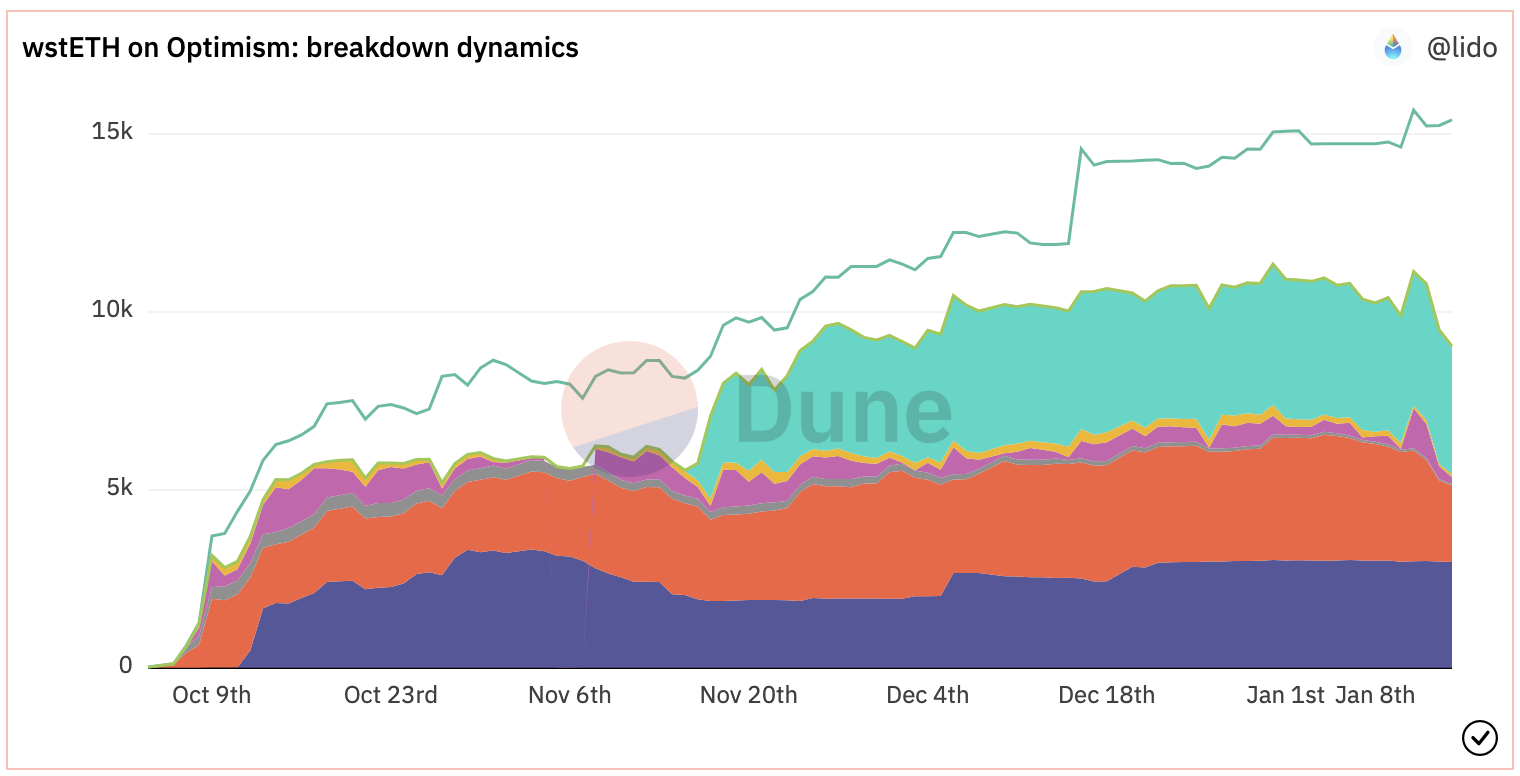

Dune: https://dune.com/lido/wsteth-on-optimism`

wstETH: Lido: Optimism Governance Bridge Executor | Address: 0xefa0db53...805966fc3 | OP Mainnet Etherscan

Chainlink: Chainlink: wstETH-stETH Exchange Rate | Address: 0xe59EBa0D...F2707dc77 | OP Mainnet Etherscan

Governance: https://research.lido.fi/

Twitter: https://twitter.com/LidoFinance

Discord: Lido

Lenster: https://lenster.xyz/u/lidofinance.lens

Summary:

This ARC presents the community with the opportunity to add wstETH to the Optimism V3 Liquidity Pool.

