title: MaticX Polygon v3 Upgrade

author: @Llamaxyz - Defi_Consulting(@MatthewGraham) @scottincrypto

created: 2023.02.02

Simple Summary

This ARFC proposes updating the MaticX Reserve on Polygon to facilitate an expansion of the MaticX/wMATIC loop strategy in the anticipation of rewards being introduced in the near future.

Abstract

The utilisation of the MaticX reserve has been trending higher over time and with the introduction of deposit rewards, there is an expectation the SupplyCap will be reached prohibiting additional MaticX from being deposited.

Increasing the SupplyCap enables the recursive MaticX/wMATIC strategy to grow beyond the current constraints. Enabling borrowing with a reasonable BorrowCap and the introduction of borrowing rewards will lead to significant utilisation of the MaticX reserve.

This proposal facilitates the expansion of MaticX yield-based strategies on Aave v3 Polygon by creating more favourable bootstrapping conditions. The introduction of liquidity mining rewards are expected to drive notable inflows and usage to the v3 deployment.

Motivation

Over the previous months, @Llamaxyz has been working with various communities to craft favourable conditions on Aave v3 Polygon to facilitate the creation of several yield aggregation products. The below proposals details are applicable:

- Proposal to add MaticX to Aave v3 Polygon Market

- [ARFC] Aave v3 Polygon wMATIC Interest Rate Update

- [ARFC] SD Emission_Admin for Polygon v3 Liquidity Pool

- [ARFC] stMATIC & MaticX Emission_Admin for Polygon v3 Liquidity Pool

This proposal is a continuation of the above work.

In support of the upcoming liquidity rewards distribution, this proposal seeks to increase the SupplyCap, enable borrowing and introduce a BorrowCap sufficient to create a notable deposit yield.

The current SupplyCap is set at 6.0M units of MaticX and has not been updated since MaticX was listed on Aave v3. When Llama listed MaticX, the risk parameters were set very conservatively. With improved liquidity conditions now and soon even better conditions when the new MaticX / bb-a-wMATIC pool launches in February, this SupplyCap can be increased.

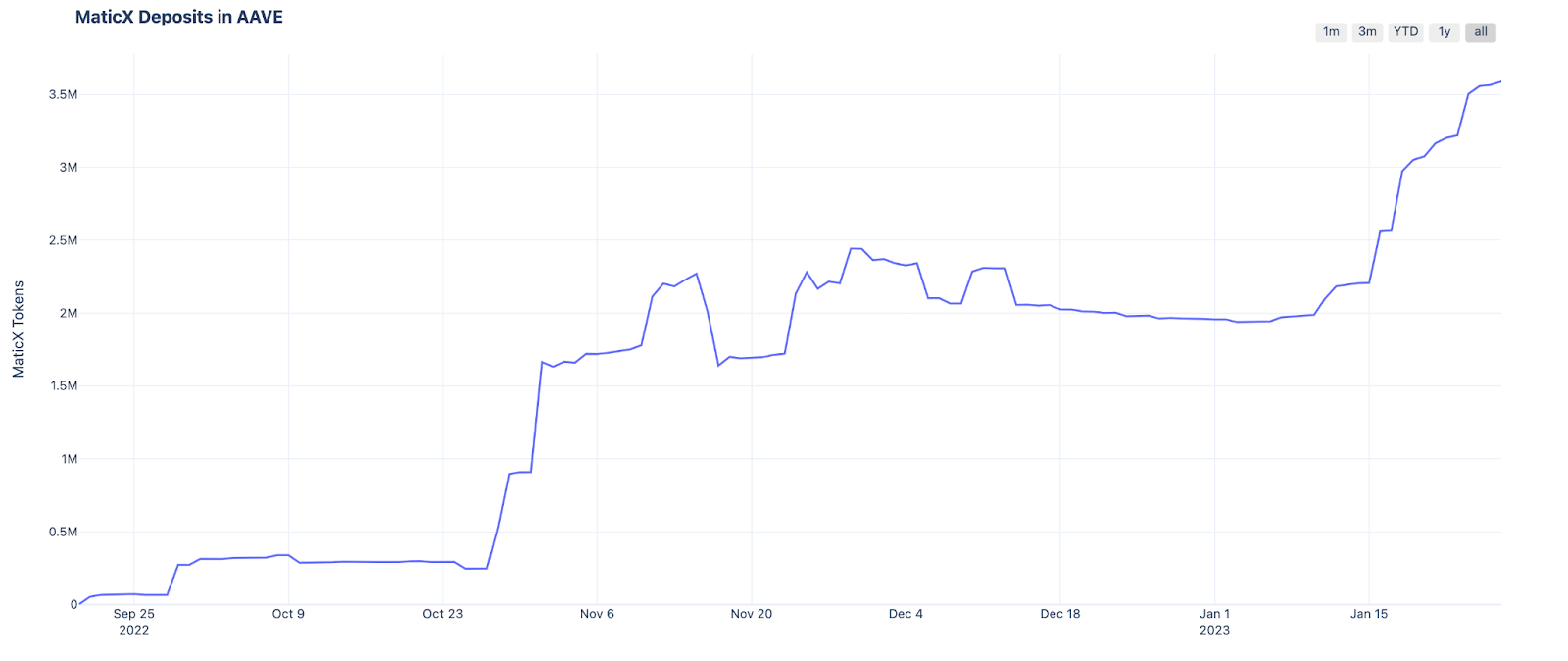

With the introduction of SD rewards, it is fair to conclude, based upon past experience, there will be a material inflow of deposits into the MaticX reserve. With utilisation already at 66.23% and deposits climbing in both USD and units of MaticX terms, as shown below, it is highly expected that the SupplyCap will indeed be reached with the introduction of SD rewards.

The charts below show the historical volume of MaticX and USD value of MaticX deposited in the reserve over time.

