Summary

This publication introduces @TokenLogic and @kpk as the DAO’s Financial Service Provider for an initial period of 180 days, with a proposed budget of 400k GHO. The scope of contribution will span the following areas of the DAO’s finances:

- Treasury Management;

- Strategic Assets’ Liquidity; and

- Safety Module.

The combined karpatkey and TokenLogic team presents an unparalleled offering of specialized skills and proven technical expertise, with a network that spans most of DeFi.

Motivation

Treasury Management

Aave is the leading cross-chain lending protocol by all relevant KPIs i.e. TVL, supplied; and borrowed assets. With the latest version (v3) present on 10 networks, Aave Protocol currently generates revenue across ten networks and 18 deployments (v1, v2 incl. Centrifuge and ARC, v3 incl. Spark), consolidating a cross-chain treasury that’s currently worth around $130M.

In spite of having a significantly sized treasury, the Aave DAO faces mainly three challenges with its current treasury composition and operational practice.

Portfolio Volatility

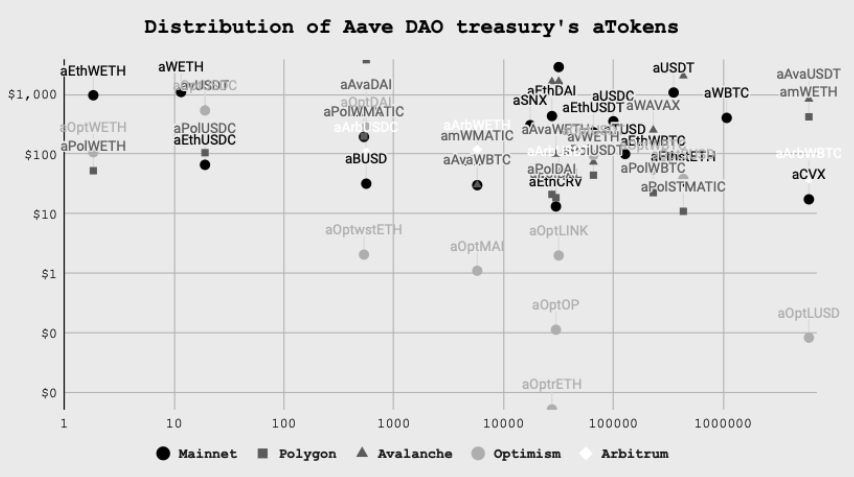

A significant portion of the treasury is held in the DAO’s native token (AAVE) which currently has limited DeFi utility and introduces volatility in the overall treasury value. The following chart illustrates the treasury allocation across various crypto assets.

Asset Dispersion

Treasury funds are dispersed around multiple collector contracts deployed in different blockchains. These funds are a direct result of how the protocol captures value and are mostly denominated in aTokens (~61) according to market activity, which requires constant rebalancing to meet expense requirements. This activity has historically been carried out through the governance processes, lacking comprehensive and up-to-date data on portfolio composition and rationale for asset allocation.

The DAO has only recently gained the ability to move funds between Polygon and Ethereum, while all other Treasuries are isolated, often leading to missed opportunities for leveraging the DAO’s funds. These opportunities are crucial for enhancing and capitalizing on synergies within the Aave ecosystem, including GHO management and the Safety Module.

Runway

According to the latest forecasted expenses, the DAO’s 12-month budget is over $19M.

| Category | Budget $k | Duration (mths) | Annualized Budget |

|---|---|---|---|

| Security¹ | $1,500 | 6 | $3,000 |

| Risk Management | $1,600 | 12 | $1,600 |

| Bug Bounty | $1,000 | 12 | $1,000 |

| Gov. Delegates | $30 | 1 | $360 |

| Fin. Serv. Providers | $400 | 6 | $800 |

| Marketing | $550 | 3 | $2,200 |

| GHO Liq. Committee | $450 | 3 | $1,800 |

| Growth ACI II | $375 | 6 | $750 |

| Aave Grants DAO² | $1,320 | 6 | $2,640 |

| Development | $2,486 | 6 | $4,973 |

| Total | $19,123 |

Note:

- Certora only.

