Overview

Chaos Labs recommends listing Resolv’s USR stablecoin within Aave V3’s Ethereum Core Instance Deployment. Below we present a comprehensive analysis and recommendations.

Resolv

Resolv is a protocol that operates the USR stablecoin and the Resolv Liquidity Pool (RLP). USR maintains stability through delta-neutral ETH-denominated spot and perpetual positions across multiple exchanges, similar to Ethena. RLP, meanwhile, functions as the protocol’s liquid insurance pool, serving as the junior tranche responsible for upholding collateralization.

Unlike USDe, which primarily distributes yield to sUSDe stakers while periodically allocating revenue to an insurance fund for over-collateralization, Resolv employs a more dynamic approach. It balances yield distribution between two key entities: RLP holders, who serve as the first line of defense against negative funding rates or adverse market conditions that could impact collateralization, receiving rewards based on the prevailing risk premium and implied collateralization ratio, and USR stakers, who benefit from greater insulation due to this structured risk allocation.

To mitigate systemic risk and reduce reliance on centralized entities, Resolv diversifies its collateral composition and distributes collateralized debt positions across multiple exchanges. This approach enhances the protocol’s resilience while ensuring transparency and capital efficiency.

USR

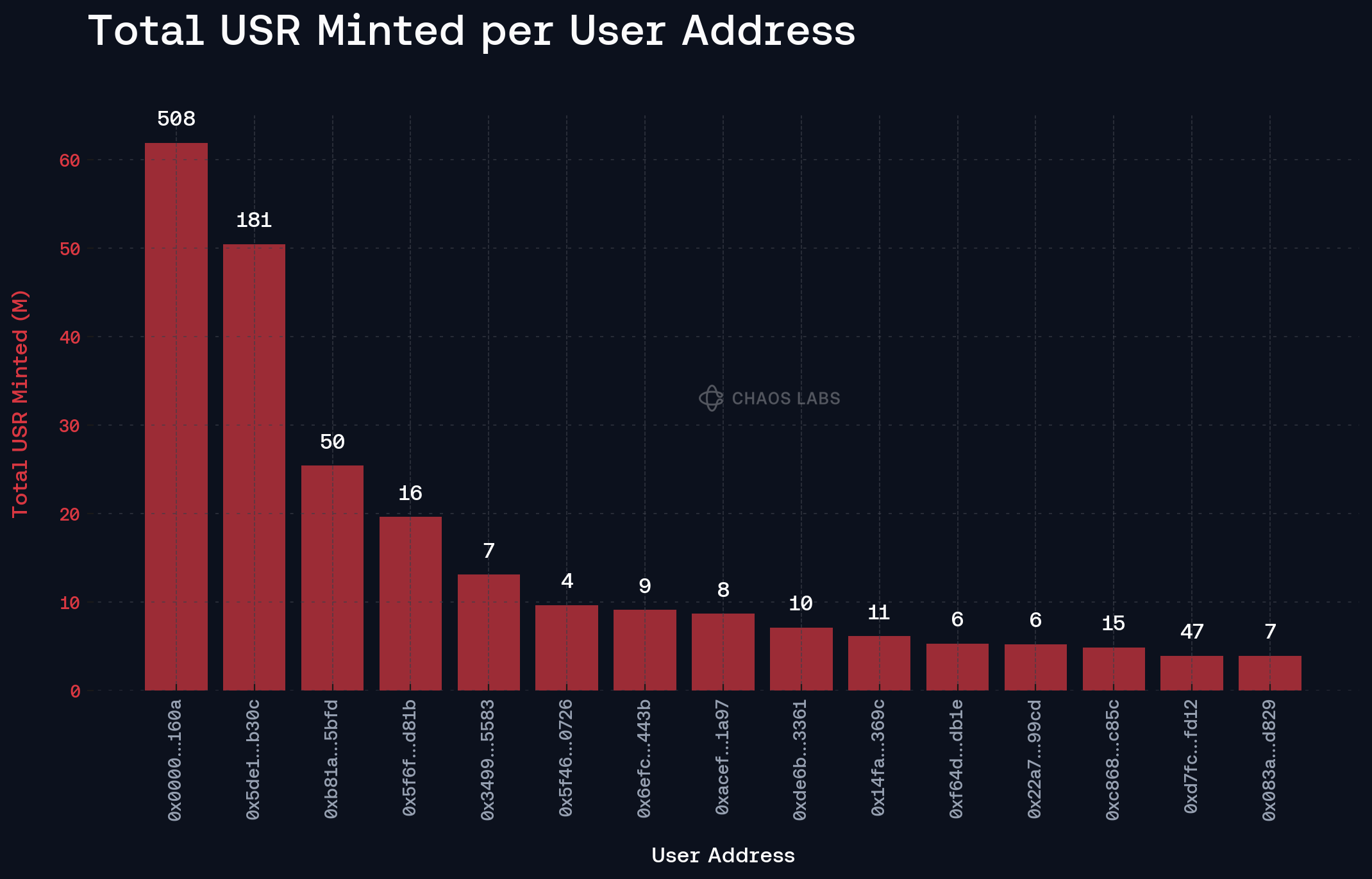

USR can be minted by whitelisted entities using USDT or USDC at a 1:1 ratio less a minting fee. The distribution of such USR minting has been performed by 71 bespoke addresses, highly concentrated within the top minters.

USR can be staked as stUSR to earn staking rewards in rebasing fashion, with an implementation akin to stETH. stUSR can be wrapped into wstUSR to aggregate these rewards in its price, making it friendlier for integration throughout the DeFi ecosystem. Since April, stUSR’s average staking APR has been 9.05%, decreasing significantly in recent weeks in accordance with the recent funding drawdown.

Source: Resolv Interface

Historically, per the recent push to incentivize vanilla USR, the percentage of USR supply staked in stUSR has continued to decrease, reaching 32% today.

Collateral Pool

