title: [ARFC] Increase Optimal Borrow Rates for Ethereum Stablecoin Markets

author: @monet-supply - Block Analitica

created: 2023-10-11

Summary

This ARFC proposes to make adjustments to stablecoin interest rate models across Aave v2 and v3 Ethereum markets.

Motivation

Over the past several months, equilibrium stablecoin borrowing costs across the broader defi space have trended upwards, and may now be higher than the governance defined “optimal borrow rate” set within Aave’s stablecoin interest rate models. For example, Maker borrow and supply (DSR) rates have been mostly over 5% since mid August. Rates in tradfi have also risen significantly, with short term treasury bills yielding around 5.5% and even long term treasury rates rising to nearly 5% across various maturities.

This mismatch between Aave’s rate models and the broader market leads to a range of potential inefficiencies, including deadweight loss from the cost of liquidity being artificially constrained away from equilibrium value, and negative UX impact due to greater rate volatility when utilization is above the optimal ratio.

First, we present data backing up the assertion that Aave’s current stablecoin rate models are not finding efficient market equilibriums. Then, we discuss the negative impacts of this including deadweight loss and UX impacts. Finally, we present a plan of adjustment that we estimate will address the market inefficiencies and lead to improved market utility across borrowers, suppliers, and the community of AAVE token holders.

UX Impacts

We gathered block by block interest rate data for the largest stablecoin markets across v2 and v3 (USDC, USDT, and DAI) from 1 August to 7 October, block numbers 17816255 to 18300344. Raw data can be downloaded here.

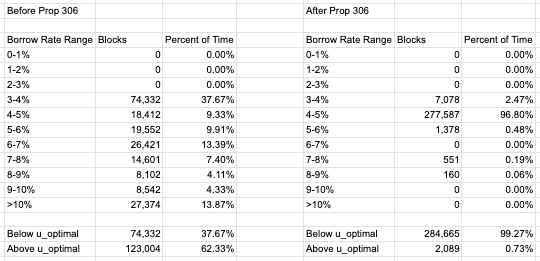

In the middle of this period (28 August), Aave governance executed proposal 306, which added sDAI as collateral on v3 while increasing the slope1 parameter for DAI to 5% on both v2 and v3. This offers useful data to A/B test the premise of whether increasing the borrow rate at optimal utilization can help improve market functioning.

Reviewing data for the Aave v3 DAI market, we can see that the increase in slope1 was strikingly effective at reducing borrow rate volatility, with the percent of time utilization was above optimal point falling from 62% to below 1%. There were some confounding factors, such as market turbulence over CRV leveraged positions at the beginning of August, and Maker’s elevated 8% DSR rate effective from 4 August to 18 August. But we can see heightened rate volatility from utilization exceeding the optimal ratio persists even excluding these periods.

Source: Stablecoins ARFC Market Data

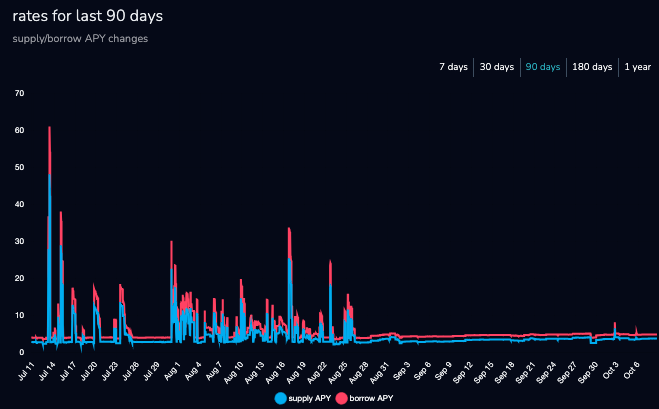

Source: Block Analitica Aave Dashboard (DAI v3)