- AGD figures based on discussions with the team.

While there are ongoing plans to secure part of this amount of stablecoins, most of it is allocated in high utilization Aave lending markets. Although reckoning the strategic rationale, holding most of the assets in the DAO’s own protocol exposes the portfolio to excessive risk in a volatility event scenario e.g. exploit.

With the aim to support the protocol’s self-sustainability, treasury management should aim to reduce long tail asset exposure, ensure a 12-month financial runway and a stablecoins allocation that balances servicing Aave users and the DAO’s capital preservation.

GHO Development

Aave developed GHO as a stablecoin native to the ecosystem and controlled by Aave Governance that enables a new level of transparency and censorship resistance. Technically, GHO is a collateral-backed stablecoin minted by users who lock up collateral assets in Aave’s v3 protocol. The protocol uses smart contracts to manage the issuance and burning of the token through allow-listed entities called Facilitators, whose capacity to mint GHO (bucket) is enabled by Aave’s governance.

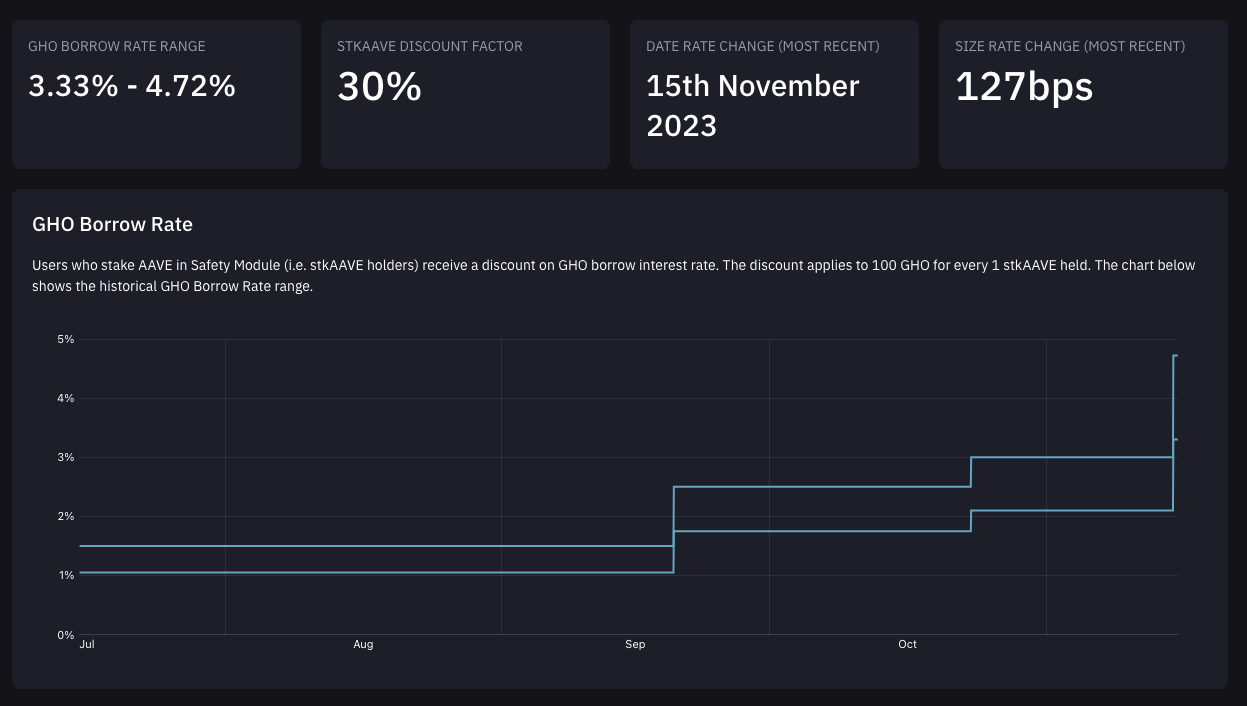

Aiming to enable committed AAVE token holders to capture additional value, GHO’s debt strategy introduces an innovative concept of rate discount by staking AAVE.

