Liquidity Mining v1

Liquidity mining incentives were introduced for Aave v2 on 4/26/21.

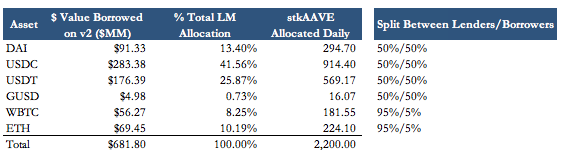

2,200 stkAAVE per day will be allocated pro-rata across supported markets based on the dollar value of the borrowing activity in the underlying market. stkAAVE was distributed over AAVE to further align users with the Aave Protocol and increase the amount of AAVE staked in the safety module.

Liquidity Mining Recap

-

Value Distributed: During the liquidity mining campaign, 198,000 stkAAVE will be distributed to borrowers and lenders on Aave v2, using ~7% of the Ecosystem Reserve. This equates to $82MM in rewards (AAVE VWAP since LM program started).

-

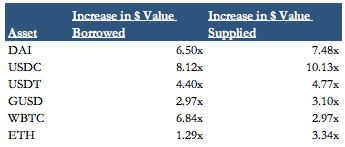

TVL: v2 TVL rose from $7.8 billion to a high of $14.4 billion in mid-May. Stablecoin liquidity accounts for more than 60% of total Aave v2 liquidity.

-

V1 to V2 liquidity migration: v1 liquidity decreased from $2.5 billion to $372MM since the liquidity mining program started. 40% of Aave liquidity was deployed in v1 before the LM rewards started. Aave v1 liquidity now accounts for less than 3% of all liquidity on Aave. This allows the community to remain focused on v2 and upcoming money markets.

-

Growth in dollar value supplied and borrowed: The USDC and DAI markets experienced the largest increase in dollar value supplied and borrowed. Note - many users on these markets have recursively levered their position to maximize yields. Recursive leverage accounts for ~32% of all deposits on v2. This compares to ~40% on Aave’s Polygon market.

-

Reserve Growth: Aave reserves help provide the first layer of protection for borrowers and lenders. Since liquidity mining rewards launched, Aave’s v2 reserves have grown by ~$7MM.

Change in v2 markets from 4/26/21 to 7/15/21

Liquidity Mining v2

In v2 of the liquidity mining proposal, we propose the following:

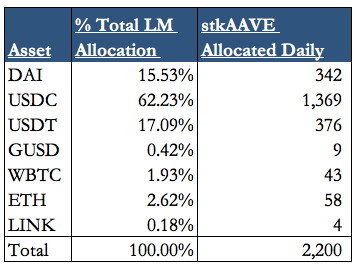

- Keep the same 2,200 stkAAVE per day distribution. Over a one year period, this equates to 803k stkAAVE distributed or ~27% of the ecosystem reserve.

- Include LINK in the liquidity mining program. We have seen close collaboration between the LINK and AAVE communities. The Aave community signaled support for adding LINK.

- We propose the Aave Risk DAO explore a separate shorter-term liquidity mining proposal for new assets. For example, this program would allow newly onboarded assets to benefit from LM rewards. This program would facilitate shorter and targeted LM distributions.

- Update the LM distribution - applying the same, formulaic approach to current borrowing demand on Aave v2 as of 7/15/21. Note - this distribution does not adjust for recursive leverage. While this distribution allocates a relatively low amount of stkAAVE to the LINK market, this number can be scaled up over time. Similar to other markets, current borrowing demand is used to determine the allocation of stkAAVE to the LINK market.

We would love to hear the community’s feedback on these parameters.

- Yes

- No

0 voters