Overview

Following the publication of our two research papers, Stress Testing Ethena: A Quantitative Look at Protocol Stability and *Aave’s Growing Exposure to Ethena: Risk Implications Throughout the Growth and Contraction Cycles of USDe,* the integration between Ethena and Aave has deepened significantly.

Since the release of these papers, USDe-backed assets on Aave have continued to grow, and Ethena has deposited a larger share of its reserve assets into Aave. In response to this increased interdependency, we collaborated with the Ethena team to introduce a set of mitigation measures designed to safeguard both Aave and Ethena against potential market stress scenarios.

This paper outlines those new mitigation mechanisms and explains how they help ensure market stability.

Context

The integration between Ethena and Aave has continued to deepen both in terms of USDe-backed asset usage on Aave and the share of Ethena’s reserve assets deployed into the protocol.

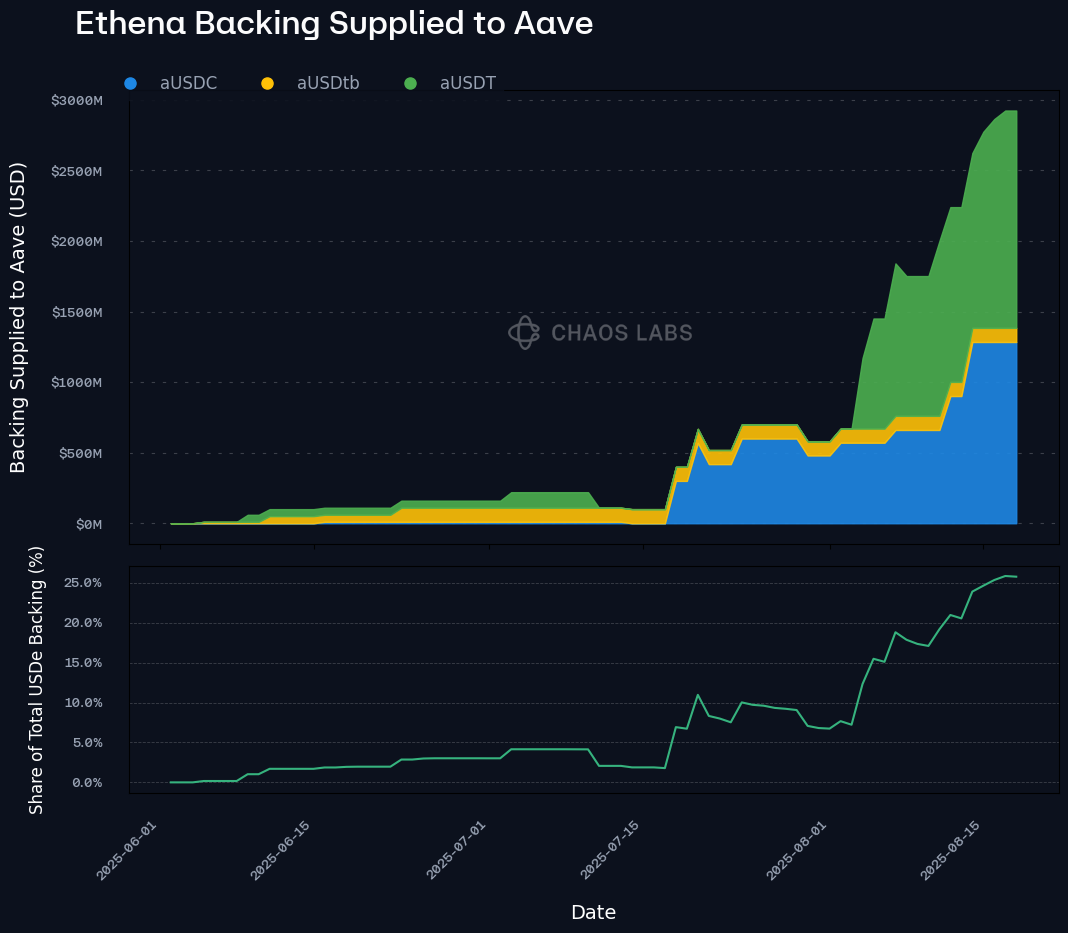

As shown in the chart below, the total supply of USDe-backed assets has grown significantly, reaching nearly $7 billion. In addition to this increase in absolute supply, the share of total USDe held on Aave has also risen steadily and now represents about 60% of circulating USDe.

