This week, Horizon’s TVL increased to $628.3m, with over $209.8m in net borrows and $340.7m in stablecoin supply.

Highlights

- TVL has increased to $628 million, with a total stablecoin supply of $341 million and net borrowings standing at $210 million. RLUSD and USCC remain the dominant supplied assets, driven mainly by previously opened positions and ongoing incentive programs.

- The incentive programs for RLUSD supply and USDC borrow markets continue to be active, albeit with a capped APR of 4.5% for RLUSD after the renewal.

Incentivize Program

Incentive programs on Horizon stimulate liquidity supply and borrowing activity, with active campaigns for USDC and RLUSD.

- USDC: The borrowing campaign remains active, offering daily rewards of $2,956, which effectively reduces the borrowing cost by approximately 3.5%.

- RLUSD: The new lending-focused campaign has began, distributing $24,104 in daily rewards, capped at a 4.5% APR.

Utilization Report

In the nineteen weeks following Horizon’s market activation, the total borrowed amount increased to $209.8m, driven by the opening of new USDC and RLUSD borrowing positions with USCC as the primary collateral asset.

Source: LlamaRisk, January 9, 2026

Parameter changes during this period

- RLUSD: The supply cap was raised to 216.5m on 6 January and then again to 221.5m on 7 January, immediately filled by large suppliers.

Supply (stablecoins)

The total stablecoin supply on Horizon increased by 9.8% to $340.7m, growth driven by a rise in the supply of both RLUSD and USDC. This Growth followed a 2x increase in the RLUSD supply cap.

- RLUSD: The supply increased by 10% from $201.5m to $221.5m.

- USDC: The supply increased by 20.3% from $33m to $39.7m.

- GHO: The supply hasn’t changed and currently stands at $79.5m, managed by the GHO Steward.

Source: LlamaRisk, January 9, 2026

Supply (RWAs)

The total supply of RWAs increased by 7.9%, holding $2876 million. The increase in supply was driven solely by the expansion of USCC positions, while supply across other assets was broadly unchanged to modestly lower.

The changes in individual RWA supplies were as follows:

- USCC: Supply decreased by 9.5%, from $266.3m to $278.5m.

- JTRSY: Supply remained at zero with no assets supplied.

- USTB: Supply hasn’t changed and currently stands at $392.5k.

- JAAA: Supply hasn’t changed and currently sits at $2.5m.

- USYC: Supply remained at zero with no assets supplied.

- VBILL: Supply decreased by 2.3%, from $6.4M to $6.25M

Source: LlamaRisk, January 9, 2026

Borrow

Total net borrowing on Horizon increased by 5.6% to $209.8m, driven by new demand for borrowing USDC and RLUSD stablecoins.

- USDC: Net borrows increased by 18.8%, from $26.1m to $31m.

- RLUSD: Net borrows increased by 5.7%, from $126.3m to $133.5m.

- GHO: Net borrows haven’t changed and currently sit at $45.3m.

Source: LlamaRisk, January 9, 2026

Stablecoin Utilization

This week, GHO utilization remained flat, while USDC and RLUSD experienced a slight decline over the period, primarily due to new stablecoin supply inflows.

