Summary

In response to recent shifts in stablecoin market conditions, Chaos Labs recommends lowering the target borrow rate for major stablecoin assets from 6.50% to 6.00%, which will be implemented through the Risk Stewards process. These adjustments aim to restore optimal utilization levels and enhance overall protocol capital efficiency.

Motivation

Since early October, stablecoin utilization across Aave markets has trended downward, resulting in reduced capital efficiency for depositors and lower protocol revenue generation. Currently, utilization averages 70-75%, representing a 25% decrease from August heights.

During the June–September period, utilization levels consistently met or exceeded target thresholds, prompting the recommendation, which increased the Slope 1 parameter for stablecoins by 100 basis points. This adjustment was made in response to elevated borrowing activity, primarily driven by Ethena-based PT looping strategies and the introduction of Ethena’s Liquid Leverage Incentive program, which generated strong leveraged yields and contributed significantly to DAO income. As illustrated below, peak borrowing demand aligned closely with the maximum volume of PTs supplied on the Aave Ethereum Core instance.

A substantial portion of stablecoin borrowing during this period was collateralized with Ethena-based assets, as users were leveraging the spread differential between underlying yield and variable borrow rates. In several cases, net yields exceeded 60% APY, particularly for PTs maturing in June through September, which exhibited implied yields in the 12–20% range. Following the maturity of the September PTs, implied yields declined materially, compressing the profitability of stablecoin looping strategies and triggering a substantial reduction in borrowing demand. As a result, the aggregate supply of Ethena-related assets fell from approximately $8.5 billion on September 21 to $4 billion after the September maturities, leading to a proportional contraction in overall stablecoin borrowing activity, which decreased from $13.8 billion to approximately $9.5 billion.

While PT deployments have been limited to the Ethereum Core instance at the time, borrow demand and rates across other Aave instances mirrored this trend. Borrow rates, which averaged 5.5–6.5% in August, have since shifted to the 5.0–6.0% range, consistent with the observed drop in utilization.

Under current market conditions, elevated Slope 1 is restrictive to marginal borrowing demand, constraining utilization below target levels. To re-establish equilibrium between supply and demand and enhance capital efficiency in a lower-yield environment, a downward adjustment of the Slope 1 parameter is proposed.