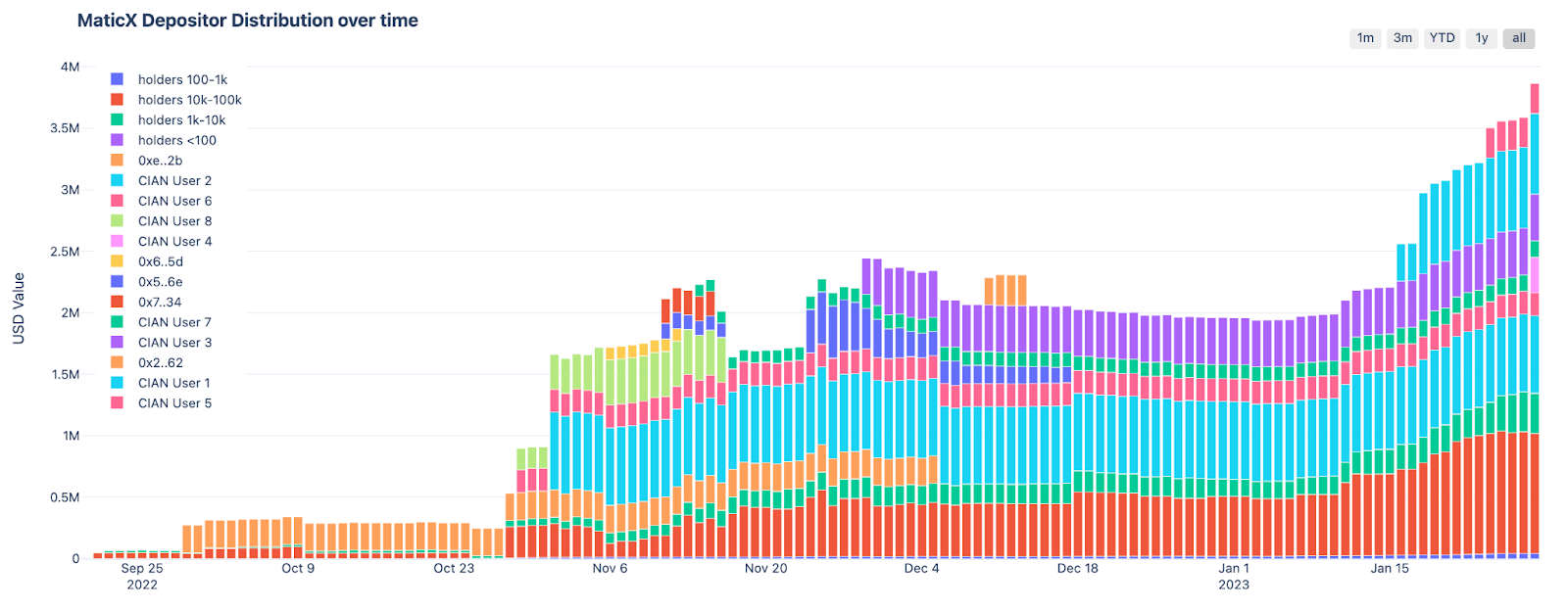

The recent push to launch automated strategies has led to material improvements in utilisation of the SupplyCap. With more strategies to be launched in the near future, the SupplyCap will become a burden preventing other communities’ products from growing TVL. This problem will be exacerbated with the introduction of rewards. If the SupplyCap is reached, then no new MaticX deposits can be made to improve the health factor of these strategies. This causes the strategies to deleverage and generate a lower return for their users. This suboptimal outcome discourages builders and creates a need to proactively manage risk parameters and work closely with communities that build on top of Aave. The chart below shows the distribution of users’ funds in the pool.

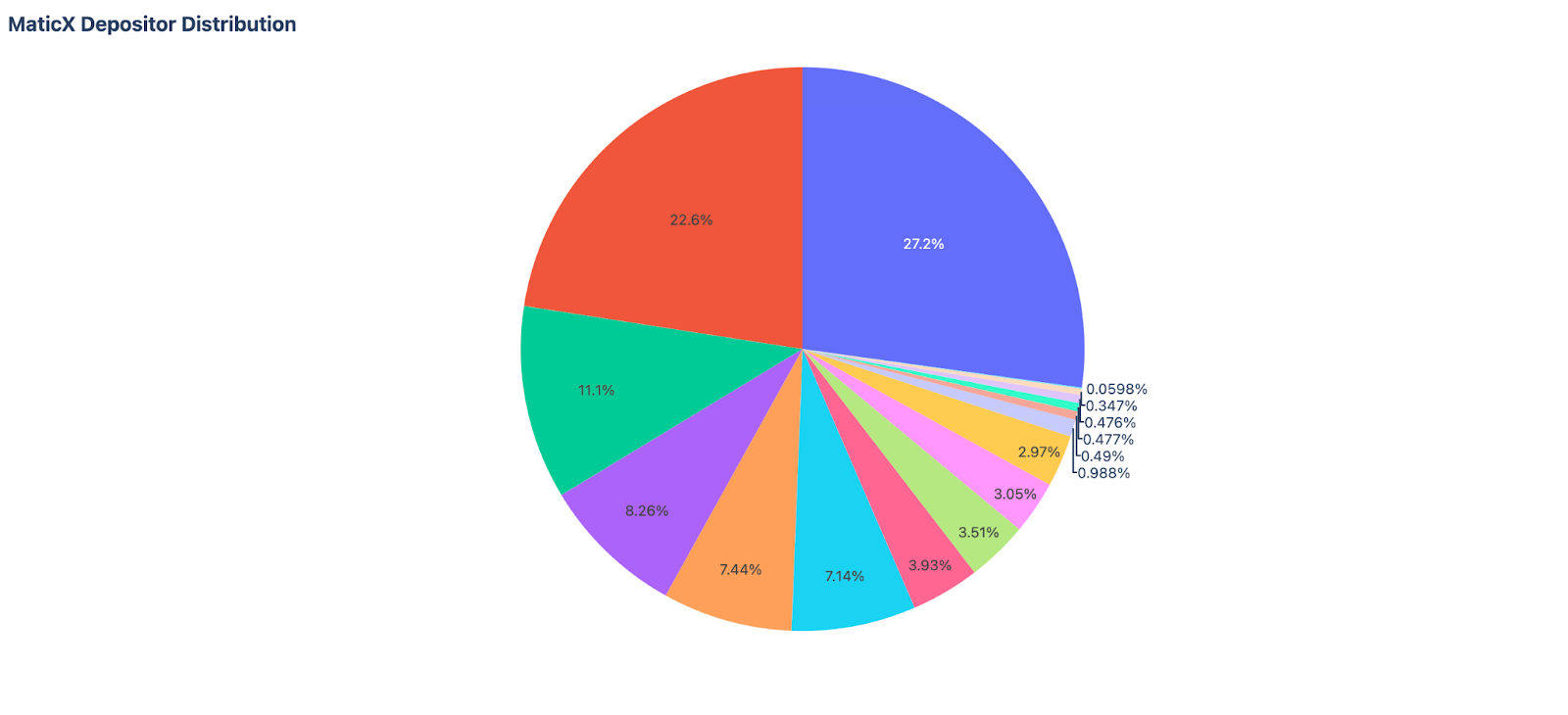

The chart below shows the distribution of MaticX deposits.