Motivation

The stETH Reserve on Aave V2 is the largest Reserve across all Aave deployments with $1.09B in deposits, exceeding USDC ($1.08B) and ETH ($1.03B). This is partially due to several communities having built products that deposit stETH and borrow ETH as part of a rewards-maximising strategyThe demand for stETH has increased as a result of listing stETH on Aave V2, which has increased the Lido DAO takes a small percentage of rewards received by staking ETH as revenue. Listing of stETH by Aave has enabled Aave to offer the best return on ETH, in ETH terms, across major lending markets, continually outperforming Compound. By listing wstETH on Optimism, the Aave community is helping create an environment capable of replicating the success of the Ethereum Mainnet Aave V2 Liquidity Pool.

Specification

1. What is the link between the author of the AIP and the Asset?

Jacob is a full time contributor to the Lido DAO

2. Provide a brief high-level overview of the project and the token?

Lido protocols enhance the security of the network by enabling more users to stake ETH. When they stake ETH through the Lido Protocol software they receive stETH. stETH tokens are fungible and liquid. The total balance of stETH in existence is based on the total amount of ETH staked via the Lido protocols plus total staking rewards minus any slashing applied on validators. stETH rebases daily.

Due to the rebasing nature of stETH, a user’s stETH balance changes daily as staking rewards are received. As some DeFi protocols require a constant balance mechanism for tokens, Lido protocols offer wstETH, which is a wrapped version of stETH. wstETH keeps a user’s token balance fixed and uses an underlying share system to reflect users’ receivedstaking rewards.

Example:

- Wrap 100 stETH to 99.87 wsETH

- Continue to receive rewards on your wstETH

- Unwrap wstETH, receive 101 stETH

When redemptions are available, wstETH can be redeemed for unstaked ETH and accumulated rewards.

wstETH on Optimism: 0xefa0db536d2c8089685630fafe88cf7805966fc3

3. Explain positioning of the token in the AAVE ecosystem. Why would it be a good borrow or collateral asset?

The below shows the effect that listing of stETH has had on the Aave v2 Ethereum Mainnet deployment. stETH drives most of the ETH borrowing demand and the resulting fee-revenue. The ETH reserve generated approximately $120k in revenue during October and has already generated $124k by late November.

4. Provide a brief history of the project and the different components: DAO (is it live?), products (are they live?). How did it overcome some of the challenges it faced?

The below provides a brief overview and some key dates of interest providing insight into the history to stETH and wstETH:

- stETH deployed on 17th December 2020

- stETH listed on Aave V2 on the 27th February 2022

- wstETH deployed 5th August 2022

- wstETH to be listed on Ethereum V3 deployment discussion 11th October 2022

The Lido protocols account for up 30.3% of the staked ETH deposits. This is the most frequently used protocol to stake ETH.

5. How is the stETH token currently used?

Aave V2 on Ethereum is the largest holder of stETH.

Deploying wstETH on Optimism, along with on other networks like Arbitrum, will make the token available to Aave users on Layer 2 networks in the same way stETH is available on Ethereum Mainnet. It will also enable DeFi protocols and products on Optimism to build interesting and exciting new use cases by utilizing integration with Aave to access the wstETH market.

InstaDapp, Index Coop, Galleon DAO, and others have all built products on top of Aave utilizing the recursive stETH/ETH strategy. By adding wstETH to the Optimism Liquidity Pool, Aave moves closer towards enabling developers to deploy similar products on Optimism.

On Optimism, wsETH is mostly used for providing liquidity on various incentivised decentralized exchanges.

6. Emission schedule

There is no emission schedule.

7. Token (& Protocol) permissions (minting) and upgradability. Is there a multisig? What can it do? Who are the signers?

For details on stETH, which is already listed on Aave V2 Ethereum, please refer to the forum post shown below:

The custom bridging contracts for the Optimism native bridge have been developed by the Lido dev workstream. The code was submitted for audit and the audit report can be found below:

The Optimism bridge is owned by Lido DAO on L1. This means, no actions can be performed on bridges without explicit Lido DAO approval (beside pausing the bridges). Just like the L1 part of the setup, the L2 one is also designed to be upgradeable. The L2 upgrades are implemented via governance approval on Ethereum and leverages the Aave Governance Cross-Chain bridges contracts.