With an on-chain vote executed in July, Aave launched GHO with two Facilitators (Aave itself and GHO FlashMinter), a borrowing rate of 1.5%, and a discount rate of 30% for AAVE stakers. Since then, the borrowing rate has been increased to 4.72%.

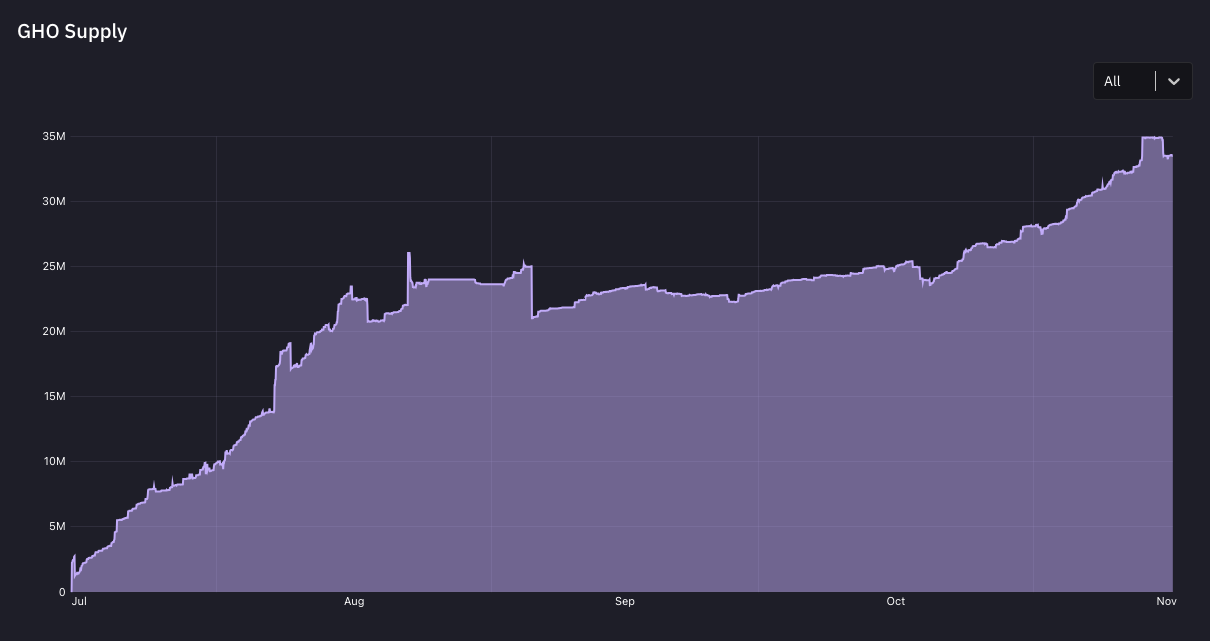

As demonstrated by GHO’s price chart, the most immediate challenge the Aave community is facing is the persistent trading of GHO at a discount practically since deployment. This trend has been influenced by higher stablecoin-enabled market rates like MakerDAO’s Dai Savings Rate (DSR), creating a rate arbitrage opportunity. This cycle of borrowing and selling GHO harms GHO holders as it generates selling pressure, leading to a loss of value and eroding trust in GHO’s stability. It also encourages a speculative pattern among GHO minters motivated to borrow and dump the asset, followed by repurchasing at a lower price, further driving down its value.

For the long-term health and success of GHO, two more enduring aspects require the community’s attention:

Peg Mechanisms

There’s a crucial need for robust peg mechanisms tailored specifically for GHO that go beyond tactical borrow rate adjustments. Such mechanisms should be designed to help maintain GHO’s value relative to its peg, irrespective of broader market movements or temporary arbitrage opportunities. Effective peg maintenance strategies will provide the dual benefits of protecting GHO’s value in turbulent market conditions and reinforcing its utility as a stable and reliable medium of exchange within the DeFi ecosystem, thus addressing the core issue of price stability head-on.

