Summary

LlamaRisk supports listing PT-USDe-09APR2026 and PT-sUSDe-09APR2026 on the Aave Plasma instance. At the time of this analysis, the assets mature in approximately 117 days.

While the TVL in these specific April maturity pools is significantly lower than previous maturities ($1.34M for sUSDe and ~$446k for USDe), the Ethena ecosystem remains a dominant force in the market. The onboarding of these assets allows users to lock in fixed rates and provides a natural rollover destination for liquidity exiting maturing pools. Given the early stage of these specific pools (deployed on December 9th), we recommend conservative initial supply caps.

Assessment of PT base asset: Link

Assessment of Pendle PTs: Link

Considered PT asset maturities: PT-USDe-09APR2026, PT-sUSDe-09APR2026

Asset State

Asset Growth

Ethena’s USDe supply has recently seen a consolidation. The total supply of USDe is now at 6.561 billion. A significant portion of this is staked as sUSDe, with the total supply of the yield-bearing sUSDe reaching over 3.55 billion, reflecting a staking ratio of approximately 54.25%.

Source: LlamaRisk Ethena Risk Portal, December 12, 2025

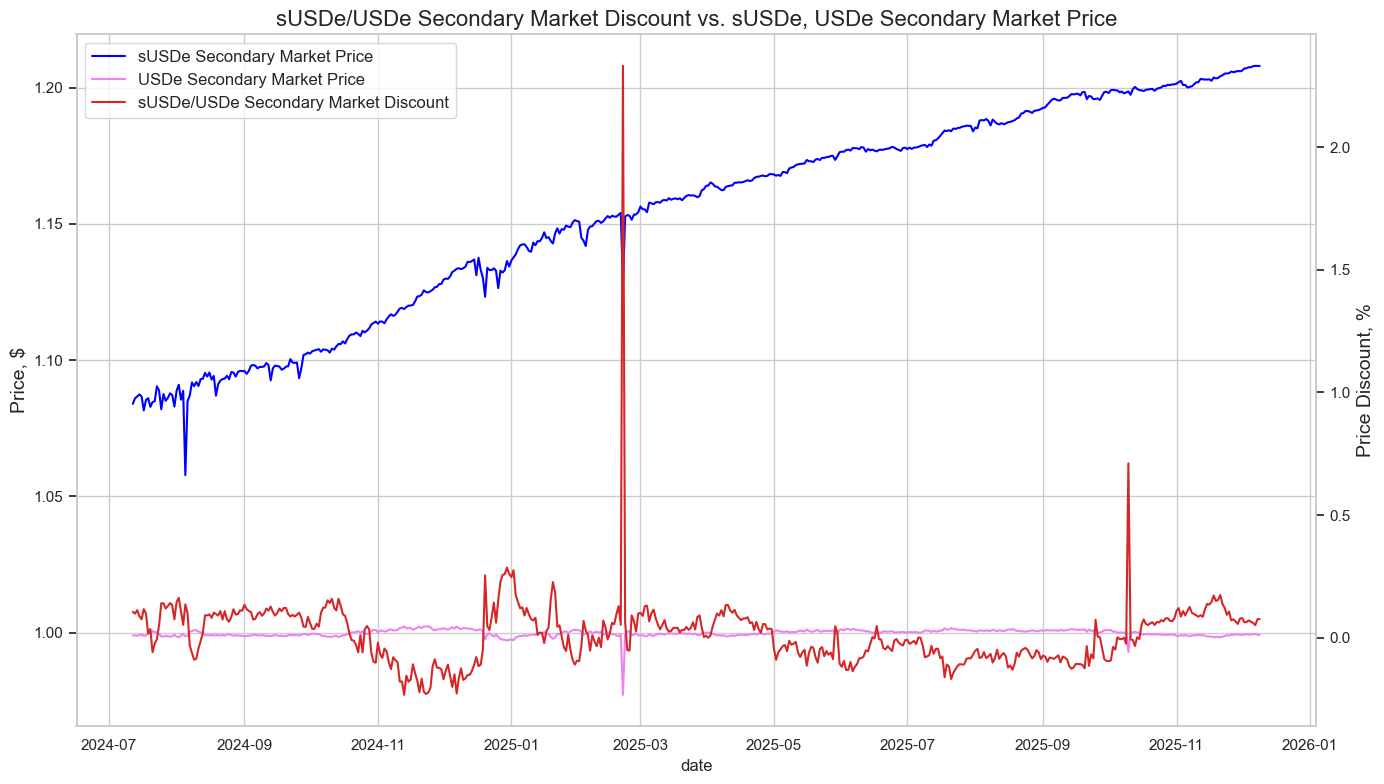

Underlying Stability

