Summary

LlamaRisk supports listing PT-USDe-05FEB2026 and PT-sUSDe-05FEB2026 on the Aave. At the time of this analysis, the assets mature in approximately 89 days. The reduction in the yield provided by Ethena’s USDe and its yield-bearing counterpart sUSDe has reduced demand for the PTs. However, it still remains significant, with currently $1.5B in the November PTs. Additionally, due to the more limited demand and the pools being newly deployed, their liquidity is currently limited, especially on the USDe PT; therefore, we recommend more conservative initial supply caps.

Assessment of Pendle PTs: Link

Considered PT asset maturities: PT-USDe-05FEB2026, PT-sUSDe-05FEB2026

Asset State

Asset Growth

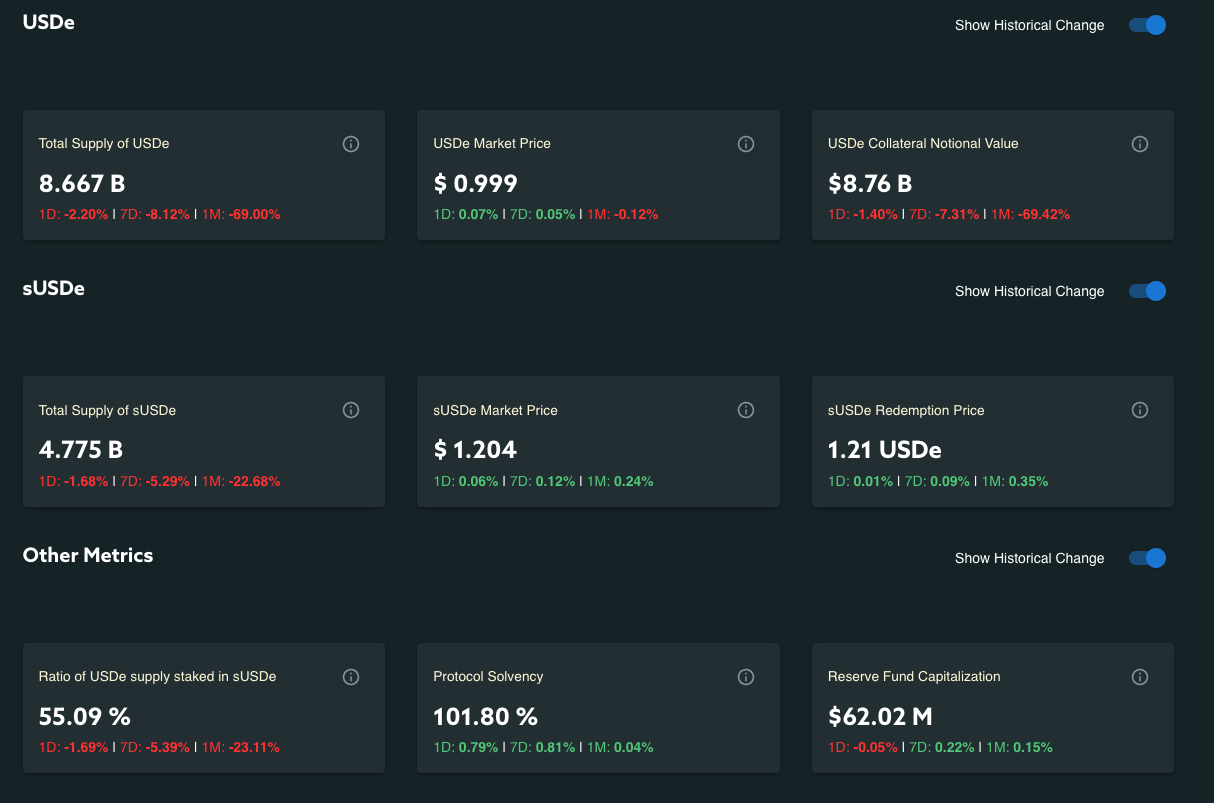

The Ethena USDe supply has suffered significant reductions in the last month, following the 10/10 crash, which led to large USDe liquidations on Binance and an overall shift in market sentiment, impacting both the sUSDe yield and $ENA price, which is directly related to the value of Ethena’s points. The total supply of USDe is now at 8.667 billion. A significant portion of it is staked as sUSDe, with the total supply of the yield-bearing sUSDe reaching over 4.7 billion, reflecting a staking ratio of approximately 55%.