The collateral pool uses various strategies to maintain delta neutrality while generating yield that passes through to stUSR and RLP and manages liquidity. The majority of this strategy involves implicit collateralization of LSTs to neutralize ETH short perp positions to collect funding, coupled with yield generation through USD-denominated strategies to maintain swift liquidity availability, similar to Ethena.

USR’s current on-chain supply is 531M, with a collateral pool backing of $636M. The majority of this is held in the on-chain treasury wallet, holding a combination of stablecoins and LSTs, while 32% is held in institutional custody (Ceffu funds are used as collateral on Binance, Fireblocks on Deribit), and 30% is held on exchanges.

Source: Resolv Interface

The collateral pool’s holdings are weighted towards ETH-correlated assets, particularly wstETH at 40.9% of the total. Resolv utilizes funds in the collateral pool to manage short-term liquidity requirements (either from redemptions or margin requirements) by borrowing WETH against wstETH on Aave V3 — Ethereum with a target health factor of 2.0. If a portion of wstETH as collateral is higher than 50%, the remaining part is unstaked to redeem borrowed ETH. The pool also holds $116M in USD-denominated assets, corresponding to 18% of total backing.

Source: Resolv Interface

Additionally, at the bottom is displayed the current position size on each exchange, roughly matching the target allocation provided in the documentation, which states that integrations with OKX and Bybit are planned.

RLP

The excess collateral in the collateral pool forms the basis for RLP, a token representing this share of the pool. Minting and redeeming the token functions in the same way as USR.

Profits and losses in the collateral pool are calculated at 12 UTC, every 24 hours. 70% of the reward is allocated pro rata to stUSR via the RewardDistributer contract, while 30% is allocated to RLP. If there are losses during an epoch, these are allocated only to RLP, effectively acting as the junior tranche, making it a higher risk and higher reward token. Additionally, in an effort to maintain a significant buffer in the reserve to protect USR collateralization, the redemption of RLP is suspended if the USR collateralization ratio falls below 110%.