The market price of USDe remains pegged to $1.00, with no significant deviations from the peg since the 10/10 market crash. From a protocol health perspective, Ethena maintains a solvency ratio of 101.64% and is supported by a Reserve Fund capitalized at over $62.07 million. The historical price chart shows the peg’s stability.

Source: LlamaRisk, December 12, 2025

Underlying Yield Source

The primary incentives for holding USDe and sUSDe are the Ethena “sats” program and the native yield from sUSDe. The sats system provides users with multipliers for different activities.

- USDe deposited on Pendle generates a sats multiplier.

- sUSDe deposited on Pendle generates a sats multiplier on top of its underlying yield.

Market Analysis

Total Supply

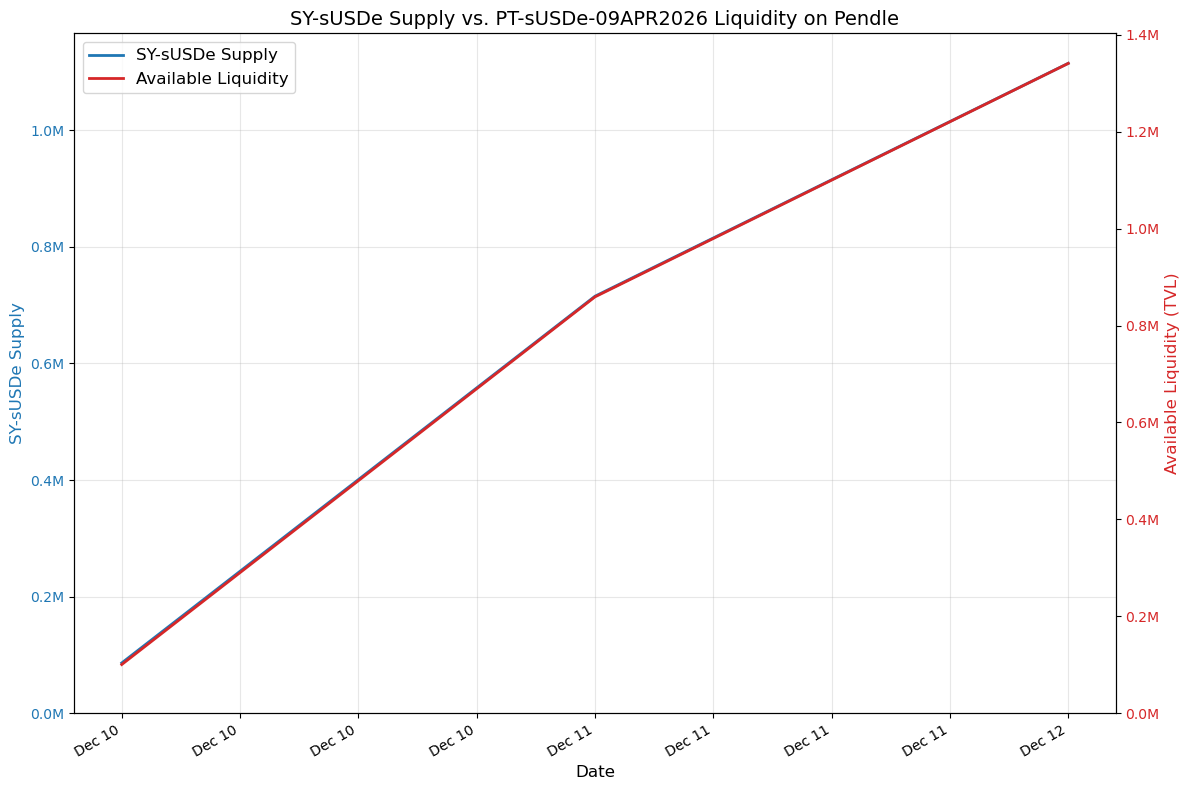

Both the PT-sUSDe-09APR2026 and PT-USDe-09APR2026 maturity pools have demonstrated linear growth since their inception. Analysis of the pools’ liquidity reveals a slow bootstrapping process, with total liquidity significantly lower than that of established pools, as users are just beginning to rotate into this maturity. This is in line with the current yield conditions and the short time since the pools’ deployment.