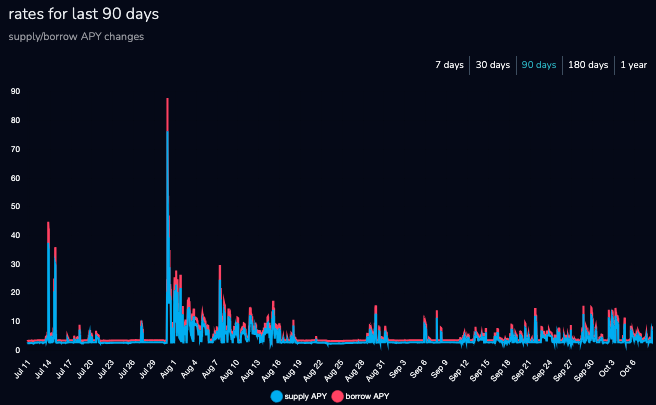

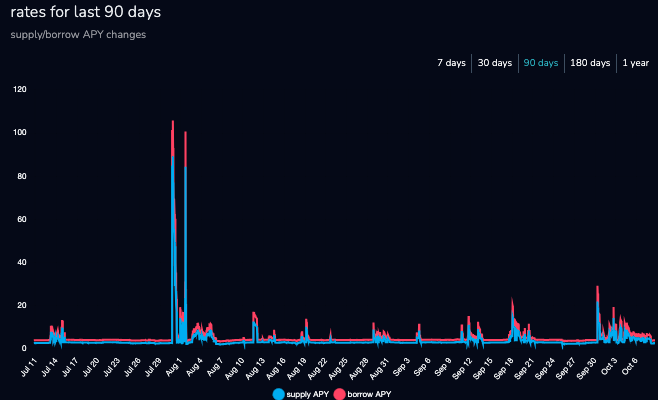

Comparing this with historical rates data for Ethereum v3 USDC and USDT markets (shown below), we can see a significant reduction in borrow rate volatility from the increase in the slope1 parameter. Note that the USDC market seems to exhibit higher volatility because it has a slope1 parameter of 3.5%, vs 4% for the USDT market.

Source: Block Analitica Aave Dashboard (USDC v3)

Source: Block Analitica Aave Dashboard (USDT v3)

We can expect reduced rate volatility to drive an increase in borrower participation. Paradoxically, raising the slope1 parameter for the DAI markets also seems to have been associated with a reduction in average (geometric mean) borrowing rates; for example, the average v3 DAI borrow cost from 1 August to 28 August (when proposal 306 was executed) was 6.49%, while the average rate from 28 August to 7 October was 4.56%.

Looking at the USDC v3 market over the same 28 August to 7 September period, we see the average (geometric mean) borrowing rates were 4.52%, so similar to DAI after the adjustment to interest rate models but with much higher volatility. This supports the notion that raising slope1 can bring greater rate stability without negatively impacting borrower welfare.