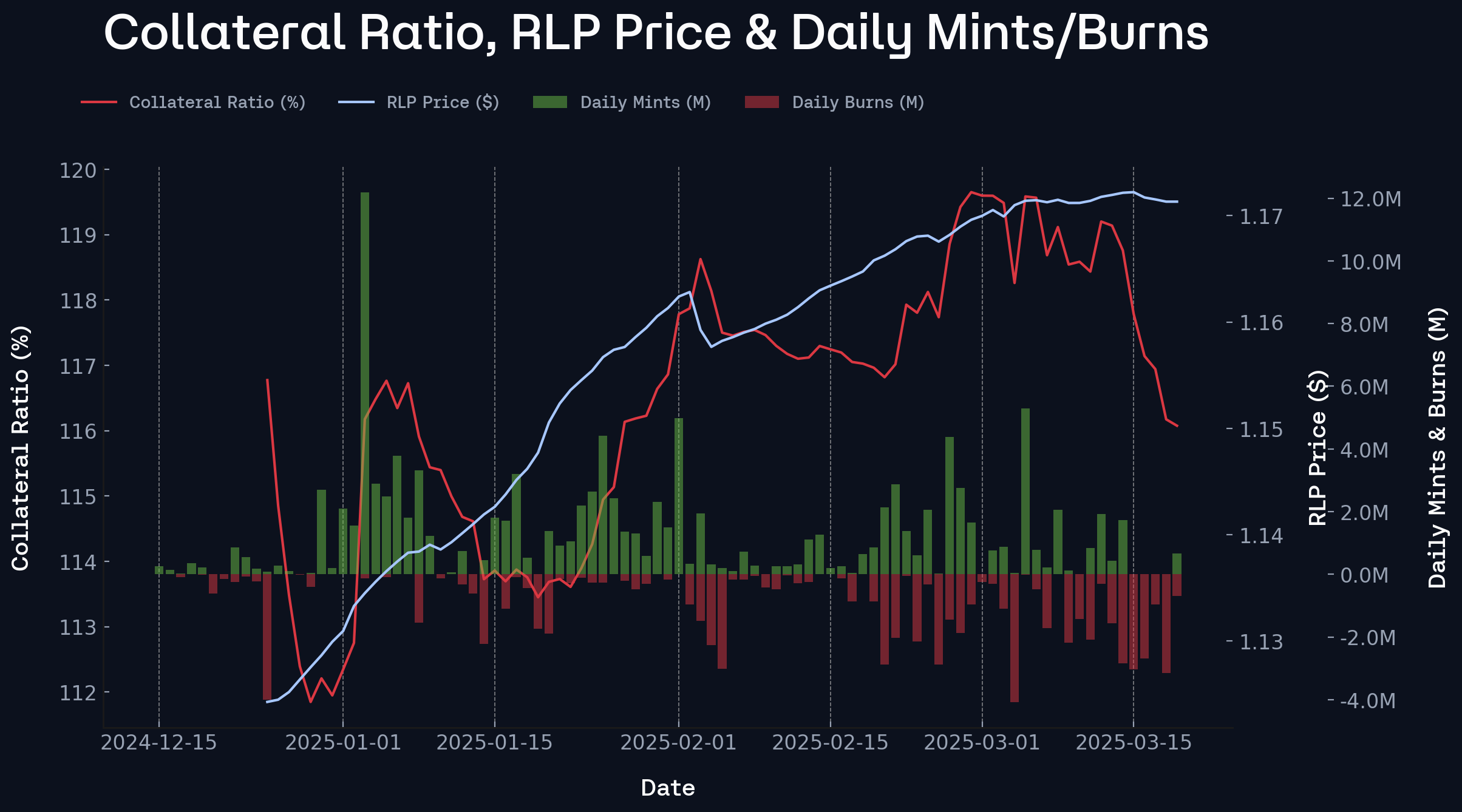

Given the mechanics of RLP, withdrawal requests are expected to surge following a negative funding round, driving USR over-collateralization downward in a first-come, first-served manner. This asymmetry results in increased expected delta exposure due to potential losses realized by the system, while inversely allowing for a decrease in expected delta exposure through large RLP fee distributions, which support a rebound in collateralization. This mechanism aims to optimally maintain an over-collateralization target while enabling system scalability.

This dynamic is clearly illustrated in the following chart, where RLP mints increase in both size and frequency during periods of positive RLP price growth, while redemptions surge during periods of negative growth driven by negative funding events. Furthermore, the lack of negative rebase risk for USR holders adds an additional layer of risk to RLP, as an increase in USR supply could push the collateralization ratio toward the critical 110% threshold. The ongoing point system further exacerbates this effect.