PT-sUSDe-09APR2026 Liquidity Growth:

PT-USDe-09APR2026 Liquidity Growth:

Source: LlamaRisk, December 12, 2025

Pool Composition

As of December 12, 2025, the composition of the pools is as follows:

- PT-USDe Pool:

- Total Liquidity: ~$445,916

- SY USDe: $393,838 (88.32%)

- PT USDe: $52,078 (11.68%)

Source: Pendle, December 12, 2025

- PT-sUSDe Pool:

- Total Liquidity: ~$1.34M

- SY sUSDe: $1.15M (85.68%)

- PT sUSDe: ~$190k (14.32%)

Source: Pendle, December 12, 2025

These liquidity levels indicate a nascent market for this specific maturity, which justifies conservative parameters initially.

Price and Yield

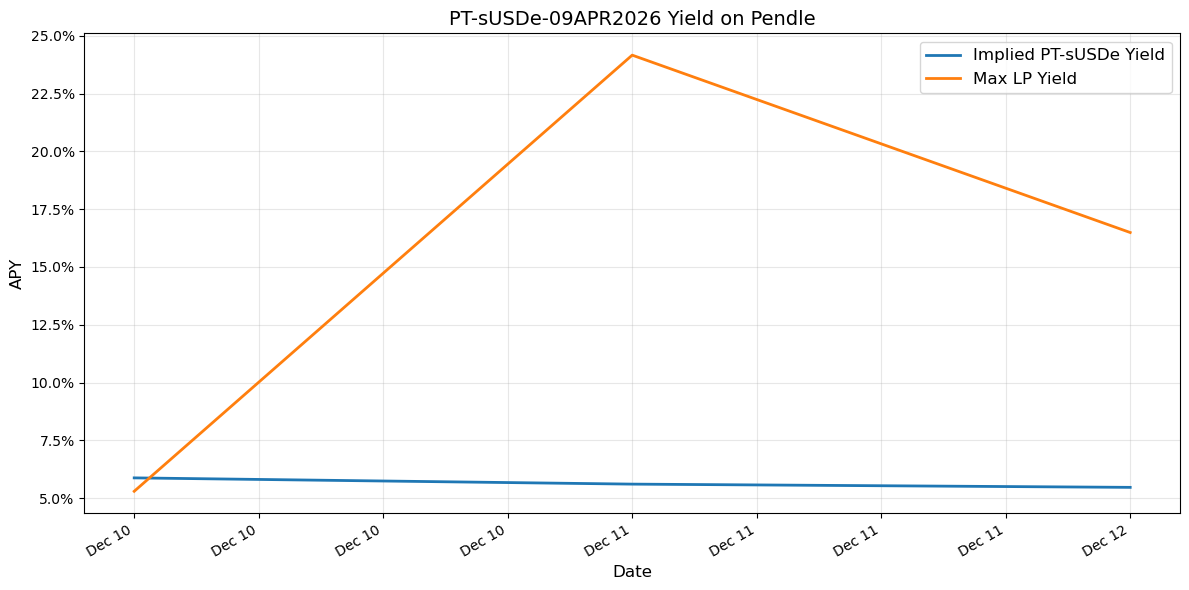

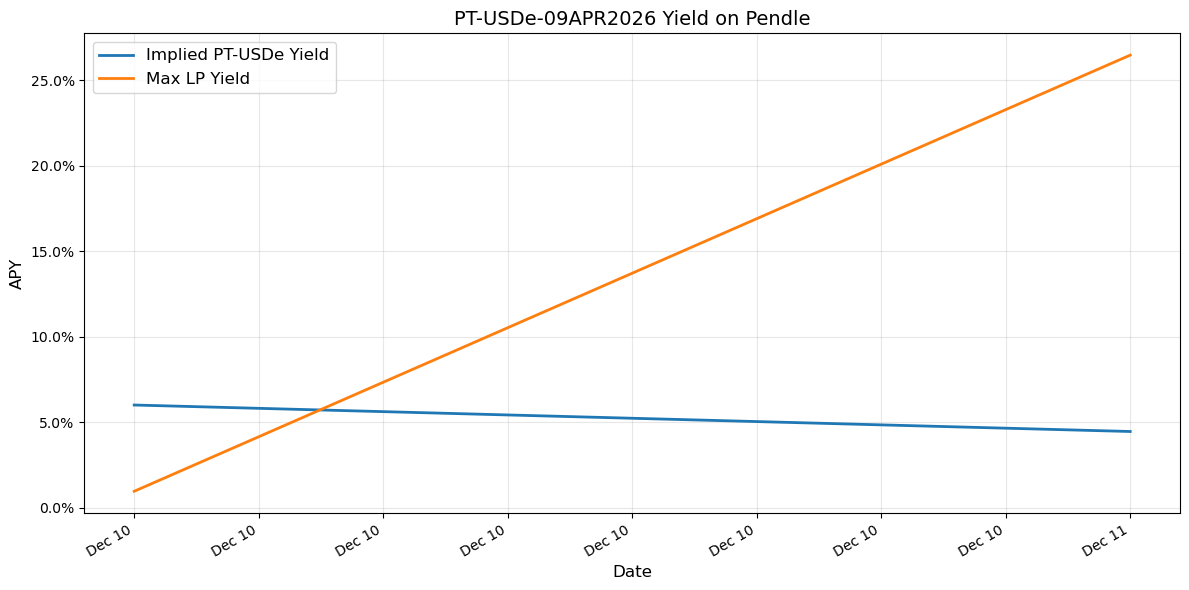

The implied yields for PT-USDe and PT-sUSDe reflect the market’s discount rate on the underlying assets.

PT-sUSDe Yield: The implied yield has remained relatively flat, hovering around 5.5%, while the Max LP yield has shown significant volatility, peaking near 25%.

PT-USDe Yield: The implied yield for the USDe PT is currently sitting slightly lower, around 4.5%.

Source: LlamaRisk, December 12, 2025

As of this review (117 days to maturity), the implied yields are:

- PT-USDe: ~4.36% Fixed APY

- PT-sUSDe: ~5.47% Fixed APY

The current yield level leaves a tight spread between the current 4% borrow rate and the PTs’ yield, potentially leading to limited demand for the PTs as collateral for looping.

Pool Parameters

The pools have the following parameters on Pendle:

PT-USDe

- Maturity: 09 April 2026

- Liquidity Yield Range: 3.5% - 25%

- Input Tokens: USDe

- Maker Fee: 0%

- Taker Fee: 0.08% (via AMM) / 0.1% (via Orderbook)

PT-sUSDe

- Maturity: 09 April 2026

