Background:

Aave has grown from $0 to $5 billion+ in total liquidity in just over a year. This growth has impressively been achieved without any liquidity incentives.

In fall 2020, Aave V2 was launched on mainnet and the LEND token was migrated to the new AAVE token. 3MM of the 16MM AAVE token supply has been allocated to the Aave Ecosystem Reserve, managing the distribution of safety and ecosystem incentives. In September 2020, AIP-1 passed, kickstarting the Safety Module and distributing 400 AAVE per day to stakers. In January 2021, AIP-7 passed, activating AAVE slashing and increasing the safety incentives to 550 AAVE per day. 20% of the fully-diluted AAVE supply is currently staked.

As described in the Aavenomics paper, the Aave community can vote to distribute liquidity incentives from the Ecosystem Reserve.

Proposal:

The intent of this RFC is to open up the discussion among the community to explore a liquidity mining (LM) program that optimizes for the long term growth of Aave. We believe that a well designed LM program can accomplish the following (as discussed in more detail below):

- Grow lending and borrowing activity in targeted markets

- Further decentralize/expand the AAVE token holder base

- Incentivize v1 to v2 migration

- Increase long-term pools of capital via stkAAVE distribution

Below is a rough sketch of ideas to consider. We invite the community to comment and vote below on the general idea of a LM program.

Liquidity Mining Benefits:

Grow lending and borrowing activity: With almost every major DeFi protocol launching a liquidity mining program, we believe it would be advantageous for Aave to utilize part of the Ecosystem Reserve to drive lending and borrowing activity across markets. Distributing AAVE to borrowers and lenders acts as an added incentive to attract more capital. The distribution can become more targeted over time. For example, certain markets may need more AAVE than others based on liquidity, utilization, and maturity of the market.

Broader distribution and protocol decentralization: Rewarding AAVE to users of the protocol improves the distribution of the AAVE token. This gets AAVE into the hands of more users, further decentralizing the protocol.

Deprecating Aave v1: Due to high gas fees and a lack of incentive to migrate, Aave v1 still contains approximately 60% of the value locked in the broader Aave protocol. By introducing liquidity mining rewards only provided on Aave v2, liquidity providers and borrowers will naturally migrate toward the optimized version. Declining liquidity on Aave v1 will facilitate a gradual deprecation of this iteration of the protocol, allowing more development activity to be directed at Aave v2.

Liquidity Mining Design Commentary:

We would like to open up the discussion among the community to explore introducing liquidity mining incentives:

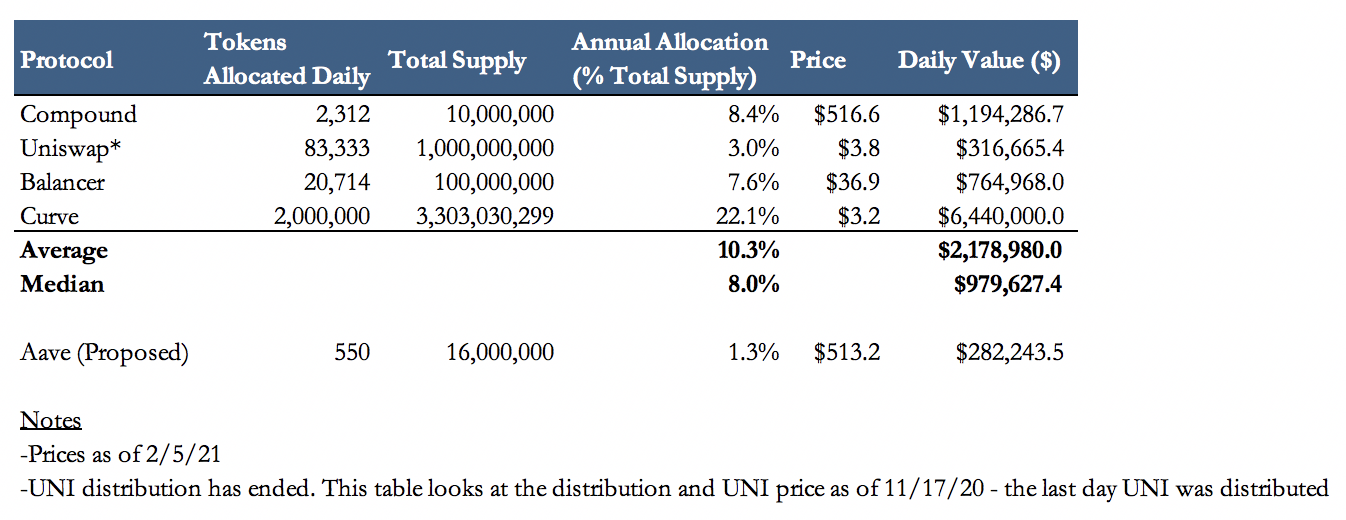

Distribution: We (ParaFi) propose a distribution of 550 Staked AAVE (stkAAVE) per day split 50-50 between lenders (275) and borrowers (275). We have considered various splits but, for now, have decided to go with an equal split for this pilot liquidity mining program.

This distribution is in line with the daily staking rewards and equates to 200,750 stkAAVE distributed per year or $103MM ($513.2/AAVE) in annualized rewards to borrowers/lenders at current prices (excluding any additional staking yield). From a supply perspective, this distribution results in only 1.25% of the fully diluted AAVE supply released each year. From a dollar value and token percentage standpoint, 550 stkAAVE/day remains significantly lower than comparable DeFi platforms. We believe the community will increase the LP distribution over time to become in line with other LM programs.

However, this allows the community to appropriately scale the distribution based on market dynamics and user activity. We have seen new DeFi protocols overpay for liquidity in the short-run and underpay for liquidity in the long-run. A relatively lower distribution to start leaves the ecosystem reserve with enough resources to scale up/down the allocation to users. If 550 stkAAVE/day is low based on liquidity and utilization, the community can vote to increase the distribution. A healthy portion of the reserve still remains for other critical areas (i.e rewarding integrations, grants, audits, etc).

Targeted Markets:

Given the number of markets on Aave, we see value in rewarding a handful of markets to start through a targeted distribution. The goal of this distribution is to increase borrow volume, pool utilization, and overall fees generated for the protocol. Over time, the community can vote to reward more markets.

For the initial distribution, we propose the following markets should be included:

- USDC

- USDT

- DAI

- GUSD

- sUSD

- TUSD

- ETH

- WBTC

Pro-Rata Distribution and stkAAVE Rewards

550 Staked AAVE (stkAAVE) per day will be allocated pro-rata across supported markets based on the dollar value of the borrowing activity in the underlying market.

This distribution strategy rewards markets based on borrow demand. Markets with higher dollar value borrowed receive a higher share of the daily stkAAVE rewards.

stkAAVE will be rewarded instead of AAVE to align long-term incentives, disincentivize speculative farmers, and allow users to earn an underlying yield on top of the AAVE they earn. This helps align LPs by giving them more governance weight upfront and secure the protocol by increasing the amount of AAVE staked in the Safety Module. LPs then immediately earn a staking yield on their vested AAVE.

