Summary

A proposal to:

- Increase the supply cap of PT-sUSDe-27NOV2025 on the Ethereum Core instance

- Increase the supply cap of PT-USDe-27NOV2025 on the Ethereum Core instance

- Increase the supply cap of sUSDe on the Ethereum Core instance

- Increase the supply cap of ezETH on the Base instance

- Increase the supply cap of weETH on the Base instance

All cap increases are backed by Chaos Labs’ risk simulations, which consider user behavior, on-chain liquidity, and price impact, ensuring that higher caps do not introduce additional risk to the platform.

PT-sUSDe-27NOV2025 (Ethereum Core)

PT-sUSDe-27NOV2025 has reached its supply cap at 1.2 billion tokens, following an inflow of over 300 million tokens in the past 5 days, indicating persistent demand.

Supply Distribution

The supply distribution is moderately concentrated, with the top user accounting for over 20% of the supply, while the top 8 suppliers have a cumulative share of over 65%. The health factors are clustered tightly in the 1.02—1.11 range, which, given the high correlation of debt and collateral assets, does not pose any immediate liquidation risk.

PT-sUSDe-27NOV2025 is used to collateralize stablecoin borrow positions. Given the high correlation of the debt and collateral assets, the liquidation risk is minimal.

Market and Liquidity

PT-sUSDe-27NOV2025’s implied rate has seen substantial volatility, decreasing by 1%, over the past week and id currently converging at an 8% implied yield. While the implied rate’s volatility affects the price of the principal token, its impact diminishes with maturity.

Due to the underlying design of the Pendle AMM, the slippage on a 35 million swap is limited to 1.5% at the current time to maturity, supporting an increase in the supply cap.

Additionally, Pendle’s order books have over 130 million liquidity at or above 6% implied yield, providing a substantial absorption buffer.

Recommendation

Given the persistent demand, ample on-chain liquidity in both Pendle AMM and order book, and safe user behavior, we recommend increasing the supply cap of PT-sUSDe-27NOV2025 on the Ethereum Core instance.

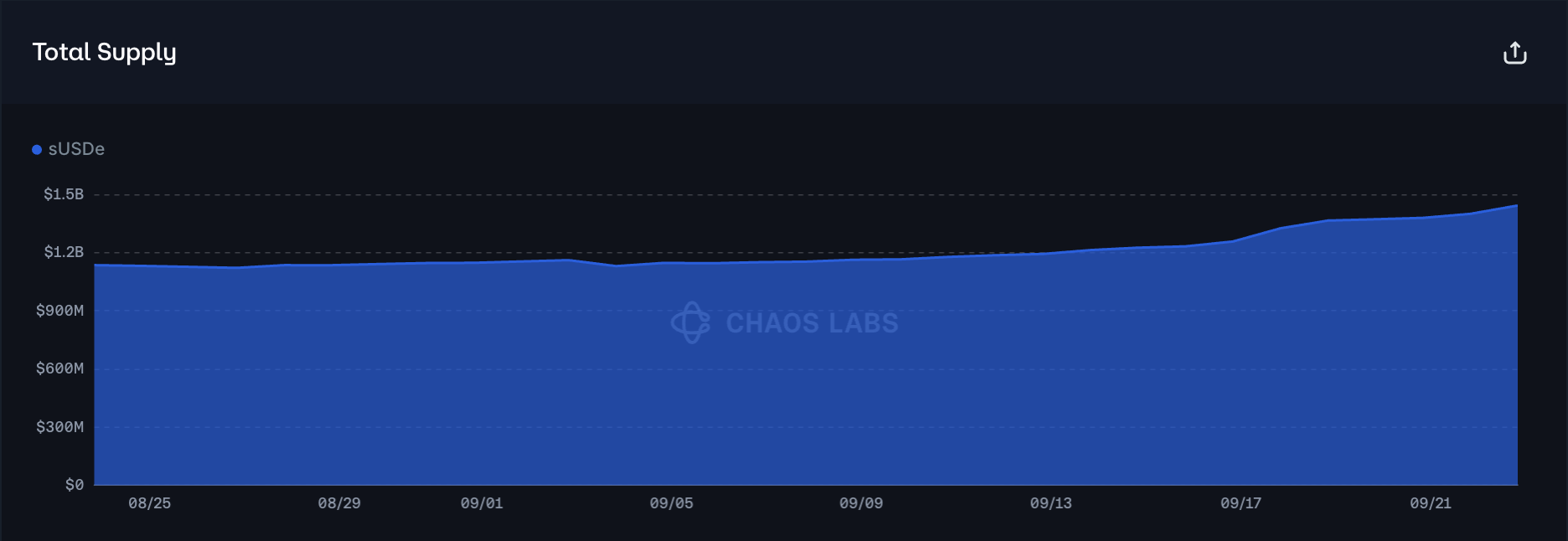

sUSDe (Ethereum Core)

sUSDe’s supply on the Ethereum Core instance has exhibited steady growth, reaching 93% of its 1.2 billion cap.