- Liquidity Yield Range: 3.5% - 25%

- Input Tokens: sUSDe

- Maker Fee: 0%

Taker Fee: 0.07% (via AMM) / 0.1% (via Orderbook)

Maturities

The availability of the April maturity allows for the continued rollover of exposure for Aave users as the earlier PT pools reach maturity. The existence of overlapping maturities (Jan, April) ensures users have constant access to fixed-rate products.

Source: Pendle Plasma Markets, December 12, 2025

Integrated Venues

PT-USDe-09APR2026 and PT-sUSDe-09APR2026 are not yet integrated into other lending venues due to the recency of the pools. This represents a first-mover advantage for Aave to capture the primary lending demand for these assets.

Recommendations

Market Parameters Recommendation

We are aligning the risk parameter recommendations for the PT-USDe-09APR2026 and PT-sUSDe-09APR2026 listings with @ChaosLabs.

Price Feed Recommendation

For pricing both PT tokens on Aave, a specific dynamic linear discount rate oracle has been developed by BGD Labs. It is recommended that both PT-USDe-09APR2026 and PT-sUSDe-09APR2026 tokens be priced using it. We also recommend setting a more expansive maxDiscountRatePerYear value in order to account for an unexpected but possible yield reversal.

Disclaimer

This review was independently prepared by LlamaRisk, a DeFi risk service provider funded in part by the Aave DAO. LlamaRisk serves as a member of Ethena’s Risk Committee and an independent attestor of Ethena’s PoR solution. LlamaRisk did not receive compensation from the protocol(s) or their affiliated entities for this work. The information should not be construed as legal, financial, tax, or professional advice.