Deadweight Loss

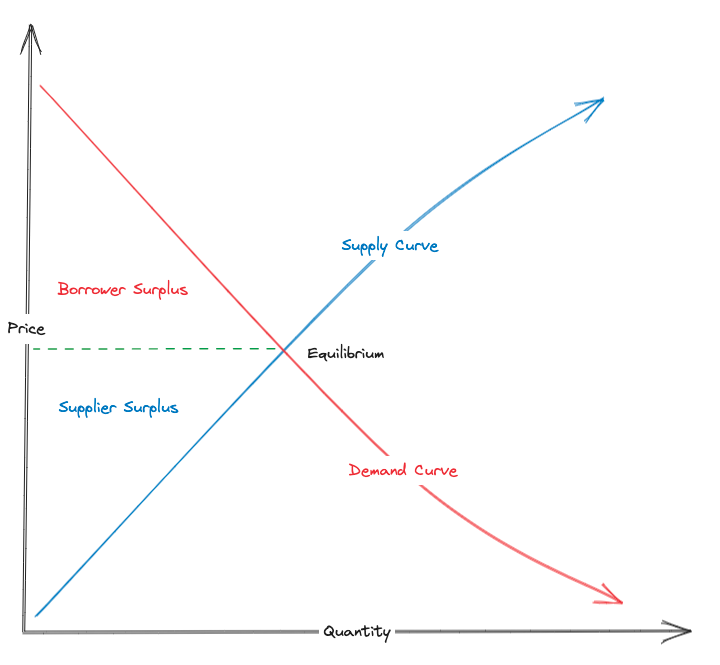

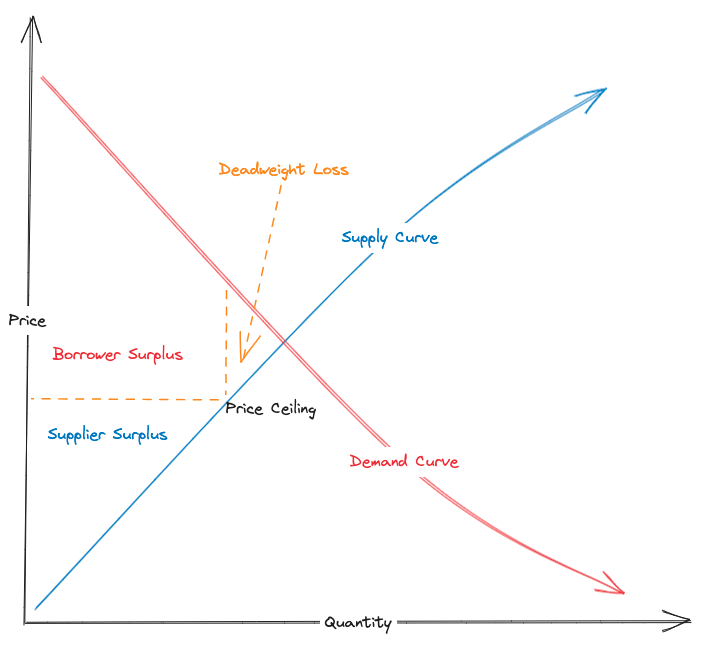

Deadweight loss is an economic concept that describes the loss of total utility created by a market when prices are artificially constrained either above or below the optimal equilibrium where supply and demand are in balance.

It is commonly demonstrated with graphs of the supply and demand curve; any quantities exchanged below borrowers’ (consumers’) marginal willingness to pay represents consumer surplus, while quantities exchanged over suppliers’ (producers’) marginal willingness to produce represents producer surplus, and together these represent the markets overall utility.

When prices are artificially constrained above or below the market equilibrium, this leads to a lower quantity of goods exchanged, which reduces the total area of consumer and producer surplus and creates an area on the graph showing reduced utility known as deadweight loss.

With borrowing rates at optimal utilization falling below broader market levels, this can have the unintentional effect of constraining price below equilibrium value, which reduces overall utility of the Aave stablecoin markets. This has a likelihood to constrain market size growth over the medium term as suppliers are insufficiently incentivized to deposit more capital, while borrowers have a very low amount of liquidity available at reasonable prices before pushing the utilization above the optimal point and potentially pushing rates far above the market equilibrium.

Proposed Adjustments

We propose an adjustment to the variable slope1 parameter for stablecoins across Aave v2 and v3 Ethereum markets to better align optimal utilization rates with the broader market. Specifically, we proposed to increase variable slope1 parameters to 5% for each of the following assets: USDC, USDT, FRAX, sUSD, LUSD, GUSD, and USDP. No changes are proposed for DAI as it already uses 5% variable slope1 across both v2 and v3 Ethereum markets.

This will result in borrowing rates at optimal utilization still being equal or slightly below most other defi options (eg. Maker and Spark rates), while significantly increasing supply rates. Increasing the expected supply rates for stablecoins on Aave v3 Ethereum market may lead to a bit more downward price pressure on GHO, but this is not expected to be material considering that users can already borrow GHO with sDAI collateral (at 5% collateral yield, likely higher than the average for other stablecoin markets after this change) and Aave governance is also considering additional measures to support the GHO peg.

Specification

Ethereum v2 Market Changes

- Increase USDC slope1 parameter to 5%

- Increase USDT slope1 parameter to 5%

- Increase FRAX slope1 parameter to 5%

- Increase LUSD slope1 parameter to 5%

- Increase sUSD slope1 parameter to 5%

- Increase USDP slope1 parameter to 5%

- Increase GUSD slope1 parameter to 5%

Ethereum v3 Market Changes

- Increase USDC slope1 parameter to 5%

- Increase USDT slope1 parameter to 5%

- Increase FRAX slope1 parameter to 5%

- Increase LUSD slope1 parameter to 5%

Disclaimer

Block Analitica is not presenting this ARFC on behalf of any third party and is not compensated for creating this ARFC.

This proposal is presented on an “as is” basis and without warranty of any kind. This is not intended or offered as financial, investment, regulatory, or tax advice. Any assets or protocols referenced are mentioned purely for illustrative purposes, and this is not a recommendation or solicitation to engage with any asset or protocol.

Next Steps

- Gather community feedback on this ARFC.

- If community consensus is reached, escalate this proposal to the Snapshot ARFC stage.

- If the Snapshot outcome is YAE, escalate this proposal to AIP stage.

Copyright

Copyright and related rights waived via cc0.