Ethena has significantly increased the share of its stablecoin reserves deposited into Aave. Since early August, deposits of aUSDC and aUSDT have grown, with peak backing reaching approximately $3 billion. This translates to around 25% of Ethena’s total reserve backing now being deployed on Aave.

Crucially, this reserve deployment has a reflexive benefit: by supplying its stablecoin backing into Aave markets, Ethena directly helps lower borrow rates for those same stablecoins. This is particularly important because one of the primary limiting factors for USDe-backed leveraged looping strategies is the cost of borrowing. When borrow rates are elevated, the economics of looping into USDe via PTs becomes increasingly unattractive, slowing down growth in USDe supply. By contrast, when borrow costs are suppressed through deeper liquidity (enabled by Ethena’s own deposits), the conditions for scaling these strategies improve meaningfully. In effect, Ethena’s reserve deployment into Aave helps bootstrap the very leverage infrastructure it relies on.

This dynamic becomes even more critical during contraction phases. In such periods, it is in Ethena’s best interest to maintain low borrow rates in Aave’s stablecoin markets. If Ethena were to withdraw its reserves from Aave to meet redemptions, rather than sourcing liquidity from other stablecoin reserves or gradually unwinding perpetual positions, it could trigger a sharp spike in borrowing costs. This would significantly erode the profitability of USDe-based loops, leading to a faster unwinding of positions and further accelerating the contraction of USDe supply. By keeping borrow rates anchored through continued reserve deployment, Ethena can avoid self-reinforcing feedback loops and stabilize redemptions.

Mitigation Measures

Given the growing interdependence between Ethena and Aave, a coordinated approach to risk mitigation has become essential. In collaboration with the Ethena team, a series of safeguards have been implemented to ensure that this integration remains robust under both normal and stress conditions.

The following sections outline the key mitigation measures currently in place.