Source: LlamaRisk, January 9, 2026

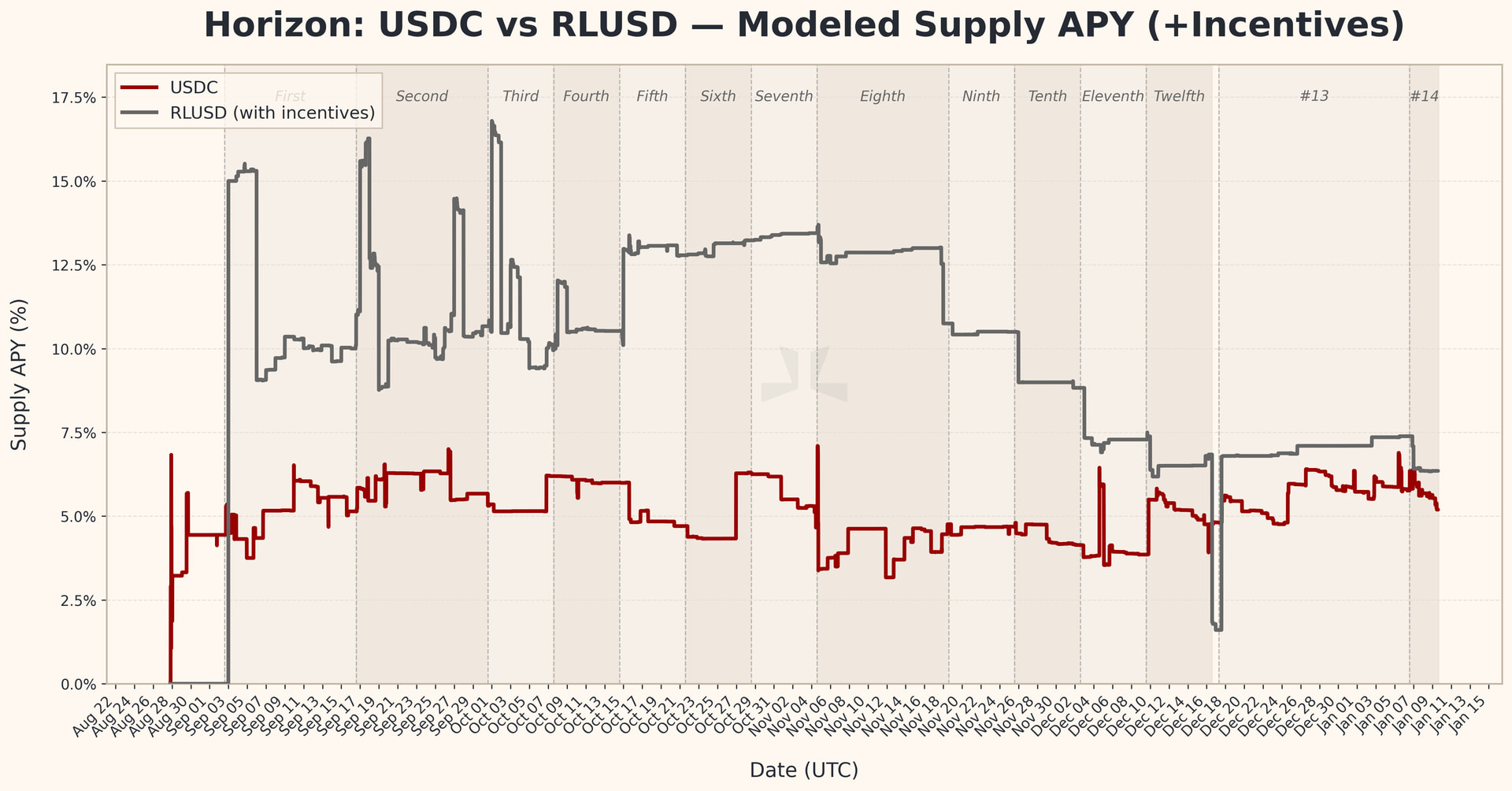

Stablecoin Supply Rates

The fourteenth incentive campaign is now live, with the RLUSD supply APY post-incentives being lower, reflecting reduced effective incentives. Overall rate conditions remain stable, with no material spillover observed in USDC markets.