In the context of USR collateralization, even if the collateralization ratio were to reach its minimum threshold of 110%, triggering a suspension of redemptions, the system would still maintain a substantial buffer to preserve over-collateralization in adverse scenarios. Additionally, the natural recovery of over-collateralization through RLP supply growth aligns with the system’s inherent risk framework. This alignment is reinforced by the fixed 30% “risk premium” distribution of aggregated yield to RLP holders, which, in relative terms, facilitates an upward scaling of collateralization during periods of strong yield accrual.

USR PoR and Mint-Redeem Functionality

To redeem USR for its equivalent backing in stablecoins (similar to Ethena), the system follows a two-step process: users first create a USR burn request (burnRequestCreated), which is then executed (burnRequestCompleted) after a variable time buffer determined at the protocol’s discretion, receiving relevant withdrawal assets (USDT/USDC) from the Treasury contract. This process differs from Ethena’s atomic redemption mechanism, where the Mint and Redeem contract is pre-funded with whitelisted withdrawal assets, with a replenishment traditionally triggered when the contract holdings fall below ~28M, topping up to a targeted value of ~30M stemming from internal stablecoin liquidity sources - feasibly performed due to the 2M redemption limit per block.

Below, we illustrate the cumulative USR redemptions relative to the time elapsed between request creation and execution. Notably, redemptions have been completed at a weighted average clip of 1.8 hours, with 50% executed within one hour and 75% within two hours.

USR withdrawals are highly distributed across numerous redeemers, with no clear correlation between the size of the redemption and the execution time of the withdrawal.

Redemption Price Oracle

When a user redeems USR tokens, an internal pricing mechanism is leveraged to determine the relative value per redeemed token. For USR, the redemption contract first fetches the withdrawal token’s real-time price using getRedeemPrice, which retrieves the Chainlink market oracle valuation of the underlying asset looking to be obtained, i.e. USDC. It then multiplies the price by the latest USR token price from getUSRPrice. The USR price itself is dynamically calculated within UsrPriceStorage via setReserves, which allows an authorized SERVICE_ROLE to update the price based on USR token supply and available reserves, typically performed once a day at 12:10 UTC. If the USR price hadn’t been updated within the usrPriceStorageHeartbeatInterval or 30 hours, the transaction was to revert.

This pricing logic effectively operates under a PoR-esque implementation, ensuring that if reserves fully back the supply, the price remains fixed at 1:1. However, if reserves are lower than the total USR supply, the price scales down proportionally to prevent overvaluation, such that price = (reserves * 1e18 / usrSupply). With the use of the USDC market oracle, the protocol aims to target a redemption valuation in dollar terms with respect to the PoR price, thereby rewarding more USDC per USR if its market price is below $1. Formally, the redemption price of USR at a given time t is calculated through the following formula:

![]()

Once the redemption price is determined, USR tokens are then burned and an equivalent amount of withdrawal tokens are received based on the computed price, applying a redemption fee to control the process. The contract then checks treasury reserves (treasuryWithdrawalTokenBalance) to ensure there are enough withdrawal tokens available. If reserves are insufficient, it borrows the missing amount from Aave via treasury.aaveBorrow, maintaining liquidity even during high redemption demand.

Since the authorized SERVICE_ROLE that updates the USR Proof-of-Reserves (PoR) oracle based on the broad reserve holdings also executes redemptions, we can reasonably assume that in an adverse scenario where the system becomes undercollateralized, redemptions will reflect the most up-to-date price rather than the price at the time of the request. This ensures that redemptions are always executed at the latest available valuation, mitigating risks associated with outdated pricing.

Redemption Limits

To minimize excessive redemptions occurring within a short timeframe, there exists an associated redemptionLimit, currently set to 1M, which ensures that redemptions stay within a daily cap while automatically resetting usage at the start of a new period. Before processing a redemption, the contract checks if block.timestamp has exceeded lastResetTime + 1 days. If so, it calculates the number of days that have passed, updates lastResetTime, and resets currentRedemptionUsage to zero, effectively restarting the redemption limit.