Supply Distribution

sUSDe’s supply distribution is moderately concentrated, with the top user representing 9% of the supply and the top 10 accounting for over 30%. As can be observed from the chart below, the suppliers are borrowing USDT and USDC, collateralizing them with equal parts USDe and sUSDe. This behavior is incentivized by Ethena’s Liquid Leverage, where users get additional USDe rewards when supplying it in equal share with sUSDe. Effectively, users are capturing the spread between stablecoin yield and borrow costs of USDT and USDC by leveraging their debt with Ethena collateral.

As mentioned, the users borrow primarily stablecoins, namely USDT and USDC, representing over $1.2 billion of debt. Given that the debt is collateralized with stablecoins, even low health positions pose minimal risk, as the debt and collateral assets are highly correlated.

Liquidity

At the time of writing, on-chain liquidity can absorb a sell order of 30 million sUSDe at 0.2% slippage, supporting an increase in supply cap.

Recommendation

Considering users’ persistent demand for liquid leverage, low liquidation risks, and strong on-chain liquidity, we recommend increasing the supply cap of sUSDe.

ezETH (Base)

ezETH supply on Base has increased substantially in the past 24 hours, adding over 1,500 tokens.

Supply Distribution

The supply distribution is highly concentrated, with the top user accounting for over 45% of the market. The users are supplying ezETH to collateralize wstETH debt, therefore leveraging restaking yield against WETH borrowing. As the debt and collateral are highly correlated, the liquidation risk is minimal.

As wstETH is the dominant debt asset for ezETH collateral, the liquidation risk in the market is low, due to high correlation of wstETH and ezETH in price.

Liquidity

At the time of writing, the price impact on a 50 ezETH swap is limited to 1%, supporting an increase of the ezETH supply cap.

Recommendation

While the market exhibits significant supply concentration, both liquidity conditions and user behavior allow for a meaningful cap increase without introducing additional protocol risk. Hence, we recommend increasing the supply cap of ezETH to drive additional demand for wstETH borrowing.

weETH (Base)

weETH has reached 91% of its supply cap on Base, following an inflow of over 13 thousand tokens in the last 4 days.

Supply Distribution

The supply distribution of weETH is moderately concentrated. The top 6 users account for 56% of the total. The health factors are clustered in the 1.02—1.15 range. Nevertheless, since users are borrowing WETH, a highly correlated asset, the liquidation risk is minimal.

As noted, weETH is primarily used to collateralize WETH borrowing positions, which substantially reduces the probability of large scale liquidations due to high correlation of the assets.

Liquidity

At the time of writing, a swap of 700 weETH for WETH would result in a 1% slippage due to deep on-chain liquidity.

Recommendation

Considering the substantial demand to collateralize WETH debt with weETH, along with deep liquidity and safe user behavior, we recommend increasing the supply cap of weETH.

PT-USDe-27NOV2025 (Ethereum Core)

PT-USDe-27NOV2025 has seen a substantial increase in supply over the past week. Given the close maturity of the September PTs, we anticipate significant demand to supply the asset, as users are expected to swap the collateral on their looping positions.

Supply Distribution

The supply distribution of PT-USDe-27NOV2025 is moderately concentrated as the top user represents over 20% of the total, while the top 11 suppliers account for approximately 80% of the market. The distribution of health factors is dense, as the scores are clustered in the 1.01—1.16 range. The liquidation risk is minimal given the high price correlation of the PT and the debt assets.

PT-USDe-27NOV2025 is primarily used to borrow stablecoins. This allows users to earn a leveraged spread between stablecoin borrowing rates and the implied APY of the PTs as they approach maturity. Since this PT will converge to USDe and most debt is also denominated in USDe, the market currently faces minimal liquidation risk.

Market and Liquidity

Along with the November-expiry sUSDe principal token, the PT-USDe-27NOV2025 has also exhibited a declining implied yield, losing approximately 1% over the last 5 days.

At the time of writing, Pendle’s AMM liquidity is sufficient to limit slippage to 2% on a 19 million swap.

Additionally, the order book has over 15 million in liquidity at a 7% implied rate, adding a substantial absorption buffer.

Recommendation

As the demand for the asset is expected to grow, we recommend increasing the supply caps to facilitate the orderly transition of the collateral from PT-USDe-25SEP2025 to PT-USDe-27NOV2025.

Specification

| Market | Asset | Current Supply Cap | Recommended Supply Cap |

|---|---|---|---|

| Ethereum Core | PT-sUSDe-27NOV2025 | 1,200,000,000 | 2,400,000,000 |

| Ethereum Core | PT-USDe-27NOV2025 | 1,000,000,000 | 2,000,000,000 |

| Ethereum Core | sUSDe | 1,300,000,000 | 1,700,000,000 |

| Base | ezETH | 1,900 | 3,600 |

| Base | weETH | 120,000 | 150,000 |

Next Steps

We will move forward and implement these updates via the Risk Steward process.

Disclosure

Chaos Labs has not been compensated by any third party for publishing this AGRS recommendation.

Copyright

Copyright and related rights waived via CC0.