Demand

The second one is generating organic demand that leads to an increased supply, mainly demand vectors external to the platform, but also including growth rooted in value-generating activities within the DeFi ecosystem. Without these value-generating flows, GHO faces the risk of remaining underutilized, hampering both its adoption and functionality as a stablecoin meant to facilitate economic activity.

Currently, external demand for GHO has predominantly centered around its exchange for USD tokens and liquidity provision. While providing liquidity has been the sole avenue for yield generation, there has been a noticeable decrease in the allocated GHO liquidity recently.

Safety Module

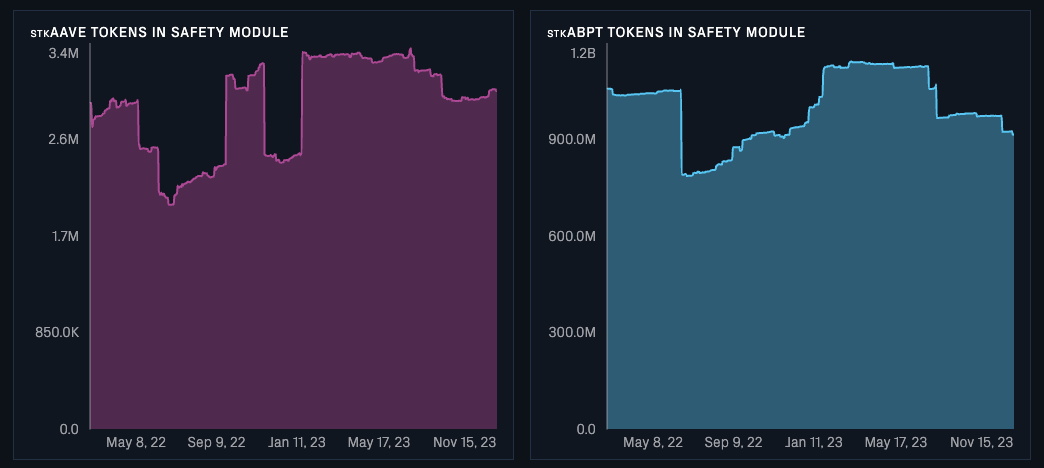

The Aave Safety Module (SM) provides the DAO with an insurance-like fund expected to repay users of lost funds resulting from Aave’s smart contract exposure. The current composition of the insurance fund is overweight AAVE to the point where there exists a negative feedback loop between potential Bad Debt exposure and the AAVE token price.

If a Short Fall event was to occur, speculators could frontrun the AAVE auction, potentially even trigger liquidations on Aave Protocol, and cause the auction to occur at a lower than otherwise AAVE price. This unintentional feedback loop can be partially mitigated by modifying the safety module fund with the introduction of additional assets over time.

Furthermore, the previously outlined negative feedback loop involving AAVE’s price, liquidations, and bad debt results in a high cost for utilizing AAVE tokens. Consequently, it is necessary to reevaluate the incentivization of liquidity in the Safety Module, aiming for a more efficient allocation of DAO funds.

The daily cost of sustaining the SM is estimated to be approximately 100k USD per day at the prevailing AAVE distribution rate and market price. If all the AAVE and B-80AAVE-20wETH can be auctioned off at spot prices, the insurance funds coverage ranges from 1.7% to 3.2% of TVL over the last 18 months. For each $1 of coverage provided, the Aave DAO is paying approximately 31 cents each year. With a reduction in AAVE rewards, as proposed here, the costs of sustaining the insurance fund will be reduced.

Why Partnering?

All of the topics mentioned above are deeply connected. Most of the assets contained in the treasury derive their value partly from their liquidity and the protocol’s security; the Safety Module’s effectiveness relies on attracting external capital through LP incentives; and GHO’s peg mechanism is dependant on liquidity, which could be incentivized using the treasury’s holdings.