For security, Emergency Brakes multi-sigs have been set up on Optimism. The multi-sig can pause deposits/withdrawals. However, only the Aragon Agent is capable of resuming bridge operations. The Optimism multi-sig address is shown below:

The multi-sig composition is 3 from 5 of the following signers:

- @psirex with address 0x2a61d3ba5030Ef471C74f612962c7367ECa3a62d

- @vsh with address 0x2a96805188e583dd760785A0dE93128504DDd5c7

- @kadmil with address 0x6f5c9B92DC47C89155930E708fBc305b55A5519A

- @ujenjt with address 0xdd19274b614b5ecAcf493Bc43C380ef6B8dfB56c

- @folkyatina with address 0xCFfE0F3B089e46D8212408Ba061c425776E64322

8. Market data (Market Cap, 24h Volume, Volatility, Exchanges, Maturity)

- Market capitalisation: $5,651,971,852

- 24H Volume ~$50M (stETH + wstETH)

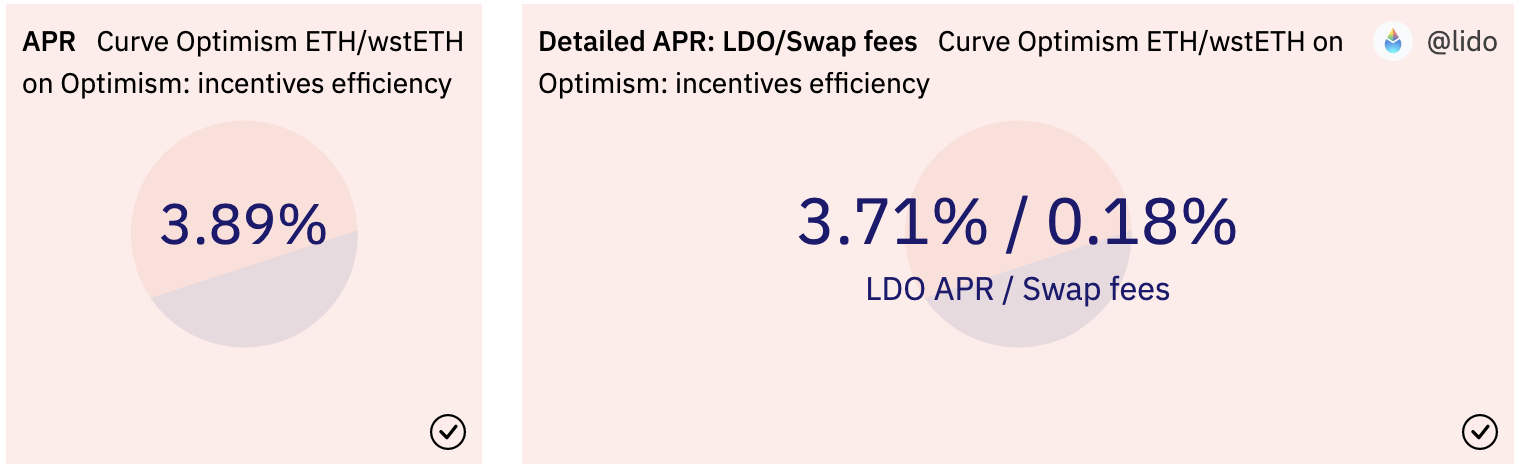

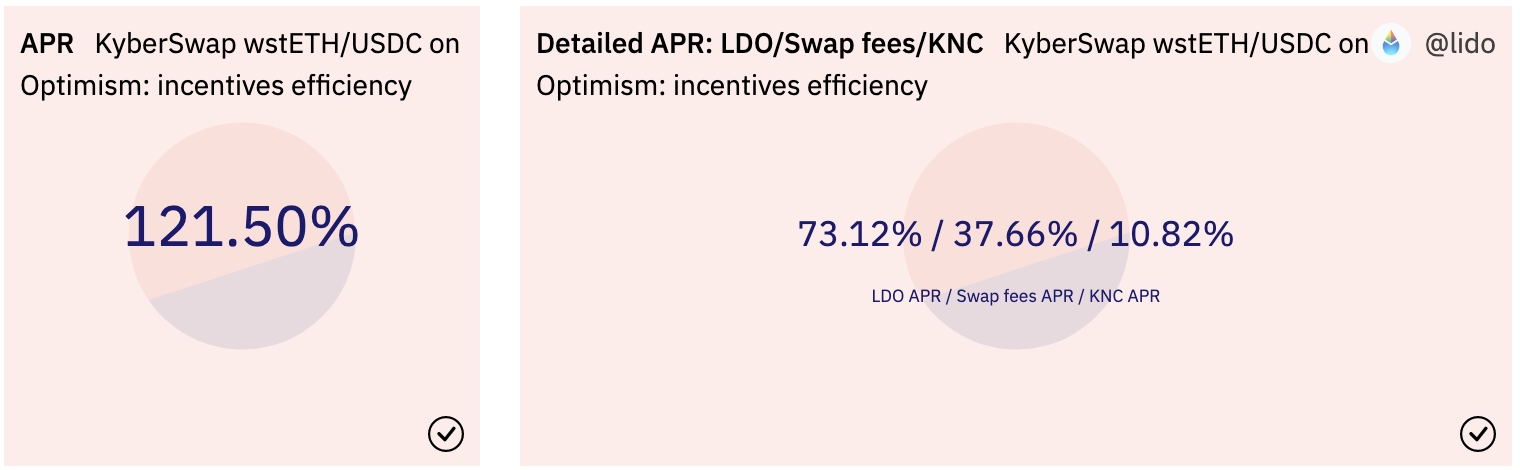

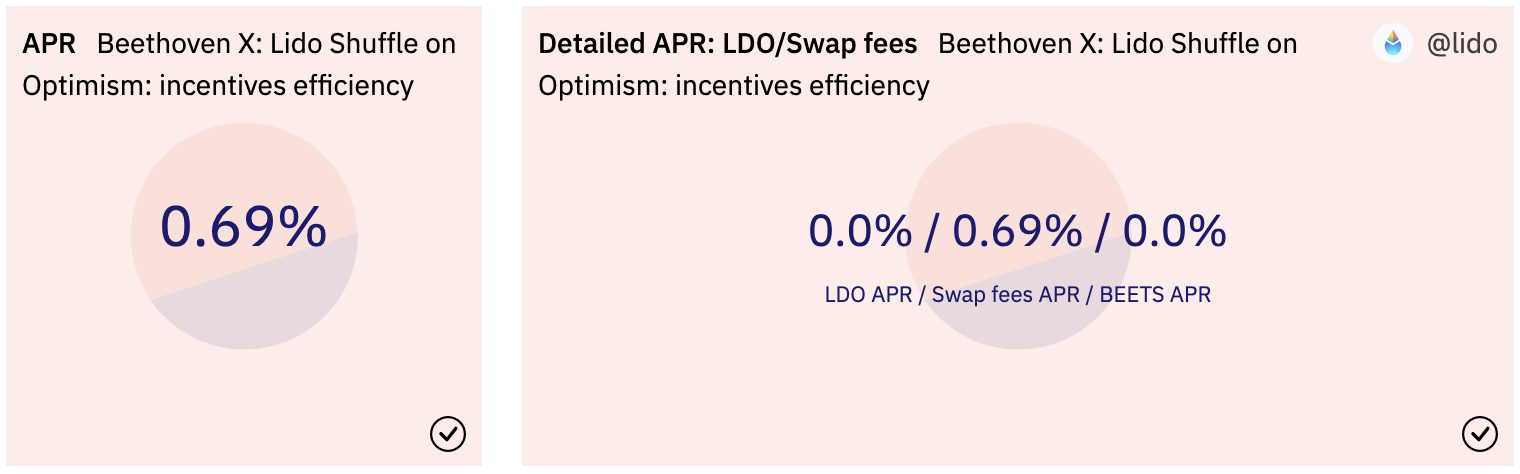

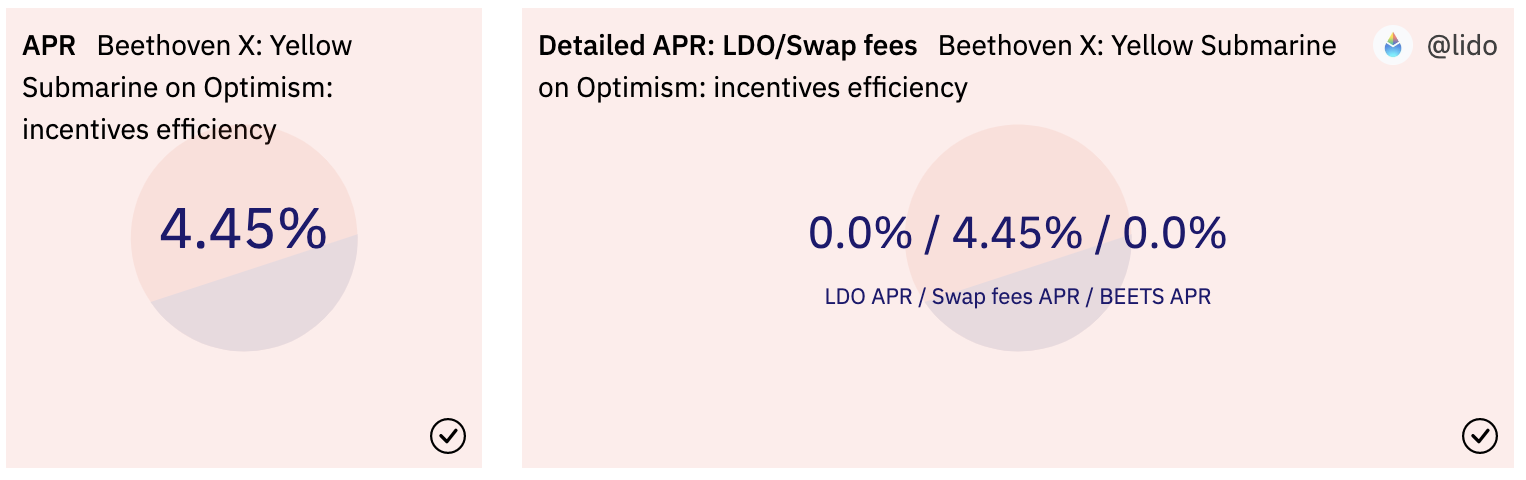

Decentralized exchange liquidity pools

Beethoven

- wstETH/bb-rf-aWETH - 0xde45f101250f2ca1c0f8adfc172576d10c12072d

- wstETH/bb-rf-aUSD/bb-rf-aWBTC - 0x981Fb05B738e981aC532a99e77170ECb4Bc27AEF