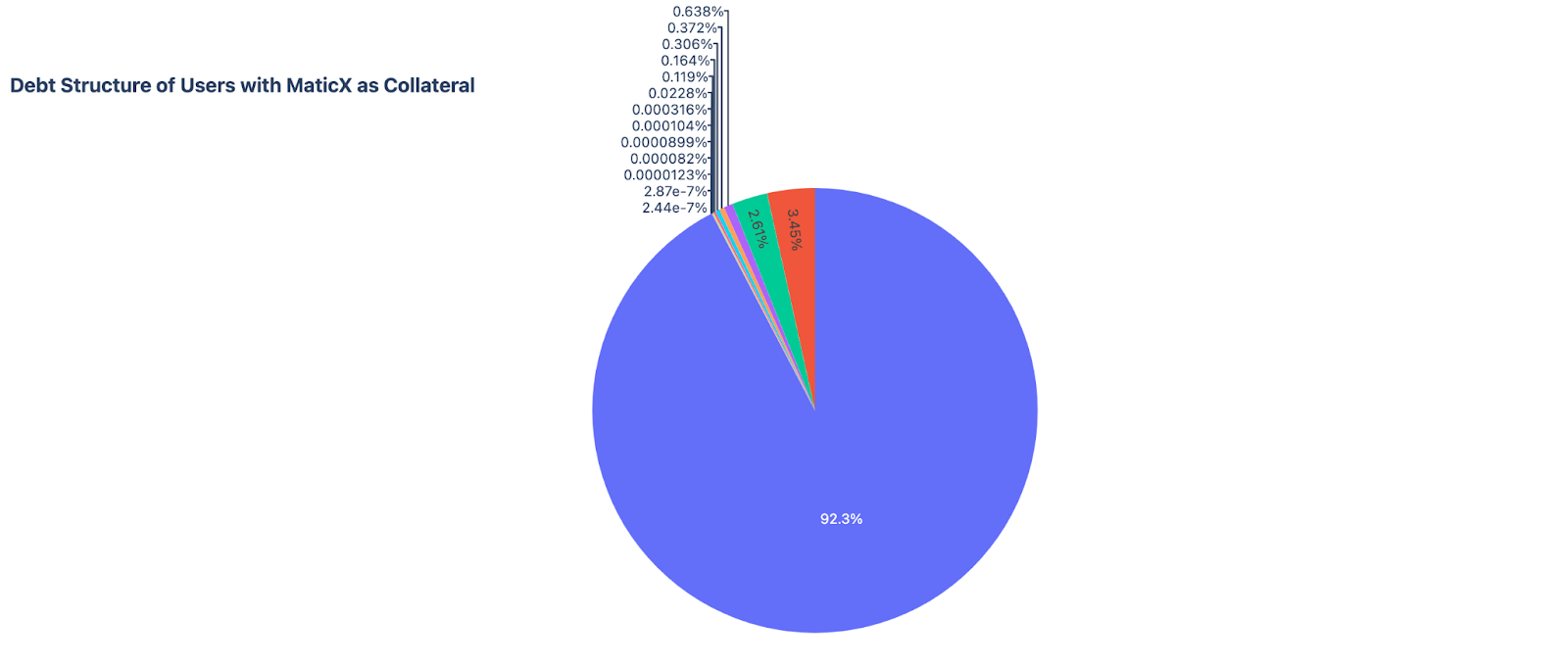

The chart below shows that 92.3% of all debt drawn against MaticX collateral positions is wMATIC. This highlights the significance of the MaticX and wMATIC relationship.