There hasn’t been a holistic approach to these core activities of Aave DAO’s financials so far, which ultimately has led to uncoordinated and inefficient decision-making processes.

TokenLogic and karpatkey are partnering to provide Aave DAO with a comprehensive financial service solution. This partnership leverages:

- Over three years of experience in advancing the Aave Protocol through a pivotal role in feature development and product adoption; and

- A distinguished history of contributing to the most respected DAOs in the industry through specialized financial services.

The combined expertise of our teams is deeply rooted in the Aave ecosystem and extends across its community.

TokenLogic

We are a proactive team that puts our partners’ needs first. Our developers are already actively contributing to the Aave Protocol, 23 AIPs to date. We believe in Aave’s incremental improvement process and building solutions that enable the DAO to manage its finances efficiently whilst minimizing external dependencies.

Our dedication was demonstrated when we presented a proposal to improve the Aave DAO’s runway and built a preliminary frontend for the community. Our analysis will continue to showcase the interactive and transparent theme of the GHO Analytics platform. The refined scope primarily focuses on Treasury Management, GHO Liquidity/adoption and the Safety Module.

karpatkey

karpatkey is a DeFi-native organization specializing in professional DAO finance through industry-leading research and tooling since 2020. We’ve been working with GnosisDAO, Balancer, ENS, CoW Protocol, and Lido on financial planning, operations, and strategy, diversifying their treasuries into sustainable portfolios of DeFi investments designed to support DAOs in executing their missions. Check out our values to understand a bit more about our guiding and decision-making principles.

As DAO treasury developers, we contributed to some of the most reputable DeFi protocols in our industry. We supported the adoption of xDAI across Gnosis Chain, paving the way for the deployment of sDAI that boosted chain TVL and consolidated a stablecoin hub with the integrations like Angle and Spark. Our extensive experience provided us with advanced practical knowledge on DeFi primitives like stableswap and concentrated liquidity AMMs, liquidity, and voting incentives, veTokenomics, leverage and lending platforms, and integrations with top protocols.

In addition to being an active Aave delegate with more than 90 governance votes since August 7th, we’ve contributed to the development of an Aave fork project and historically deployed, borrowed, and staked a combined $26.51M worth of LP positions in both Aave V2 and V3.

We now believe we can meaningfully contribute to solidifying Aave’s position as the leading DeFi lending protocol, not only through domain expertise but mostly through pushing positive-sum initiatives with the DAOs we work with.

Specification

This proposal outlines a collaborative framework between TokenLogic and karpatkey to manage the Aave DAO’s treasury. Both parties will work in unison to ensure any future proposals within the agreed scope are jointly developed and endorsed.

Architecture for Asset Management Tooling

We aim to define and implement a robust architecture for asset management. At a high level, this architecture will enable non-custodial asset management, incorporating role-based access controls preapproved by the community that will enable treasury diversification and yield optimization. This system will ensure the Aave DAO retains full control over fund retrieval and permission management, facilitated through Aave’s “shortExecutor”. All designs will be aligned with Aave best practices, and will encompass required steps to update existing infrastructure (e.g. SAM).

As the architecture for treasury management is being developed, the TokenLogic and karpatkey partnership will diligently progress with the necessary treasury operations, aligning them with the needs of the DAO and the stipulations of this proposal. All activities will be conducted in accordance with the established AIP model to avoid any disruptions.

Financial Security

A key objective is to secure sufficient funds to ensure a one-year runway, aligning with the DAO’s known budget and anticipated expenses as shared above. This approach guarantees financial stability and an operational continuity for Aave DAO.

Key components of this objective will include:

- Bridging Aave funds from other blockchains to consolidate them in Ethereum;

- Migrating primary stablecoin funds from Aave v2 to Aave v3 for improved experience in using aTokens as payments; and

- Swapping secondary stablecoins in mainnet prioritizing GHO.

