title: [ARC] BAL Interest Rate Curve Upgrade

Author: @Llamaxyz @MatthewGraham @scottincrypto

Dated: 2022-10-29

Simple Summary

@Llamaxyz presents a proposal to amend BAL interest rate parameters and enable borrowing of BAL on the Aave Ethereum v2 Liquidity Pool.

Abstract

There is currently a high demand for borrowing BAL (interest rate = 19.9%), but the pool has poor capital efficiency with the utilization of the Reserve (47.0%), being near the Optimal point of 45%, [1].

By changing the interest rate curve and enabling borrowing, this proposal is expected to improve capital efficiency of the Reserve, generate more revenue for the DAO and significantly reduce the amount of free BAL in the Reserve.

Due to the ongoing incentives offered by Aura Finance, any increase in deposits is expected to be borrowed due to the high demand for BAL. Users are able to borrow and deposit BAL into Aura Finance’s staking contract to earn a yield of around 60% at the time of writing, [2]. This creates an arbitrage opportunity of 41% taking into account the liquidation risk, auraBAL pag and Aura Smart Contract risk.

Motivation

Users are expected to continue borrowing BAL to earn yield whilst interest rates permit and, in doing so, will create ongoing borrowing demand for BAL. Changing the interest rate curve by amending the Uoptimal parameter from 45% to 80% will improve the capital efficiency of the Reserve by enabling a greater portion of the BAL to be borrowed at the Optimal point than currently offered.

The chart below shows the 6 month historical BAL interest rate. The interest rate at the current Optimal point is 7%, which is low relative to current demand of 19.9%. This proposal recommends increasing the interest rate (slope 1 parameter) to 14% which is a 100% increase to the existing rate. Over time, we will be able to monitor the Reserve and amend the slope 1 parameter in an attempt to keep the utilization beneath the Optimal point for the majority of the time.

In addition, this proposal introduces a base rate of 2% and changes slope 2 from 300 to 150. This means at 0% utilization, the interest rate for borrowers is 2% and the gradient post-Optimal point is reduced, resulting in a less volatile interest rate for users with increasing utilization. The result will be a BAL interest rate similar to the SNX interest rate curve which has a base 3%, slope 1 12% and slope 2 100%.

The graphic below shows the changes in the interest rate.

Utilization of the liquidity in the Reserve is expected to increase from 45% → 73.33% assuming users pay an interest rate of 13%, which is less than the current borrowing rate of 19.9%. With a borrowing cost of 14% at the Optimal point, depositing BAL into Aura Finance’s auraBAL staking contract or B-80BAL-20wETH / auraBAL gauge will remain lucrative for users.

Assuming the BAL Reserve remains at $3.62M, the revenue generated at the Optimal point for the DAO will increase from $20.8k to $75.3k, or 230%. The Reserve utilization increases from 45% to 80%, which reduces the amount of unused BAL by 63.6%. This will provide a significant increase in capital efficiency and reduce the unutilized BAL to $724k.