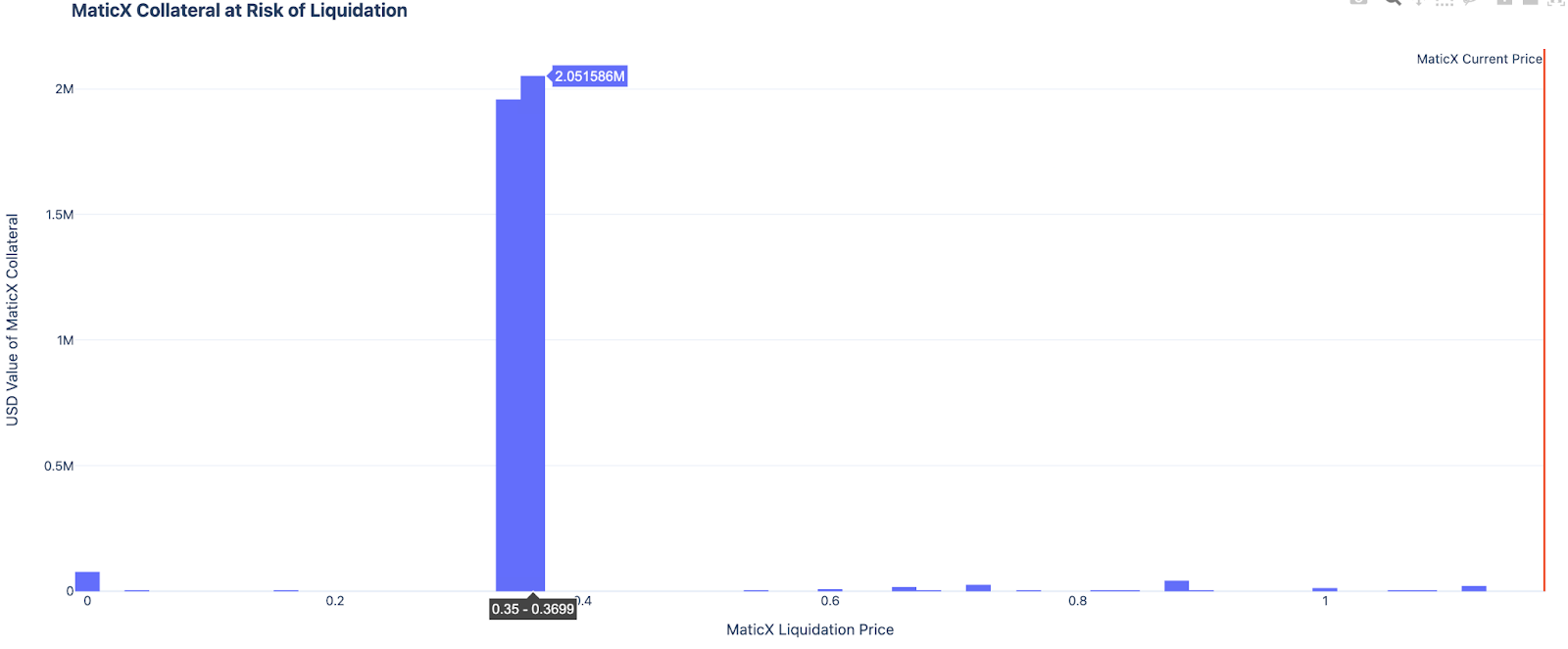

The chart below shows the amount of MaticX that would be for a given price. If the price of MaticX falls to 35 cents, 2.05M units of MaticX will be liquidated. This is shown as the 3.45% allocation in the above pie chart which represents the largest MaticX collateral and non wMATIC debt position.

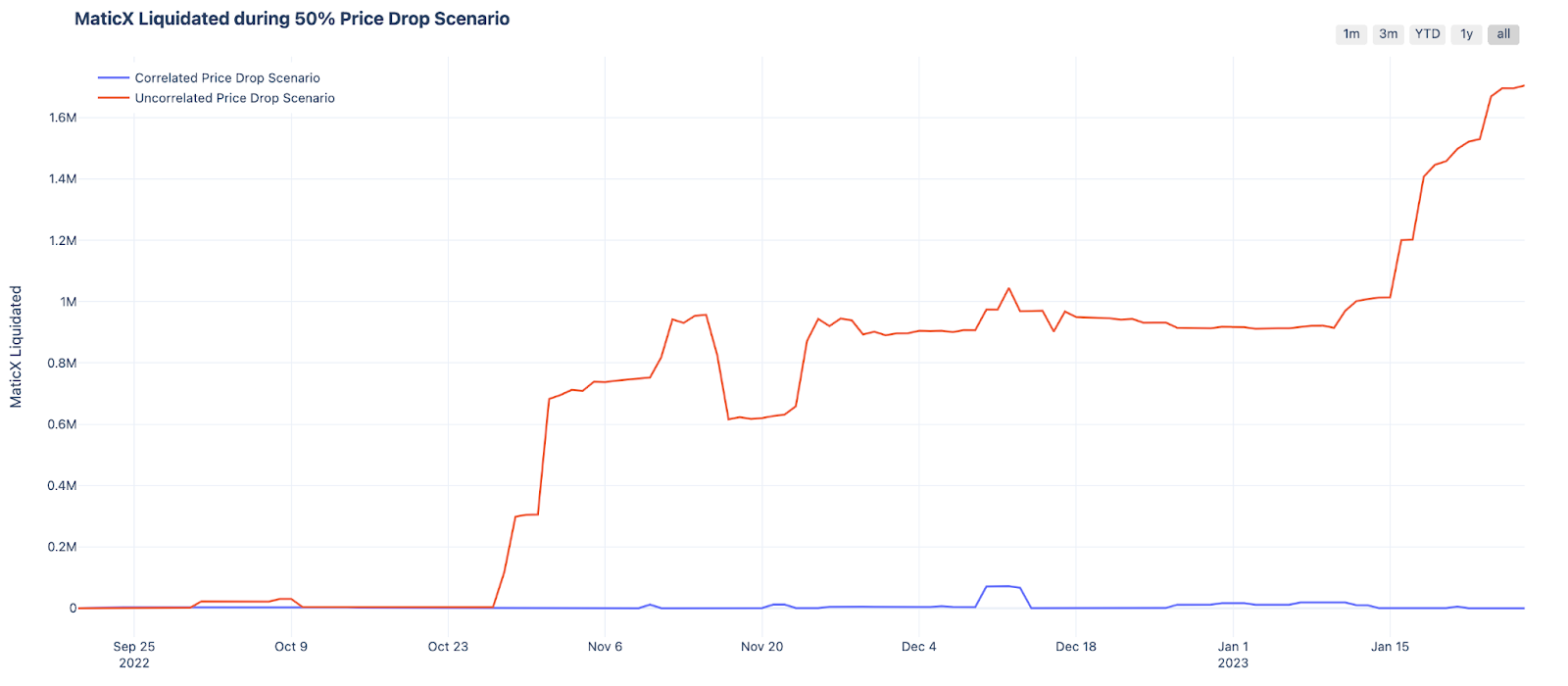

By aggregating all positions together, we can simulate the volume of MaticX deposits liquidated for a predefined percentage fall in the MaticX price. The chart below shows the volume of MaticX deposits liquidated for a 50% fall in the price of MaticX. A 50% price fall in MaticX would trigger 1.7M units of MaticX collateral positions being liquidated as of the 27th January 2023.