RLP Redemptions

From a technical perspective, RLP redemptions largely operate in the same vein, with a few differences:

- The externally owned account (EOA) authorized with the

SERVICE_ROLEis responsible for managing the internal proof of reserves (PoR) for USR, along with overseeing the minting and redemption of both RLP and USR. However, rather than algorithmically deriving an exchange rate withinRlpPriceStorage, the operation adheres to a straightforward calculation immediately after invoking thesetReservesfunction on the USR PoR:

This ensures a direct and transparent determination of value within the system. - RLP price updates generally occur once a day, with an enshrined lowerBoundPercentage of 45 bps and upperBoundPercentage of 50 bps. In an adverse scenario, it is expected that burn requests will be executed following the updated oracle price after the aggregation and quantification of relevant reserves once a day, as otherwise, frontrunning of the system can potentially occur. RLP redemptions are thus executed at a slightly slower clip than that of USR, with a weighted average time to redemption execution of 2.9 hours.

- Redemptions of RLP are credited from the same Protocol treasury, with the withdrawal token being USDC or USDT. As expressed beforehand, this results in the protocol’s collateralization ratio scaling downward.

Exchange Insolvency Risks

Much like Ethena, Resolv leverages custodians’ solutions and their off-exchange settlement options effectively insulate Resolv and USR from exchange insolvency risks and prevents a situation such as the FTX collapse from significantly affecting USR backing.

USR’s collateral backing is safeguarded by two custodians: Ceffu and Fireblocks. These custodians are explicitly detailed in backing attestations, offering transparency about the distribution and management of assets. Both Ceffu and Fireblocks offer off-exchange settlement capabilities, which mitigate USR’s exposure to exchange-related risks. Under this model, Resolv’s backing assets remain stored in custodian-managed wallets and are not used as collateral on exchanges. Instead, centralized exchange accounts for Resolv are credited with virtual balances that mirror the custodian holdings. These virtual balances, being used to perform the ETH short hedges, allow for daily reconciliation and settlement of positions, significantly reducing the net exposure to exchange solvency and limiting it to the daily profit/loss from the short hedges. Ceffu primarily facilitates Binance-related settlement, while Fireblocks handles interactions with other centralized exchanges such as Deribit. Furthermore, off-exchange settlement enables the instant delegation of assets, significantly reducing the risk of liquidation of the ETH hedges during periods of heightened market volatility.

While off-exchange settlement mitigates the risk posed by an exchange failure, this risk is not eliminated. Given the daily settlement of balances, Resolv maintains risk exposure to the daily profits/losses from the short positions. In the case of an exchange failure, we expect the value of ETH to drop as a reaction to the news; the profit on hedges would likely be lost.

An associated duration risk is present and quantified as the time between the exchange failure and the return of funds from Ceffu’s custody to Resolv (Copper users’ funds were wholly available within days of Coinflex’s exchange failure). With the additional minimum 10% collateralization buffer stemming from RLP, there exists a significant insulation of reserves to significantly minimize any relative shortfall from Binance exchange failure.

Aave would only incur bad debt in the event of large price declines in ETH between the time of exchange failure and the custodied assets being released from custody. As the loss from this event is exclusively derived from the accumulated hedge profits stuck within the failed exchange, the value of the assets held by Ceffu during this time can decrease as much as the delta between the bad debt threshold of 1/(1+LB) and the LTV of the position with the minimum health score, coupled with the additional reserves from RLP safeguarding the system, before Aave accrues any bad debt. Below, we plot the expected USR price with respect to (ETH) collateral price movements during an exchange failure and under the worst-case assumption that the collateralization ratio starts at its minimum of 110%. The protocol maintains a significant collateralization buffer that insulates the protocol in extreme scenarios as such, with the ability to sustain a 20% ETH price drop in such an extreme scenario without affecting USR backing whatsoever.

Finally, despite their high-security standards, including MPC signing and use of safely stored cold wallets, custodians remain susceptible to hacks, which could compromise USR’s backing assets. To mitigate the risk of custodian hacks or collusion, Ceffu provides additional monetary insurance on their custodied assets. The combined insurance policy value between the two major providers equals $1B.