Source: LlamaRisk, January 9, 2026

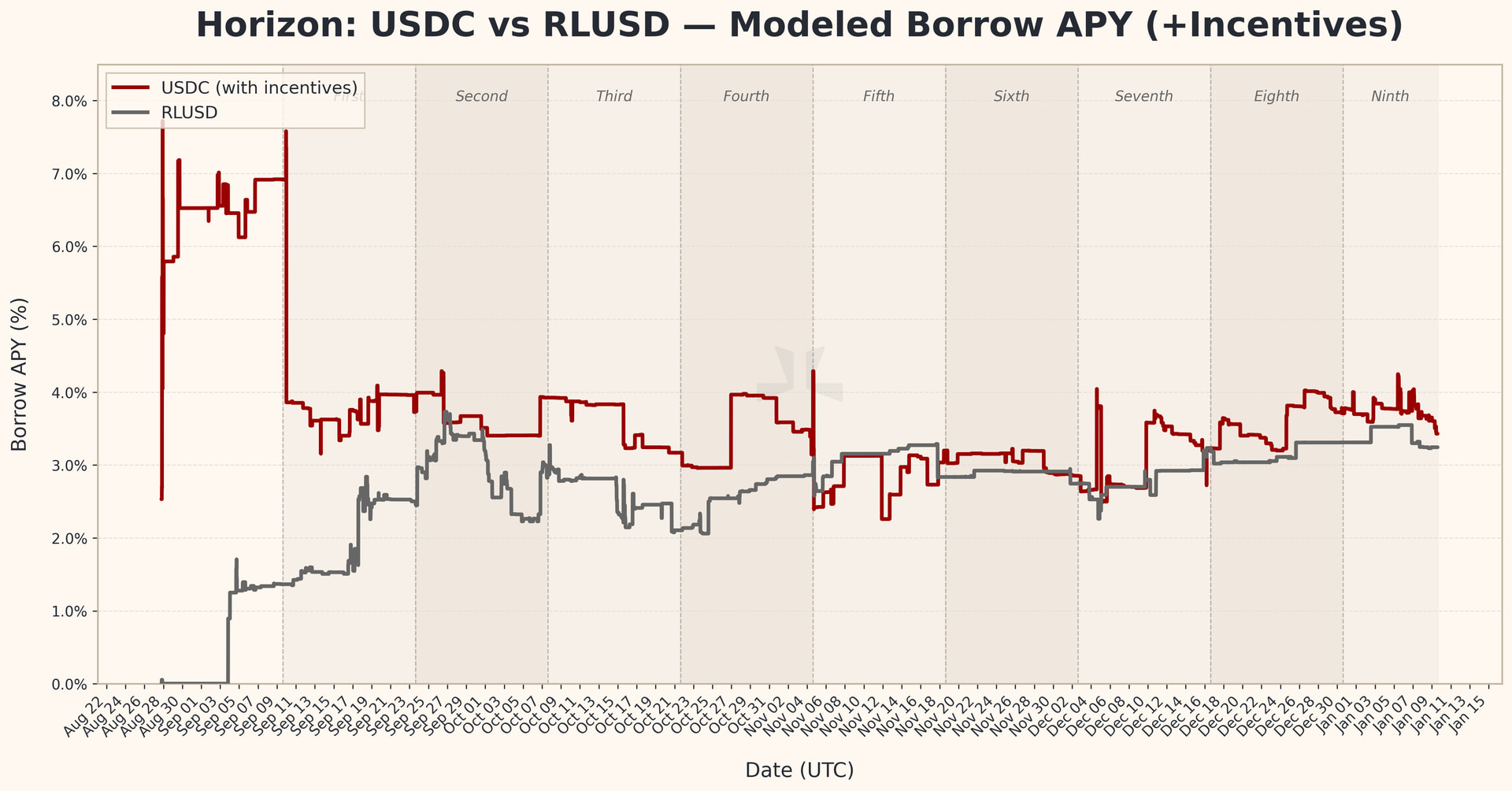

Stablecoin Borrow Rates

USDC and RLUSD borrowing rates held steady over the week, showing limited volatility and no meaningful trend, as additional stablecoin supply was matched with incremental borrows.

Source: LlamaRisk, January 9, 2026

Profitability heatmaps for leverage looping

USCC and USTB yields both declined over the period, with USCC falling to 4.4% and USTB slipping to 3.59%. Yields remain within a contained range, suggesting limited impact on the broader rate environment.

USCC

Source: LlamaRisk, January 9, 2026

Source: LlamaRisk, January 9, 2026

USTB

Source: LlamaRisk, January 9, 2026

Source: LlamaRisk, January 9, 2026