Source: LlamaRisk Ethena Risk Portal, November 7, 2025

Underlying Stability

The stability of the underlying USDe peg and the overall health of the Ethena protocol are critical risk parameters. The market price of USDe remains pegged to $1.00. From a protocol health perspective, Ethena maintains a solvency ratio of 101.8% and is supported by a Reserve Fund capitalized at over $62 million. The historical price chart shows the peg’s stability, although it also reflects the brief de-peg of 65 basis points from the 10/10 market crash.

Source: LlamaRisk, November 7, 2025

Underlying Yield Source

The primary incentives for holding USDe and sUSDe are the Ethena “sats” program and the native yield from sUSDe. The sats system provides users with multipliers for different activities.

- USDe deposited on Pendle generates a 60x sats multiplier.

- sUSDe deposited on Pendle generates a 20x sats multiplier on top of its underlying yield.

Market Analysis

Total Supply

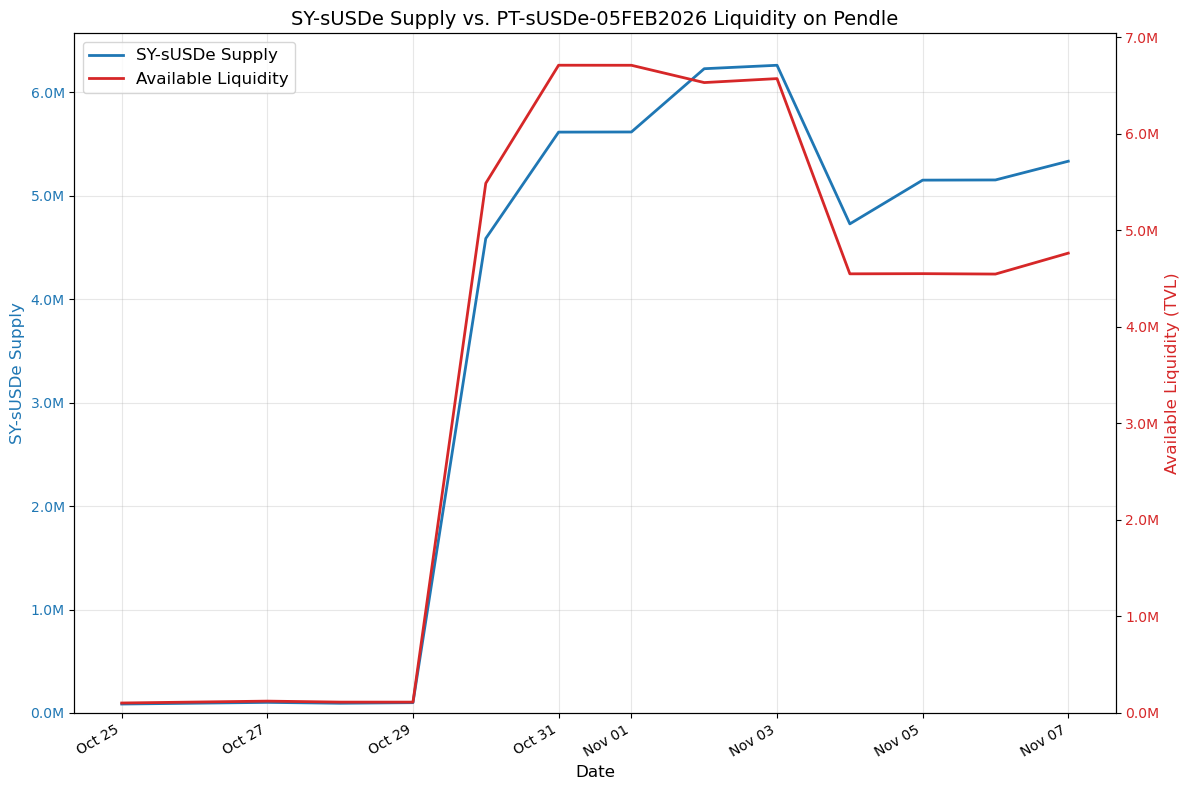

The PT-sUSDe-05FEB2026 maturity pool has demonstrated sustained growth since its inception, while the PT-USDe-05FEB2026 liquidity growth has been more limited. As the November PTs mature, we expect the liquidity to rotate to the February pools as has happened with previous PTs.

Source: LlamaRisk, November 7, 2025

Source: LlamaRisk, November 7, 2025

As of November 7, 2025, the composition of the pools is as follows:

- PT-USDe Pool:

- Total Liquidity: $1.5M

- SY USDe: $1.28M (83%)

- PT USDe: $250K (16.8%)

- PT-sUSDe Pool:

- Total Liquidity: $4.77M

- SY sUSDe: $3.9M (82.2%)

- PT sUSDe: $850K (17.8%)

These liquidity levels indicate a significant decline compared to past PTs, which may impact pool stability.

Source: Pendle, November 7, 2025

Source: Pendle, November 7, 2025

Price and Yield