Redemption Priority

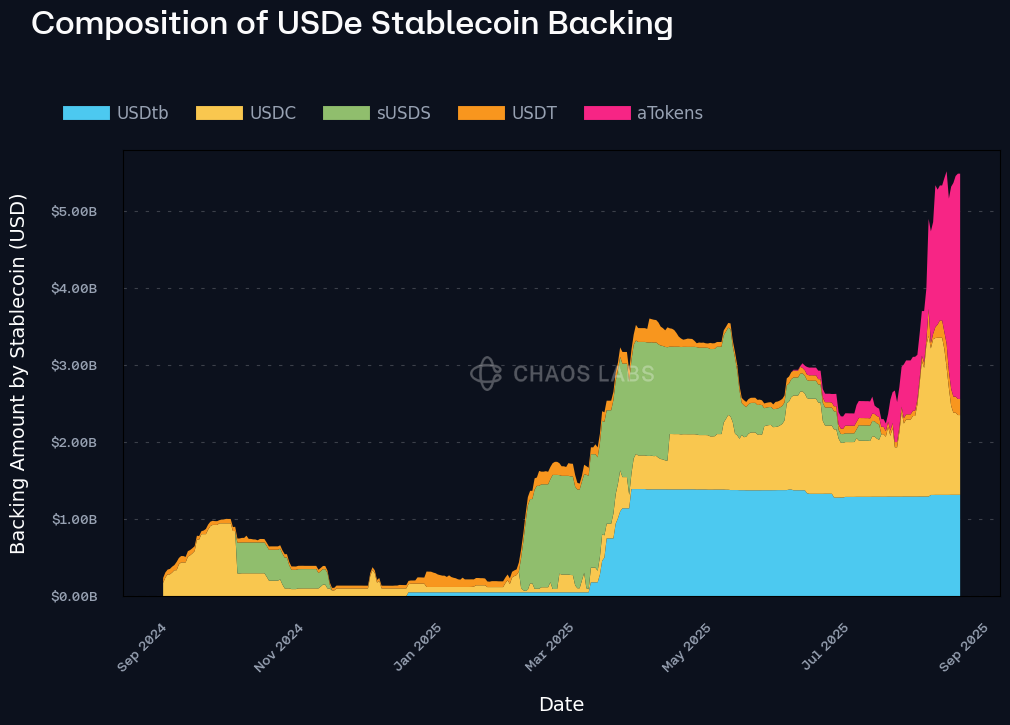

The composition of USDe’s stablecoin backing has shifted significantly over time, as shown in the chart below. Early in its lifecycle, USDe was primarily backed by USDC. Over the course of 2025, the makeup of its reserves evolved, particularly with the introduction of USDtb and aTokens. Currently, a sizable portion of the backing is held in USDtb, USDC on Coinbase, and aTokens on Aave, especially aUSDC and aUSDT.

While redemption behavior may vary depending on market conditions, Ethena has indicated a general preference for sourcing liquidity from on-chain stables such as USDT, USDC, and USDtb before turning to perpetual position unwinds. Withdrawals of aTokens from Aave are considered an even lower-priority option, reflecting the potential impact such actions could have on Aave’s stablecoin markets and, by extension, on the contraction of USDe supply.

The effective redemption ladder can be summarized as: Stablecoins → Perpetual unwinds → aTokens.

This prioritization ensures that aTokens are treated as the last capital to be touched during redemptions. This is a deliberate risk mitigation measure designed to prevent destabilizing Aave’s liquidity pools, where many USDe holders interact with USDe-backed looped positions.

While in some scenarios multiple redemption sources may be tapped concurrently, Ethena has expressed clear internal alignment around minimizing the impact of reserve withdrawals on Aave markets. This is particularly important given how closely Ethena’s leverage strategies depend on healthy borrowing conditions in Aave. Pulling stablecoin liquidity from Aave in times of stress would not only impair broader market functionality but could also accelerate unwinds in USDe-based loops, amplifying contraction pressures on USDe supply.

By positioning Aave-based liquidity as the “last capital standing”, Ethena reinforces systemic stability and protects both protocols from reflexive downside spirals during periods of high redemption demand or liquidity stress.