Do note, Financial statements have been omitted in order to present a cost conscious, high-impact solution within the current budget. If the Aave DAO wishes to explore having financial statements as part of a broader proposal, we can later expand the funding to include the additional scope.

As it currently stands, all necessary preparation for incorporating financial statements as part of the earlier TokenLogic proposal has been paused due to overall Aave budget considerations.

Formation of the Aave Liquidity Committee

This expanded committee will oversee the management of liquidity incentives and Aave-owned liquidity in alignment with Aave’s strategic asset goals. One of the main focus areas will be supporting GHO’s token price recovery. Key initiatives include:

- Foster concentrated liquidity profiles that support GHO’s price movement towards re-pegging, while maintaining its utility across a full range AMMs.

- Utilize Maverick’s design to automate liquidity concentration as prices evolve, while reducing the friction caused by liquidity fragmentation in concentrated boosted pools.

- Optimize incentives on Uniswap v3 for concentrated liquidity, tailored across three categories: fees, GHO, and other USD token liquidity. Prioritize USD liquidity, particularly when GHO is off-peg.

- Continuously review and adjust incentives on platforms that yield the best results.

- Initial focus is on skewed liquidity distribution to support regaining the peg. However, it is paramount to ensure existing liquidity providers find sufficient utility on their GHO funds (through sustainable strategies that make use of Aave’s AURA holding) to mitigate selling pressure.

- Post-Repeg Strategy for GHO, explore sustainable approaches that preserve the token’s value and expand its functional role within the ecosystem:

- Implement optimized liquidity strategies through Maverick and Merkl to achieve balanced liquidity and deeper market depth.

- Enhance GHO’s extrinsic demand by incentivizing stableswap pools, such as Balancer’s GHO pools, leveraging Aave’s capacity for a significant TVL increase.

- Work with Gyroscope to deploy liquidity pools that align with Balancer’s architecture, using their advanced bonding curve model for concentrated liquidity AMMs. This strategic integration will use Aave-owned AURA to enhance GHO’s price stability.

- Deploy and incentivize markets beyond USD-pegged assets, including ETH, ETH LSTs, EUR, and Real World Assets (RWAs). This diversification will open up new investment avenues and attract liquidity providers with varying risk appetites.

- Collaborate closely with Aave and specialized risk service providers to support the deployment and configuration of the GHO Stability Module (GSM). This coordination will focus on fine-tuning critical parameters, taking into account prevailing market conditions. Our objective is to integrate the GSM with managed capacity, potentially even before GHO achieves full re-pegging, as a strategic mechanism to foster price stability.

- To optimize the utilization of surplus votes resulting from incentivized liquidity, we propose to leverage excess voting power effectively, transforming it into tangible rewards through participation in voting markets such as Curve, Convex, Balancer, and Aura.

For operational simplicity and alignment with the DAO’s strategic objectives, evolving the GHO Liquidity Committee into the Aave Liquidity Committee is a logical step. The proposed change involves updating the multisig to replace @Dydymoon with @Sisyphos (karpatkey), reflecting our commitment to this new direction.

| Signer | Address |

|---|---|

| Matthew Graham (TokenLogic) | 0xb647055A9915bF9c8021a684E175A353525b9890 |

| Emilio (Avara) | 0x9C3E82658d10064121048A21c69978D3400abb25 |

| Marc (Aave Chan Initiative) | 0x329c54289Ff5D6B7b7daE13592C6B1EDA1543eD4 |

| Solarcurve (Balancer) | 0x512fce9B07Ce64590849115EE6B32fd40eC0f5F3 |

| Sisyphos (karpatkey) | 0x818c277dbe886b934e60aa047250a73529e26a99 |

| Figue (Paladin) | 0x009d13E9bEC94Bf16791098CE4E5C168D27A9f07 |

| TokenBrice (DeFi Collective) | 0xAA7A9d80971E58641442774C373C94AaFee87d66 |

All transactions impacting Aave collectors or other smart contracts will adhere to the standard AIP process for execution.