The implied yields for PT-USDe and PT-sUSDe reflect the market’s discount rate on the underlying assets based on the opportunity cost of earning yield and sats. These rates have remained stable since the pool launch, if the yields for both PTs continue to fluctuate around the 6.3% and 6.6% respectively we expect to see more limited demand for borrowing due to the contraction of the spread between the Aave borrow cost and the PTs yield.

Source: LlamaRisk, November 7, 2025

Source: LlamaRisk, November 7, 2025

As of this review (89 days to maturity), the implied yields are:

- PT-USDe: ~6.3% APY

- PT-sUSDe: ~6.6% APY

The pools have the following parameters on Pendle:

PT-sUSDe

- Liquidity Yield Range: 3.5-25%

- Input Tokens: sUSDe

- AMM Fee: 0.09%

- Orderbook Fee: 0.12%

PT-USDe

- Liquidity Yield Range: 3.5-25%

- Input Tokens: USDe

- AMM Fee: 0.08%

- Orderbook Fee: 0.1%

Maturities

The availability of multiple maturities ensures a more natural rollover of the PT pools, which is also relevant for Aave’s exposure. With the onboarding of the February PTs when the November pool expires, users will be able to migrate.

Source: Pendle, November 7, 2025

Integrated Venues

PT-USDe-05FEB2026 and PT-sUSDe-05FEB2026 are not yet integrated into other lending venues due to the recency of the pools. This represents a significant first-mover advantage for Aave to capture the primary lending demand for these assets.

Recommendations

We are aligning the risk parameter recommendations for the PT-USDe-05FEB2026 and PT-sUSDe-05FEB2026 with @ChaosLabs.

Price Feed Recommendation

For pricing both PTs tokens on Aave, a specific dynamic linear discount rate oracle has been developed by BGD Labs. It is recommended that both PT-USDe-05FEB2026 and PT-sUSDe-05FEB2026 tokens be priced using it.

Disclaimer

This review was independently prepared by LlamaRisk, a DeFi risk service provider funded in part by the Aave DAO. LlamaRisk serves as a member of Ethena’s Risk Committee and an independent attester of Ethena’s PoR solution. LlamaRisk did not receive compensation from the protocol(s) or their affiliated entities for this work. The information should not be construed as legal, financial, tax, or professional advice.