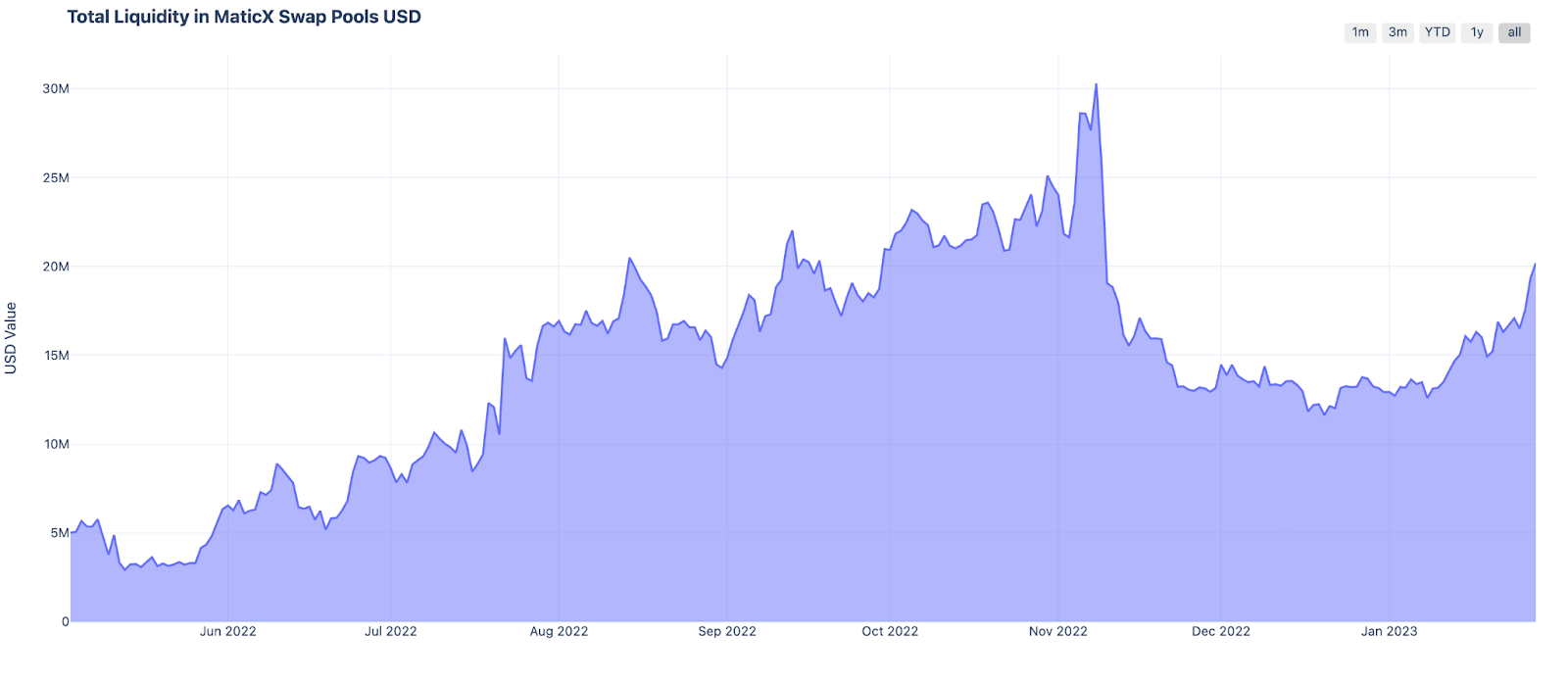

On-chain liquidity for MaticX, measured in units of MaticX, has been steadily sideways to slightly higher overall during 2023.

The chart below shows the USD value held within the main liquidity pools across Polygon.

- Balancer v2 MaticX/wMATIC

- Quickswap MaticX/wMATIC

- Dystopiaswap MaticX/wMATIC

- Meshswap MaticX/wMATIC

- Meshswap MaticX/USDC

The MaticX oracle is a calculated oracle and does not rely on spot pricing which removes the ability to liquidate users on Aave through manipulating MaticX spot pricing. The MaticX/USD Chainlink Oracle was used upon listing MaticX and wMATIC/USD when listing wMATIC. The MaticX oracle utilises the MATIC oracle in calculating its feed price. It is worth noting that to influence the spot price of MaticX through repeat entries on a lending market, the attacker would need to offset the flow of arbitrage traders profiting from the price variance. ie: If MaticX spot price is above the calculated feed, then swap MaticX for wMATIC and stake, and if MaticX’s spot price is trading at a discount, swap wMATIC fro MaticX, deposit Aave, borrow wMATIC and swap to MaticX in a recursive loop. Some arbitrage flow would be limited by the bridge transaction times and the Stader provided deposit liquidity.

When Borrowing is enabled, it becomes possible to arbitrage the spot and the calculated oracle. The arbitrage loops makes it more expensive to move the MaticX away from the Net Asset Value as it becomes profitable to run a counter strategy. The combination of having a base asset, wMATIC, with a staking contract makes this feasible and Aave’s liquidity would then make it easier to execute the arbitrage strategy. The chart below shows the DEX Aggregator price relative to the Calculated price feed. It shows the spot pricing closely tracking the calculated feed.

This is supportive of enabling borrowing of MaticX on Polygon Aave v3.