Hyperliquid

A portion of the collateral and hedge position is allocated on the Hyperliquid perpetual exchange platform, currently valued at $93.20 million. These funds face potential exposure to bridge-related tampering risks. The platform employs a layered security system, requiring consensus from two separate groups of just two out of four validators to authorize bridge transactions. However, this risk could be mitigated in the future with the adoption of native stablecoins as Hyperliquid collateral, reducing reliance on external bridging mechanisms.

Source: L2Beat

On-chain Liquidity

Since December, USR’s liquidity has experienced steady growth, reaching $60 million. The majority of this liquidity is allocated to a Curve stableswap pool, where $11M in USR is paired with $16M in GHO. Additionally, USR liquidity is distributed across several other pools, including $13M in a USR/USDC pool, $11M in a USR/DOLA pool, and $12M in a USR/RLP pool.

USR has demonstrated a strong peg relative to USDC, consistently remaining within a 5 bps range.

Parameter Recommendations

Liquidation Threshold and Bonus

The asset’s strong peg, coupled with robust collateralization mechanisms in place, indicates that it would be appropriate to list with a high LT. However, some factors lead us to recommend slightly more conservative measures: the asset has not demonstrated its peg through a bear market with sustained low or negative funding rates; a points program is partially driving the asset’s growth, and supply could contract following TGE; a high degree of complexity in the protocol means that there are many points of failure that could lead to partial shortfalls. Taking these factors in mind, we recommend listing the asset with a 78% LT and 6% LB.

We do, however, recommend creating a stablecoin emode configuration to enable capital-efficient looping capabilities.

Supply Cap

Per the on-chain distribution of USR liquidity, we recommend listing with an initial supply cap of $50M.

USR Borrowability

We do not recommend enabling USR as borrowable given the atomicity presented with stUSR staking, thereby enabling arbitrage opportunities that effectively siphon a relative share of yield away from stUSR stakers, preliminarily uncovering such information that stUSR will not rebase negatively. Such a phenomenon was akin to the rationale behind not enabling stETH as a debt asset on Aave V2. This behavior is currently occurring within Euler’s eUSR-1 vault, whereby an arbitrageur borrows as much USR as he can just before the staking yield distribution at 12:05pm UTC, receives his share of the yield, then withdraws his stUSR for USR and repays his debt at minimal cost. With a hypothetical market size otherwise theoretically enabling many millions of borrowable liquidity availability on Aave, before enabling borrowing, we recommend the implementation of some sort of duration-based withdrawal buffer or yield distribution at a higher frequency than that of once a day, to minimize this attack vector through requiring significant interest to be paid to uphold such a position.

Oracle Implementation

We recommend utilizing the USR Proof-of-Reserves oracle, through its AggregatorV3Interface, maintained and integrated within Resolv’s dedicated infrastructure for key functions such as crediting redemptions, as the primary oracle within Aave, as covered extensively above.

Specification

We have aligned with @LlamaRisk on the following parameter specification:

| Parameter | Value |

|---|---|

| Isolation Mode | No |

| Borrowable | No |

| Collateral Enabled | Yes |

| Supply Cap | 50,000,000 |

| Borrow Cap | - |

| Debt Ceiling | - |

| LTV | 73% |

| LT | 78% |

| Liquidation Bonus | 6% |

| Liquidation Protocol Fee | 10% |

| Variable Base | - |

| Variable Slope1 | - |

| Variable Slope2 | - |

| Uoptimal | - |

| Reserve Factor | - |

USR Stablecoins Emode

| Parameter | Value | Value | Value | Value |

|---|---|---|---|---|

| Asset | USR | USDC | USDT | GHO |

| Collateral | Yes | No | No | No |

| Borrowable | No | Yes | Yes | Yes |

| LTV | 90.00% | - | - | - |

| LT | 92.00% | - | - | - |

| Liquidation Penalty | 2.00% | - | - | - |

Disclaimer

Chaos Labs has not been compensated by any third party for publishing this ARFC.

Copyright

Copyright and related rights waived via CC0