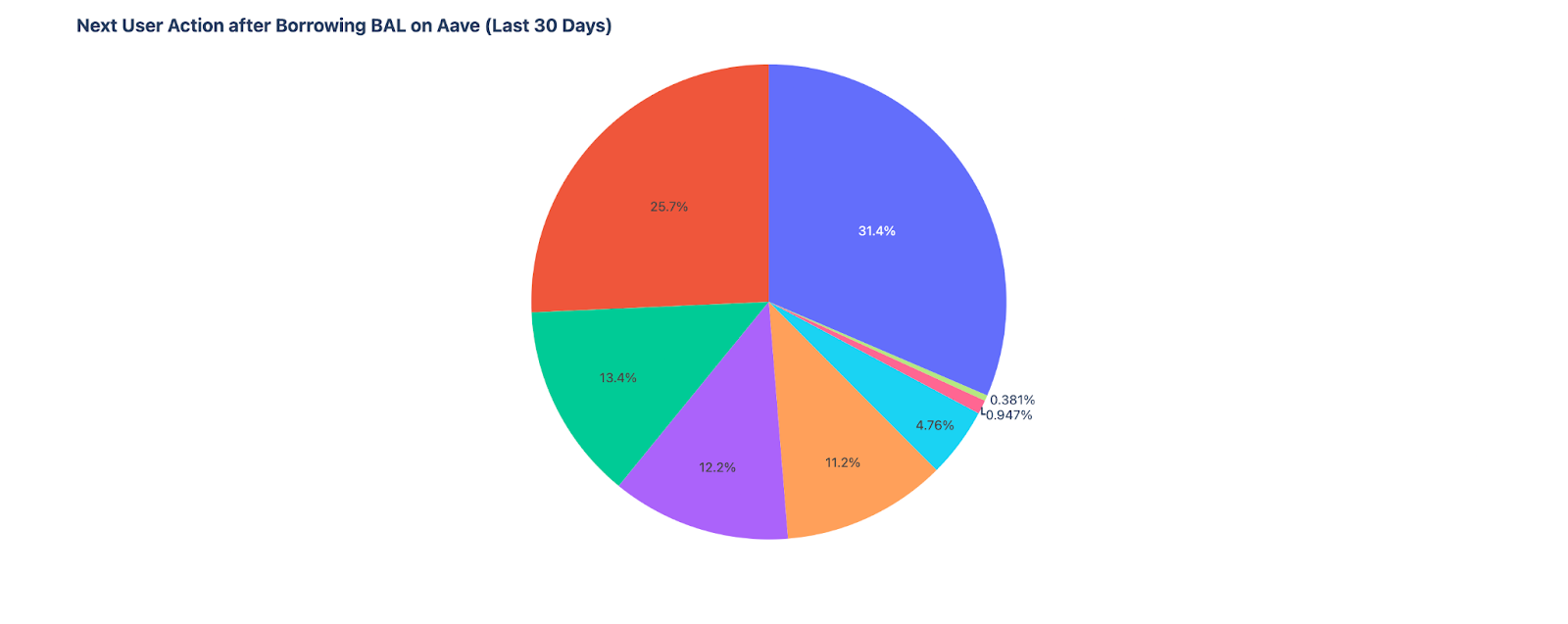

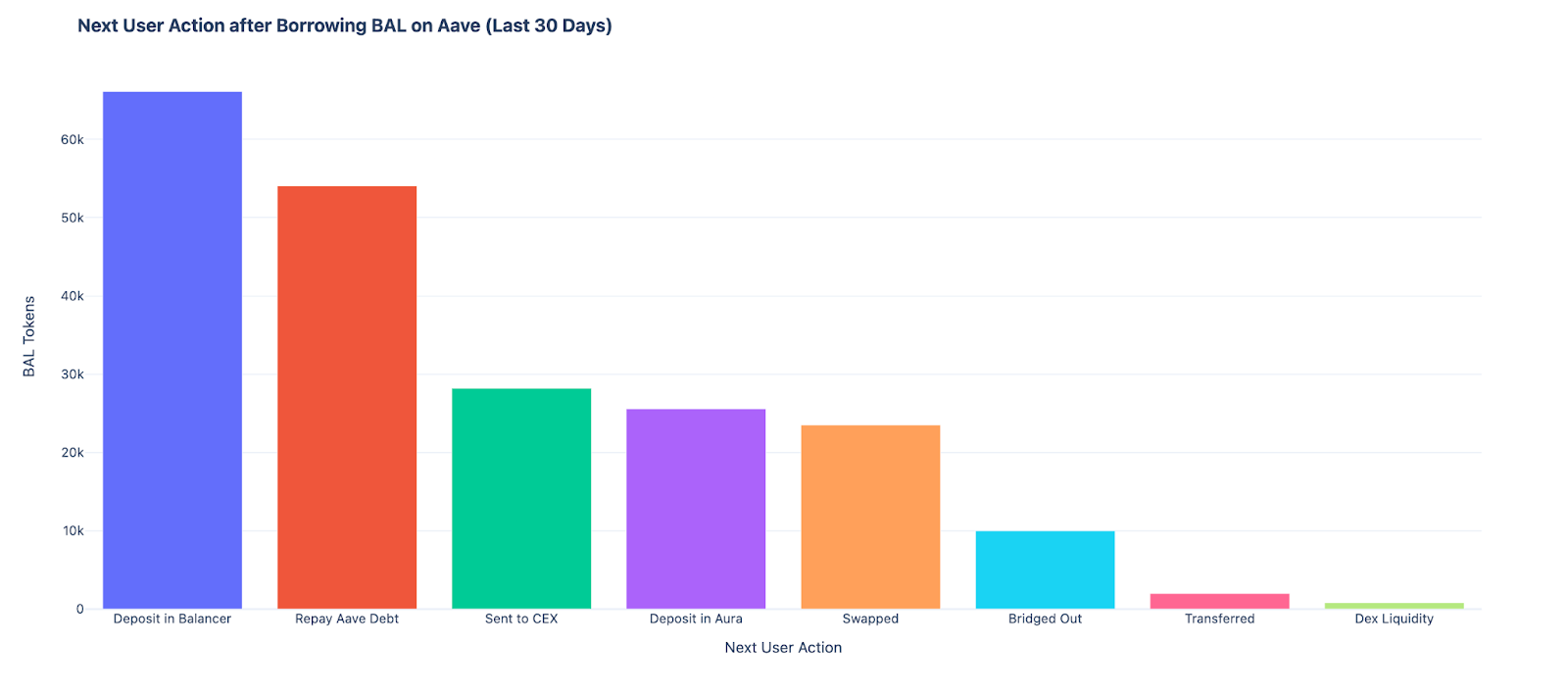

In order to enable users to access the BAL in the Reserve and realize the improved capital efficiency, borrowing is to be enabled. The high borrowing demand is due to users depositing BAL into Aura Finances contracts that then supply liquidity to the B-80BAL-WETH pool or depositing directly in Balancer pools, [3]. During the last 7 days of October, 100% of the borrowed BAL was deposited into Aura Finance.

The improved capital efficiency of the BAL Reserve is expected to lead to an increase in BAL liquidity on-chain. The more on-chain liquidity there is, the more expensive it is to manipulate an oracle feed.

Specification

The below table shows the current and proposed changes to the BAL Reserve.

| Parameter | Current (%) | Proposed (%) |

|---|---|---|

| Uoptimal | 45 | 80 |

| Base | 0 | 2 |

| Slope1 | 7 | 14 |

| Slope2 | 300 | 150 |

| Reserve Factor | 20 | 20 |

| Borrowing | Disabled | Enabled |

References

[1] Aave - Open Source Liquidity Protocol

[2] https://app.aura.finance/

[3] Balancer: B-80BAL-20WETH Token | Address: 0x5c6ee304...820db8f56 | Etherscan

[4] Deed - CC0 1.0 Universal - Creative Commons

Copyright

Copyright and related rights waived via CC0, [4].