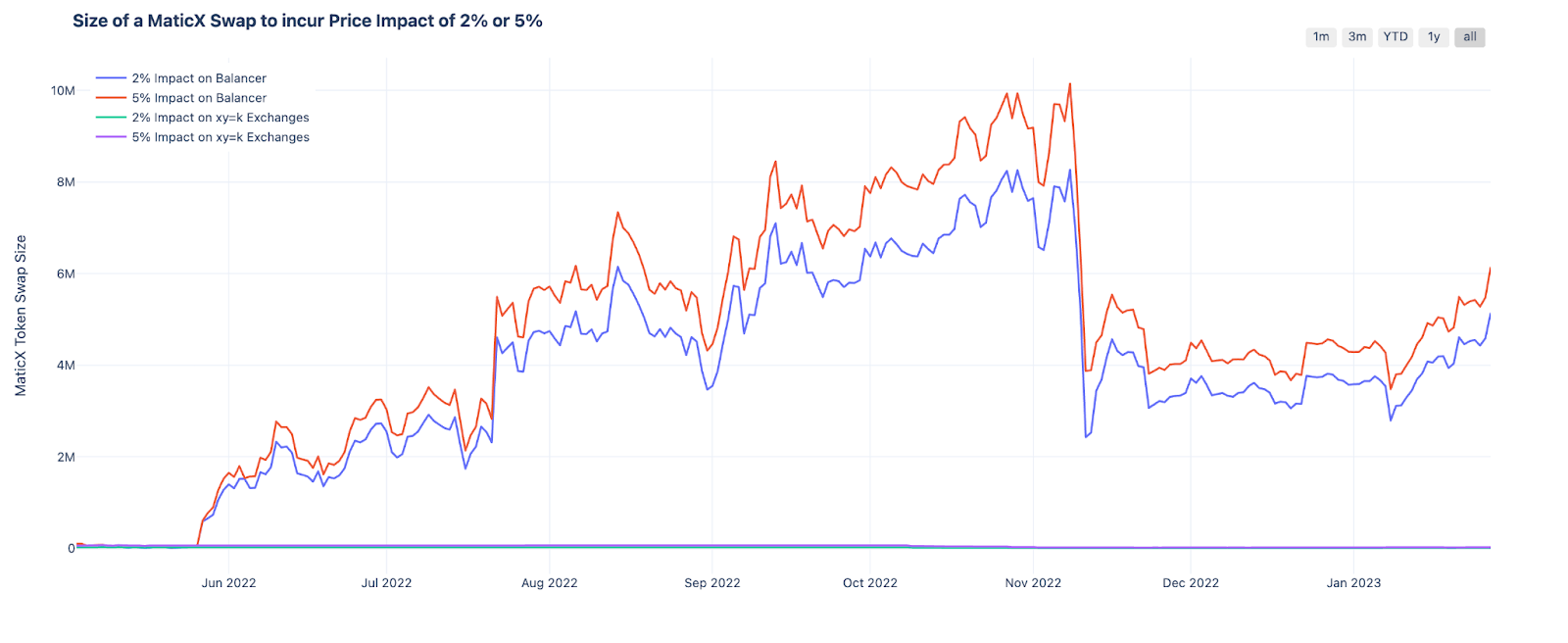

Looking at just the main liquidity pool, a 2% price impact swap will facilitate a swap size of 5.13M units. For 5% price impact, 6.12M of MaticX can be swapped. The entire SupplyCap on Aave could be purchased for less than a 5% price impact from a single DEX pool.

Expanding beyond the main liquidity pool and routing a swap via 1inch on Polygon, the below swap sizes can occur for a predefined 2% price impact. This is optimised for speed when using the 1inch’s new Fusion upgrade. There is also additional liquidity available by Stader, which is not likely to be integrated into the 1inch platform.

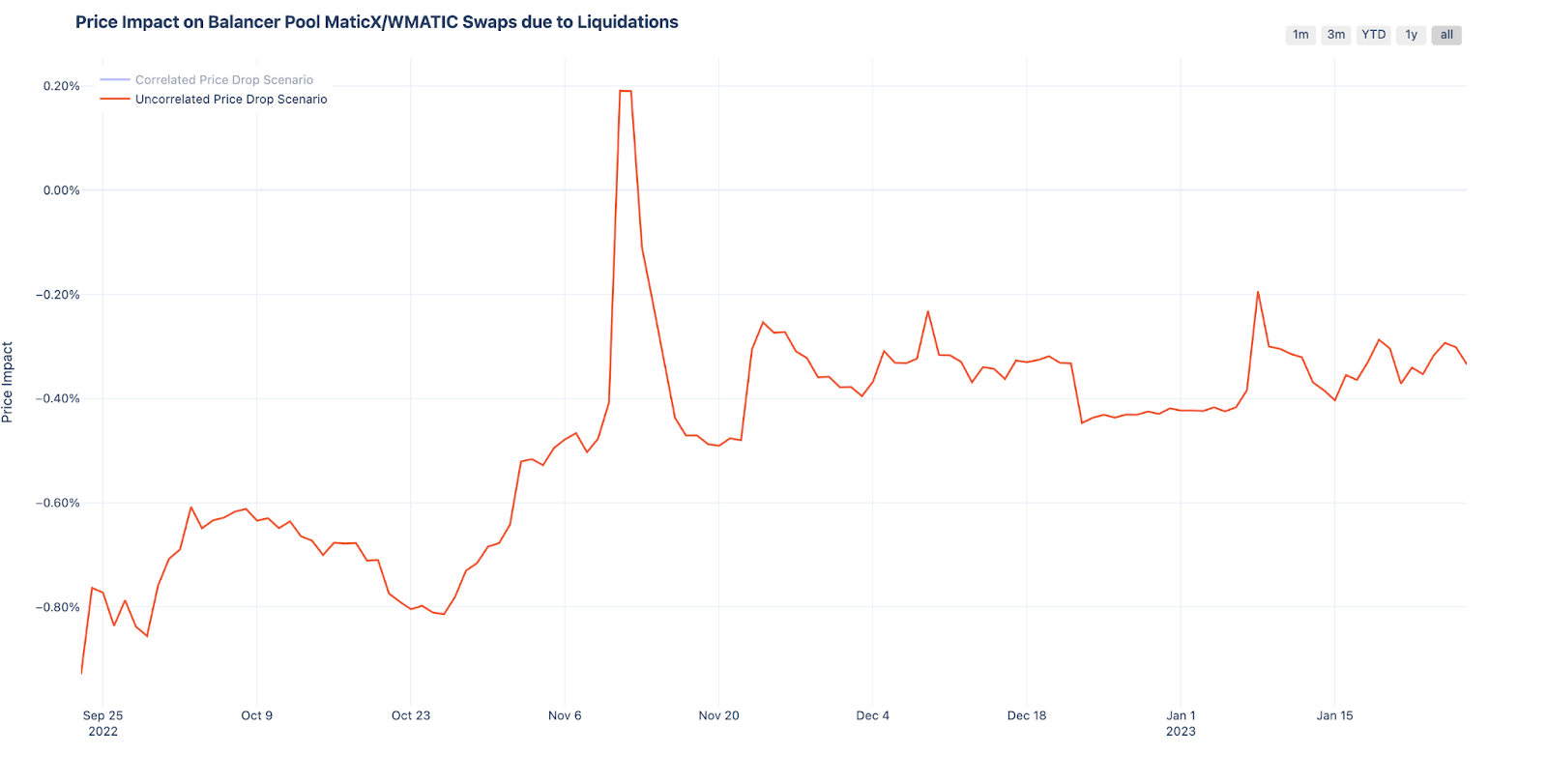

With reference to the MaticX collateral and now wMATIC debt positions, the below chart shows the amount of price impact the main MaticX/wMATIC Balancer pool would occur when all users positions are liquidated in the event of a 50% price fall event. Liquidating all MaticX positions due to a 50% fall in the price, would cause -0.33% price impact if swapped at once. Due to improving liquidity over time, the price impact of liquidating users due to a 50% fall in price is reducing. This may change with the introduction of more structured products that utilise uncorrelated assets as the initial collateral deposit. However, these strategies can also be automated and unwind the leverage gradually to avoid liquidation.