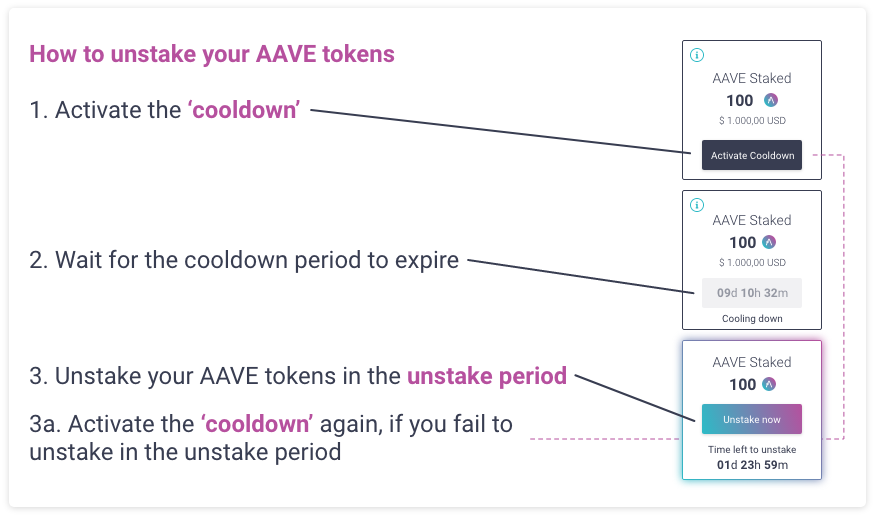

stkAAVE requires a 10 day cooldown period. The cooldown period must be started before LPs can unstake their AAVE. After the cooldown period, users have a 2 day window to unstake. By distributing rewards in stkAAVE, borrowers and lenders are immediately aligned with the protocol, increasing the security stake while earning a yield on their AAVE rewards.

This cooldown period indirectly serves as a vesting component for LP rewards. In Compound’s liquidity mining program, Gauntlet stated a “large fraction of COMP holders are selling all of their earnings and not staying long-term holders.” We have seen this dynamic take place in a number of DeFi protocols post-launch. By implementing stkAAVE rewards, we naturally mitigate this suboptimal outcome. If need be, the community can vote to implement a vesting component for stkAAVE (i.e LPs receive ½ stkAAVE upfront, receive ½ stkAAVE in 6 months).

There is room to increase the daily AAVE distribution based on the number of markets, liquidity levels, and utilization. Over time, the LP rewards can be used to bootstrap liquidity in new markets and encourage new assets to be onboarded.

Any distribution schedule can be reviewed on a quarterly basis.

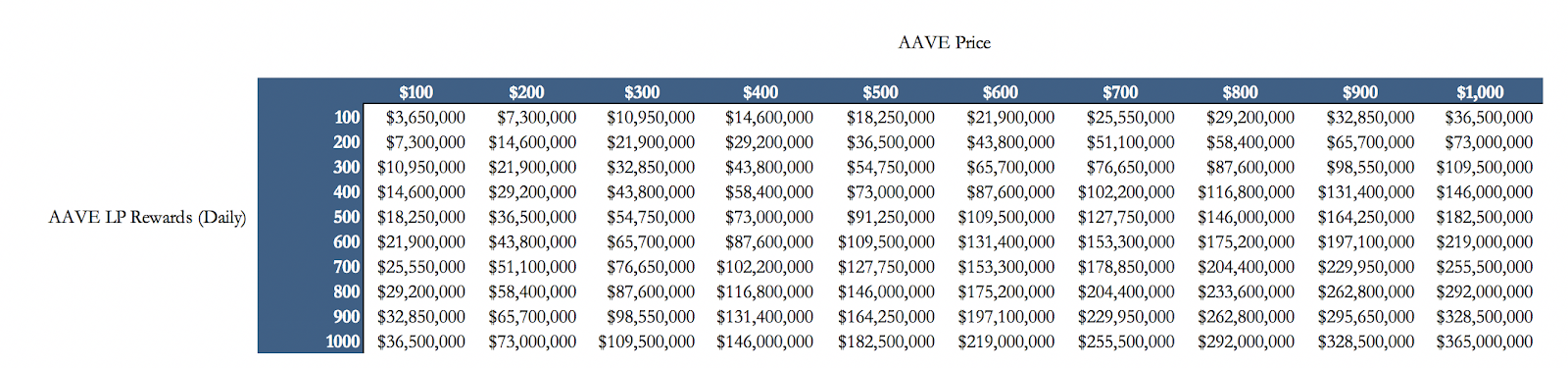

Projected AAVE LP Rewards (Annualized)

We welcome feedback from the community on this proposal.

Poll:

- Yes

- No

0 voters