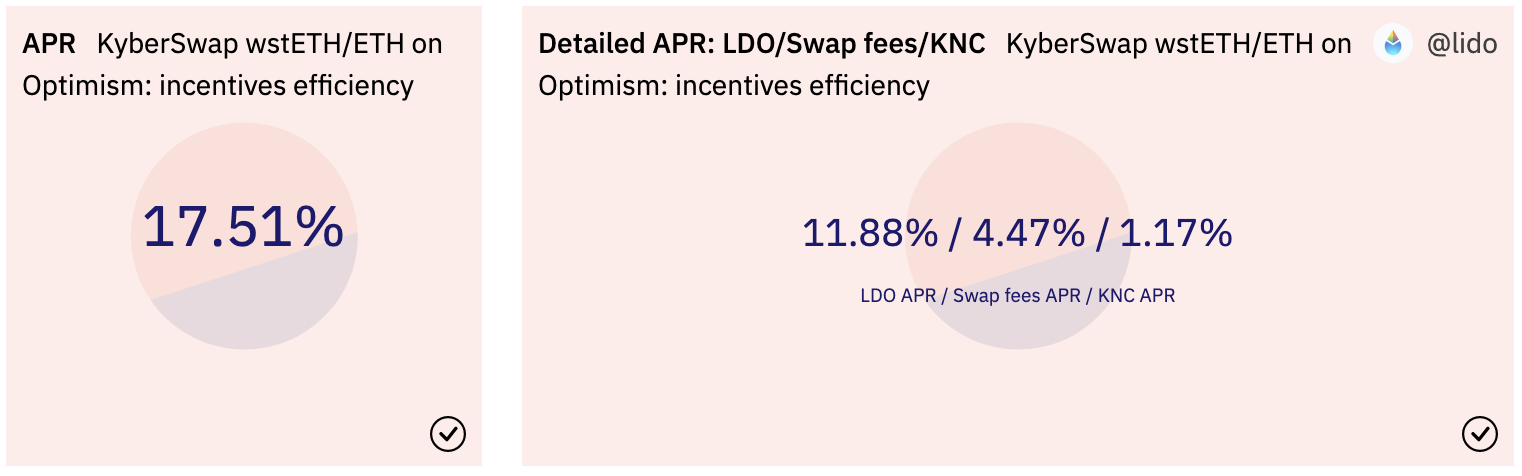

Kyber Network

- wstETH/ETH - 0xda74db17023750d02b83be2559a4eaa013b65c54

- wstETH/USDC - 0x5fc53f707c7aacd460a1cd564c06e0f07610fcb7

9. Social channels data (Size of communities, activity on Github)

10. Contracts date of deployments, number of transactions, number of holders for tokens

The below applies to just wstETH on Optimism:

- Date of Deployment: August, 05 2022

- Number of Transactions: 106,563

- Number of holders for token: 907 (liquidity pools are recorded as 1 address)