Recommendation

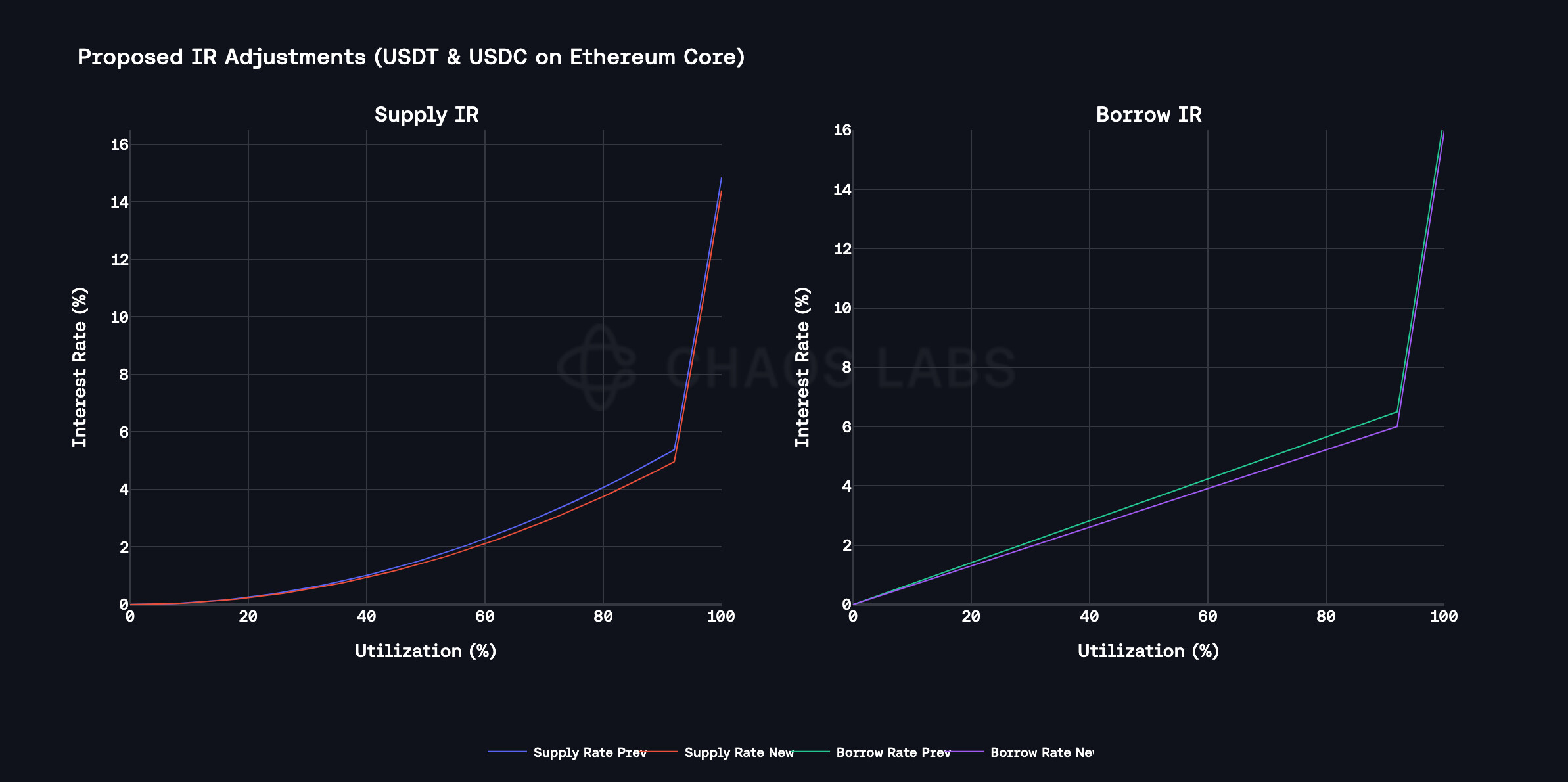

Given the moderation in stablecoin borrowing, we recommend reducing the Slope 1 across stablecoin markets on Aave V3 to restore utilization and capital efficiency. Lowering Slope 1 will better reflect current market yields, which have reduced borrower tolerance for higher rates, and help reverse the recent decline in utilization. This adjustment stabilizes borrowing demand and supports sustainable protocol revenue in a relatively lower-yield environment.

Please note that a set of stablecoins is excluded from the focus of this analysis. Such cases are: GHO, bridged stablecoins, stablecoins currently in the deprecation process, and others.

Specification

| Protocol | Instance | Asset | Current Slope1 | Recommended Slope1 |

|---|---|---|---|---|

| Aave V3 | Ethereum Core | USDC | 6.50% | 6.00% |

| Aave V3 | Ethereum Core | USDT | 6.50% | 6.00% |

| Aave V3 | Ethereum Core | USDe | 6.75% | 6.25% |

| Aave V3 | Ethereum Core | USDtb | 6.50% | 6.00% |

| Aave V3 | Ethereum Core | DAI | 6.50% | 6.00% |

| Aave V3 | Ethereum Core | pyUSD | 6.50% | 6.00% |

| Aave V3 | Ethereum Core | LUSD | 6.50% | 6.00% |

| Aave V3 | Arbitrum | DAI | 6.50% | 6.00% |

| Aave V3 | Arbitrum | USDT0 | 6.50% | 6.00% |

| Aave V3 | Arbitrum | USDC | 6.50% | 6.00% |

| Aave V3 | Optimism | DAI | 6.50% | 6.00% |

| Aave V3 | Optimism | USDT | 6.50% | 6.00% |

| Aave V3 | Optimism | USDC | 6.50% | 6.00% |

| Aave V3 | Base | USDC | 6.25% | 5.75% |

| Aave V3 | Metis | m.DAI | 6.50% | 6.00% |

| Aave V3 | Metis | m.USDC | 6.50% | 6.00% |

| Aave V3 | Metis | m.USDT | 6.50% | 6.00% |

| Aave V3 | Avalanche | DAI.e | 6.50% | 6.00% |

| Aave V3 | Avalanche | USDC | 6.50% | 6.00% |

| Aave V3 | Avalanche | USDt | 6.50% | 6.00% |

| Aave V3 | Avalanche | AUSD | 6.50% | 6.00% |

| Aave V3 | Gnosis | WXDAI | 6.50% | 6.00% |

| Aave V3 | Gnosis | EURe | 6.50% | 6.00% |

| Aave V3 | Gnosis | USDC.e | 6.50% | 6.00% |

| Aave V3 | BNB | USDC | 6.50% | 6.00% |

| Aave V3 | BNB | USDT | 6.50% | 6.00% |

| Aave V3 | BNB | FDUSD | 6.50% | 6.00% |

| Aave V3 | Scroll | USDC | 6.50% | 6.00% |

| Aave V3 | ZkSync | USDC | 6.50% | 6.00% |

| Aave V3 | ZkSync | USDT | 6.50% | 6.00% |

| Aave V3 | Linea | USDC | 6.50% | 6.00% |

| Aave V3 | Linea | USDT | 6.50% | 6.00% |

| Aave V3 | Celo | USDT0 | 6.50% | 6.00% |

| Aave V3 | Celo | cUSD | 6.50% | 6.00% |

| Aave V3 | Celo | USDC | 6.50% | 6.00% |

| Aave V3 | Celo | cEUR | 6.50% | 6.00% |

| Protocol | Instance | Asset | Current Base | Recommended Base |

|---|---|---|---|---|

| Aave V3 | Plasma | USDT0 | 2.50% | 2.00% |

| Aave V3 | Plasma | USDe | 2.50% | 2.00% |

Next Steps

We will move forward and implement these updates via the Risk Steward process.

Disclosure

Chaos Labs has not been compensated by any third party for publishing this AGRS recommendation.

Copyright

Copyright and related rights waived via CC0.