It is worth noting here, a new MaticX / bb-a-wMATIC pool will be deployed (February) that will have an amplification factor of 500 and will replace the current MaticX/wMATIC pool with an amplification of 50. This 10x amplification factor increase will significantly improve liquidity measured in swap size for a given price impact through the main Balancer Pool. Migrations of liquidity from one pool to the next occurs fairly quickly with 86% of the liquidity migrating within 12 days last time the pool was migrated.

Having worked with the Balancer team we are confident the vast majority of the liquidity will be migrated to the new pool quickly. This is largely due to the end user preference to use automated strategy platforms like Beefy, InstadApp, Cian, and others…

With Borrowing Enabled and borrowing rewards introduced, the recursive deposit and borrow the same asset loop, is expected to inflate deposits and borrowings in the reserve. An ideal outcome would be for on-chain liquidity to benefit from the introduction of borrowing rewards. However, in the past users have shown a preference to enter a single asset recursive loop. This strategy would be limited by the lesser of the LTV, SupplyCap and BorrowCap parameters.

Due to the imminent SD rewards emissions, we are opting for a more generous BorrowCap allowance than otherwise would have been suggested. A BorrowCap of 5.2M which is still less than the (Uoptimal + 10%) x SupplyCap methodology indicates, but sufficient to enable the Aave community to gauge the market’s appetite for borrowing MaticX. Future proposals can revise this parameter. It is worth noting that during discussions with some yield strategy managers, it was highlighted that some vaults are optimised for yield across various strategies which include providing on-chain liquidity.

Since listing MaticX, the Loan To Value (LTV) and Liquidation Threshold (LT) has not been revised. This proposal recommends revising the LTV and LT from 50% to 58% and 65% to 67% respectively. These parameter adjustments will not affect the recursive loop strategies MaticX/wMATIC that utilise the Matic eMode category. These adjustments will encourage users to deposit MaticX as collateral and borrow assets other than wMATIC.

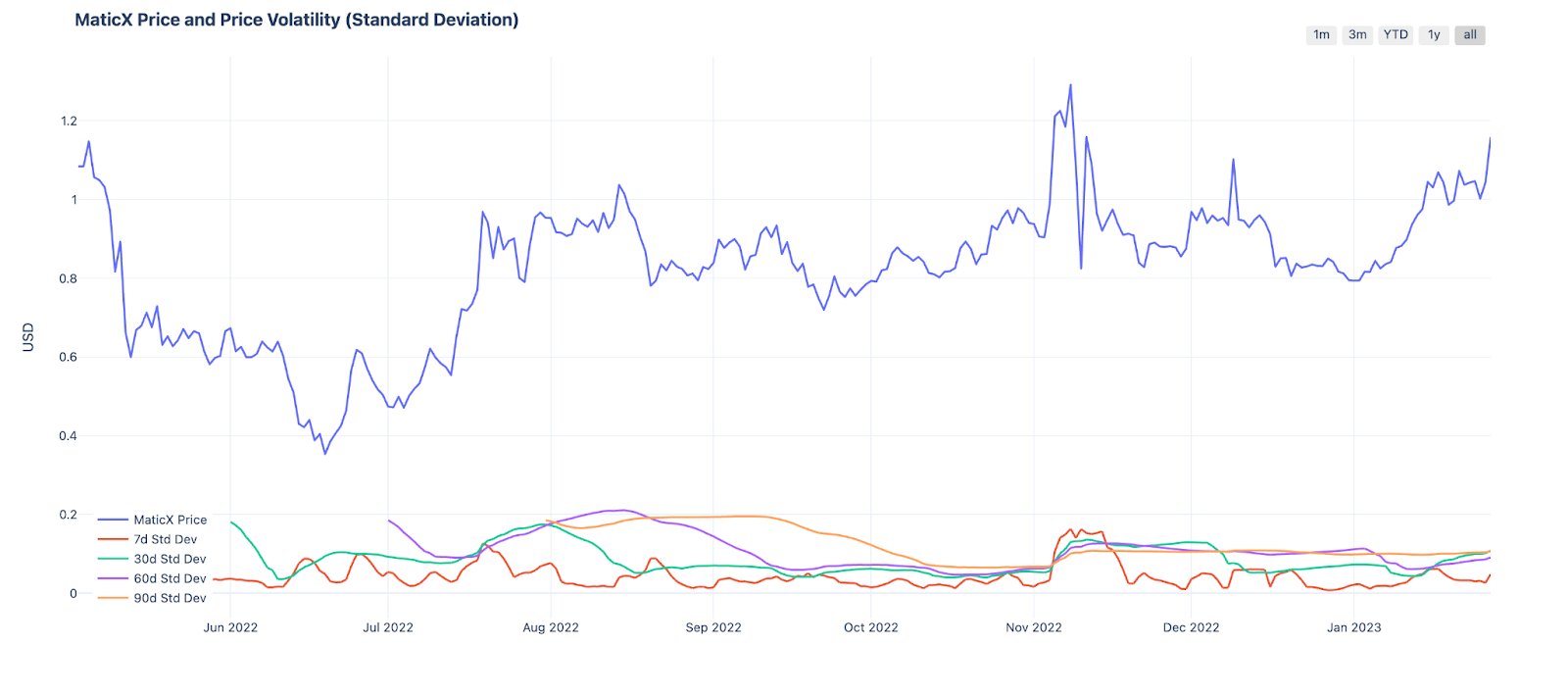

The chart below shows the MaticX price and how the volatility of MaticX has varied overtime. This is reflective of the underlying wMATIC assets volatility.