Aave as a Whitelisted Redeemer

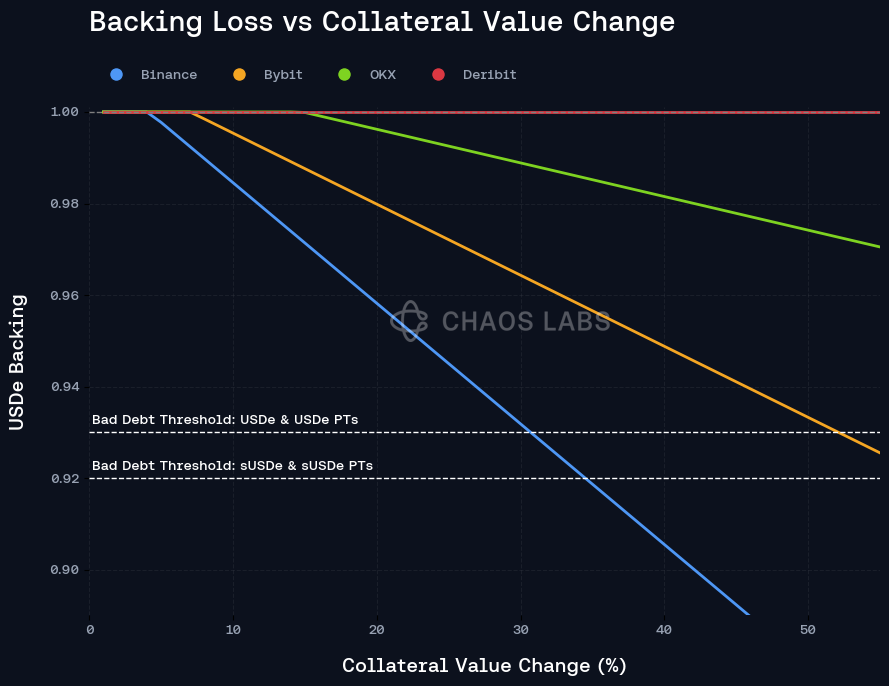

A core mitigation designed to strengthen the integration between Aave and Ethena is the establishment of Aave as a whitelisted redeemer within Ethena’s Mint and Redeem contracts. This mechanism is intended to prevent or significantly limit the accrual of bad debt on Aave in the event of a backing loss within USDe.

In practice, the design allows Aave to directly redeem underlying collateral from Ethena when USDe-backed positions approach or cross into undercollateralization. Because USDe is priced using the USDT oracle on Aave, a backing loss in USDe would not be reflected unless the oracle is manually updated. Under such conditions, Aave would internalize liquidations and proceed to redeem the corresponding collateral directly from Ethena’s redemption contract.

By executing this process internally, Aave avoids relying on secondary markets where slippage, liquidity fragmentation, or price dislocation could amplify protocol losses. This creates a controlled unwind mechanism that limits systemic spillovers and protects Aave’s core markets from contagion risk.

We are working with BGD to design an optimal algorithmic solution that accounts for the characteristics of Ethena-related assets and their underlying properties. The goal is to ensure that redemption flows can be executed efficiently even under stressed conditions, where certain assets may exhibit limited liquidity or delayed convertibility. This requires accounting for factors such as the lifecycle of principal tokens, potential frictions around time-locked assets like sUSDe, and the availability of vanilla USDe for immediate redemption. The resulting framework aims to deliver predictable redemption outcomes, limit dependence on external markets, minimize capital requirements and associated duration risk, and safeguard Aave’s stability across diverse market conditions.

Conclusion

The interactions between Aave and Ethena have become one of the most significant protocol-to-protocol relationships in DeFi, with USDe-backed assets now accounting for a growing share of activity on Aave and Ethena increasingly relying on Aave for reserve deployment and USDe growth. This interdependency creates powerful benefits in terms of liquidity, capital efficiency, and scalability, but also introduces reflexive risks that must be carefully managed.

The mitigation measures detailed in this analysis, prioritizing on-chain stables and perpetual unwinds before tapping Aave liquidity for redemptions and designating Aave as a whitelisted redeemer, collectively strengthen the resilience of both protocols. These safeguards ensure that redemption flows remain functional under stress, borrowing conditions remain stable during contraction phases, and the risk of bad debt accumulation on Aave is materially reduced.

Importantly, we are continuing to collaborate closely with the Ethena team to explore additional safeguards and risk management frameworks. By embedding these systems and continuing to build jointly, Aave and Ethena are taking deliberate steps to align incentives and protect the integrity of both ecosystems. The result is a more robust and scalable integration — one that can absorb shocks, support USDe’s growth trajectory, and deepen the foundational infrastructure of DeFi.

Disclaimer

Chaos Labs has not been compensated by any third party for publishing this research paper. Our pre-launch risk reports on Ethena, published over a year ago, represented a temporary compensated engagement, bear no implications on the current state of the protocol and can be viewed here on our website. We additionally provide proof-of-reserve attestations for the Ethena Protocol, which periodically reflect the aggregate state of the portfolio relative to the underlying USDe shares emitted. This research paper was not created in collaboration with Ethena; however, we are grateful for the team’s thorough review.