Chaos Labs supports enabling PYUSD as collateral on the Aave V3 Ethereum Core instance. This change does not pose additional risks to the protocol.

Motivation

While this represents a reversal of our prior recommendation to disable PYUSD’s collateral status, made during an earlier optimization proposal, we support this change following discussion with Aave Growth Service Providers. The change stems from the launch of the PayPal incentive program, which ultimately has become contingent on the asset’s collateral status.

The asset was previously enabled as collateral; therefore, this update does not introduce a new risk type but reinstates an already evaluated configuration. Additionally, the DEX liquidity for PYUSD has exponentially improved following the launch of incentive programs and, as such, mitigates some of the concerns raised in the prior post. PayPool and Spark PYUSD Reserve Curve stableswap pools have scaled to as much as $29M and $100M TVL, respectively, in just a few days.

Given the unchanged risk profile and improved liquidity conditions, we believe re-enabling PYUSD as collateral will allow Aave to capture demand driven by the upcoming incentive phase without introducing new systemic exposure.

Specifications

We recommend restoring the previous collateral configuration

Parameter

Current Value

Proposed Value

LTV

0%

75%

Next Steps

We will move forward and implement the supply and borrow cap updates via the Risk Steward process.

Disclosure

Chaos Labs has not been compensated by any third party for publishing this recommendation.

LlamaRisk supports enabling PYUSD as collateral on Aave V3 Core with an LTV of 75%. However, we observe a notable concentration of DEX liquidity, with the majority of PYUSD liquidity in the leading Curve pool bootstrapped within the past 20 days and entirely supplied by Spark through its Spark Liquidity Layer. This allocation may not be sustained once the incentive program concludes. Therefore, we recommend closely monitoring the pool’s liquidity dynamics before considering any further cap adjustments.

Market Risk

As of October 11, 2025, PayPal USD (PYUSD) has a total supply of 1.92B on Ethereum. The majority of this supply is concentrated among two centralized entities, Paxos Hot Wallet, holding 36.74%, and Copper: Ethena Custody, holding 31.42%. This distribution pattern highlights a high degree of custodial control and suggests that PYUSD is primarily being utilized as collateral for the issuance of some other asset.

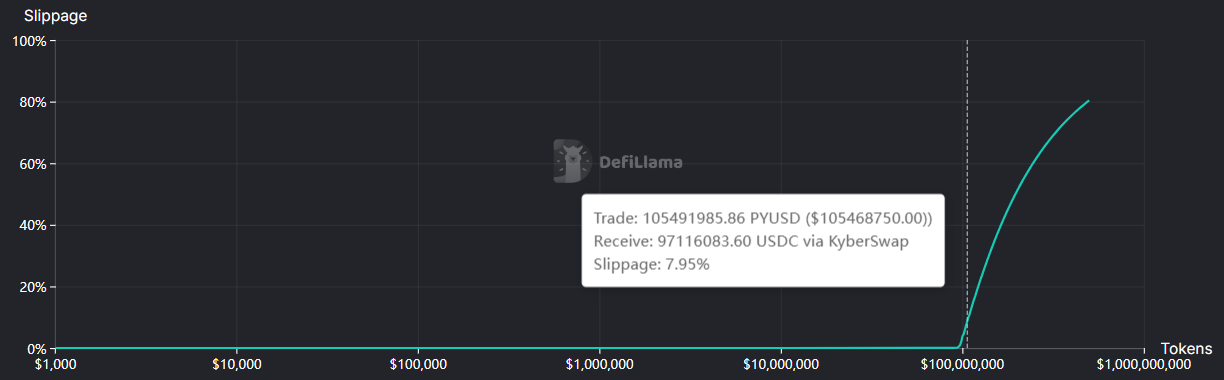

Source: pyUSD/USDC Swap Liquidity, DeFiLlama, October 11, 2025

Users can swap up to approximately $105 M worth of PYUSD for USDC within a 7.5% price impact. This capacity has increased notably following the rise in DEX liquidity after the launch of PayPal’s incentive program. Most of PYUSD’s liquidity is concentrated in its top two pools: Curve pyUSD/USDS ($98.7 M) and Curve pyUSD/USDC ($30.93 M).

Source: pyUSD DEX Pairs on Ethereum, GeckoTerminal, October 11, 2025

The DEX liquidity for PYUSD is highly concentrated across these pools, particularly in the Spark PYUSD Reserve on Curve. The breakdown is as follows:

Curve pyUSD/USDS ($98.7M TVL): A recently launched pool on Curve that is part of the Spark Liquidity Layer (SLL). Its entire liquidity has been bootstrapped over the past 20 days and is exclusively supplied by Spark.fi’s ALM Proxy. Since this pool accounts for the majority of PYUSD’s DEX liquidity, it remains uncertain whether the SLL allocation will persist once the PayPal incentives end. It is therefore advisable to closely monitor liquidity levels in this pool and avoid further cap increases if liquidity declines.

Curve pyUSD/USDC ($30.93M TVL): 32.3% of this pool’s liquidity is supplied by a single EOA.

Disclaimer

This review was independently prepared by LlamaRisk, a DeFi risk service provider funded in part by the Aave DAO. LlamaRisk is not directly affiliated with the protocol(s) reviewed in this assessment and did not receive any compensation from the protocol(s) or their affiliated entities for this work.

The information provided should not be construed as legal, financial, tax, or professional advice.