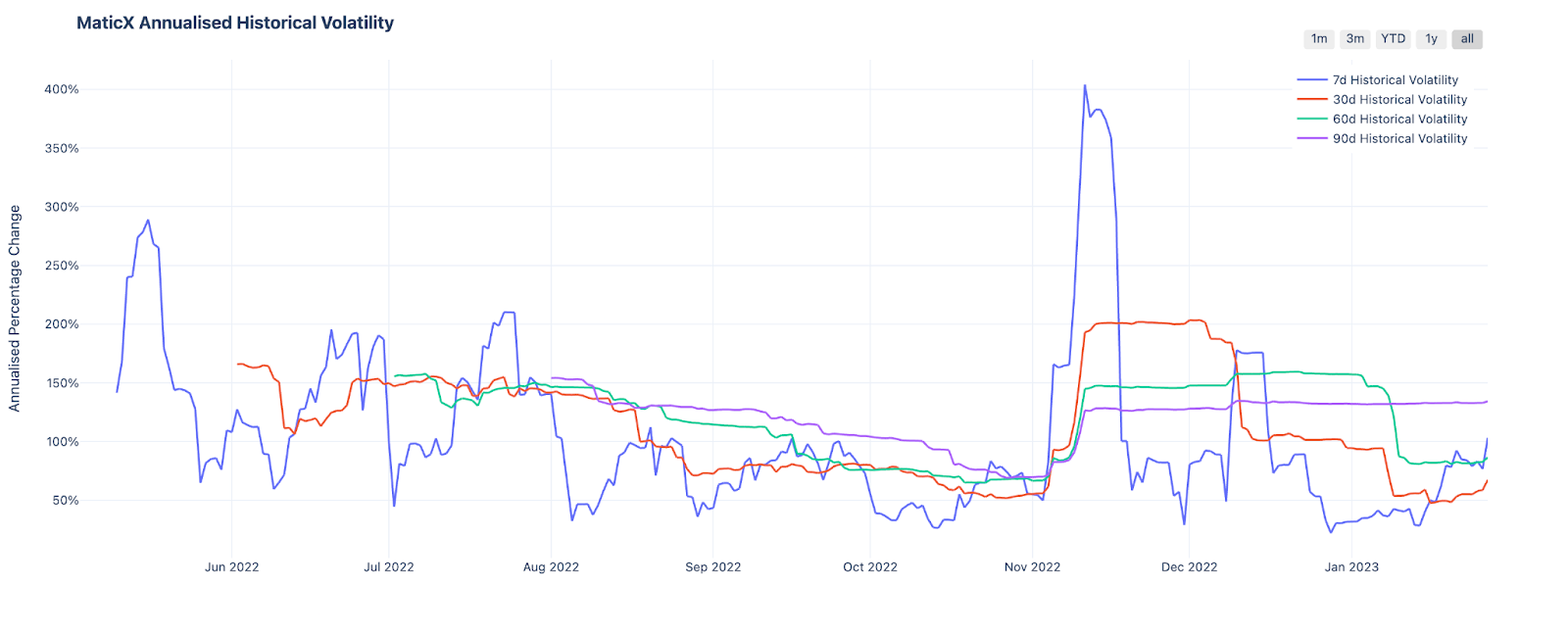

The chart below shows Annualised Volatility for various time sample periods.

The above data indicates a strong case for increasing the LTV for MaticX and wMATIC. As this proposal focuses on MaticX, any future wMATIC upgrades will be presented via a separate proposal.

Increasing the LTV and LT as defined above may be just enough, but probably not, to support building leverage long and short products with ~2x leverage which also minimise carry costs through utilising the MaticX/wMATIC recursive loop. Some communities are exploring the feasibility of this new type of structured product. At 65% LTV, ~2x leverage is possible as proven by Index Coop’s MATIC2x-FLI-P that uses Aave v2 and wMATIC as collateral. However, it is not yet known if the recursive loop with 58% LTV can enable free carry leverage trading products to be developed on top of Aave v3. To be clear, this does not influence the risk parameters setting and is intended only to provide context around some of the benefits associated with higher LTV and LT parameters.

Interest Rate

With Borrowing enabled, the following rationale was applied when developing the MaticX interest rate.

For the recursive strategy, it is highly desirable the deposit APR changes gradually with varying Utilisation. As the deposit rate for MaticX offsets the borrowing costs of wMATIC, any heightened volatility in the deposit rate of MaticX leads to more frequent rebalancing. This is more prominent within strategies trying to maximise yield. Due to the recursive loop, the end user experiences amplified volatility of the delta between the MaticX deposit rate and wMATIC borrowing rate.

To reduce this volatility, the Slope1 parameter should be minimised. A higher Uoptimal also reduces the volatility of borrowing costs by acting to distribute the increase in the borrow rate over a greater Utilisation horizon. An initial MaticX Slope1 parameter of 4% is proposed.

In accommodating a low Slope1 parameter and achieving a suitable Borrowing rate, a Base can be introduced. The borrow rate at the Uoptimal utilisation point is equal to the sum of the Base and Slope1 parameter. An initial Base parameter of 0.25% is proposed. The borrow rate at the Uptimal point is 4.25%.

An initial Uoptimal parameter of 65% is proposed. In time this can be increased depending upon the size of the larger borrowers of MaticX holdings. It is worth noting that swapping 5.125M of wMATIC to 4.79M of MaticX incurs a 2% slippage and the liquidator receives a 10% liquidation bonus payment which more than offsets the price impact of a swap. This compares favourably with the initial BorrowCap of 5.2M units of MaticX.

An initial Slope2 parameter of 150% is proposed and is support by Gauntlet.

Specification

The following risk parameters are being proposed and have been reviewed by Llama.

| Parameter | Proposed Value |

|---|---|

| Loan To Value | 58.00% |

| Liquidation Threshold | 67.00% |

| Liquidation Bonus | 10.00% |

| Liquidation Protocol Fee | 10.00% |

| SupplyCap | 8.6M units |

| Borrowing | Enabled |

| BorrowingCap | 5.2M |

The following interest rate parameters have been reviewed by Llama.

| Parameter | Proposed Value |

|---|---|

| Base | 0.25% |

| Uoptimal | 45.00% |

| Slope1 | 4.00% |

| Slope2 | 150.00% |

| Reserve Factor | 20.00% |

| Stable Borrowing | Disabled |

| Stable Slope1 | 0.50% |

| Stable Slope2 | 150.00% |

| Base Stable Rate Offset | 2.00% |

| Stable Rate Excess Offset | 5.00% |

| Optimal Stable To Total Debt Ratio | 20.00% |

Next Step

2-3 weeks of discussion on the forum and then a Snapshot vote will be held. If the vote goes well, then Llama will prepare the payload for BGD to review soon thereafter.

Copyright

Copyright and related rights waived via CC0.