Diversification and Yield Optimization

In order to secure the protocol’s runway from platform risks, streamline the DAO’s capacity to meet future cash flows, and generate additional risk-adjusted returns, our initial set of recommendations consists of:

- Continue optimizing Aave supplied liquidity to ensure capital availability and allocation while lending markets are kept operational with effective interest rates on the edge.

- Where volatile non-ETH and non-AAVE assets with little DeFi utility can be withdrawn without substantially increasing the interest rate, the possibility of increasing the stablecoin funds should be explored.

- A second flow of yield will be unlocked by improving current asset allocation to risk-adjusted yield-generating DeFi strategies. We recommend initially exploring the following DeFi strategies:

- Withdraw ETH from Aave markets where possible and stake in LST protocols.

- Review options within Aave’s legal framework and strategy to further diversifying stablecoins for RWA yield, either through existing strategies, or exposed assets like Backed, Ondo, or Angle. These strategies will have to strike the right balance between generating yield and allocating treasury funds to support GHO demand.

Safety Module

As part of the scope, karpatkey and TokenLogic will focus on modeling the SM performance during shortfall events and present proposals to diversify asset categories. This proposal will feature how the DAO can utilize the vlAURA position, realize synergies between GHO Liquidity and overall attempt to reduce the DAOs insurance fund spend.

The below outlines at a high level what we intend to deliver:

- Introduce additional asset categories to the SM to promote diversification and reduce the dependence on AAVE as a backstop for the protocol. The initial parameter configuration will incorporate feedback from @ChaosLabs. We will explore the feasibility of including GHO LP assets and harness rewards from other protocols. In developing such a strategy, the technical lift will be performed by @bgdlabs with a security audit by Certora and/or Sigma.

- A 90-day emission forecast will be shared ahead of each emission cycle for community feedback and the expense will feature in the DAOs runway analysis. The iterative approach to SM emissions will enable the DAO to target specific asset categories in an attempt to improve the correlations between bad debt potential whilst maintaining a base level of insurance. The proposal will feature the ability to reward some categories with non AAVE rewards, like GHO, to support adoption and velocity.

- Focus on capital efficiency, over time the SM categories rewards will be optimized to balance attracting and retaining new deposits for each respective category. For example the APR on stkAAVE is expected to continue being reduced given the recent GHO Mint Discount utility being added and the introduction of new categories.

- Complimenting the efforts above a dashboard will be maintained that tracks the effective coverage of the insurance fund under various market conditions. The deposit value, composition of assets, APR over time and impact on the DAOs runway will all be readily available for the community to view. This is expected to create transparency and provide insight into the performance of the SM as an effective insurance fund for the DAO.

Implementation

The execution of this proposal requires funding, which has been incorporated into the existing budget projections. The allocation for this initiative will be streamlined into a dedicated budget stream as part of this proposal. The budget allocation is meticulously planned to cover all aspects of the proposed activities, ensuring that the Aave DAO’s financial resources are utilized effectively and transparently.

The AIP will call the createStream() method of the IAaveEcosystemReserveController interface to create two 180-day streams for 220k and 180k of GHO.

- The following address will be the recipient of the 220k GHO stream:

- Address:

0x58e6c7ab55aa9012eacca16d1ed4c15795669e1c

- Address:

- The following address will be the recipient of the 180k GHO stream:

- Address:

0x3e4A9f478C0c13A15137Fc81e9d8269F127b4B40

- Address:

Afterwards, both karpatkey and TokenLogic will be able to periodically claim a fraction of the budget for the duration of the stream.

Similar to ACI, both karpatkey and TokenLogic are to be included in the Gas Rebate program that reimburses on-chain voting, calling revenue contracts and deployment costs.

TokenLogic and karpatkey both commit to not receiving any funds from other entities for creating proposals and publishing AIPs on Aave Protocol.

Disclaimer

TokenLogic and karpatkey receive no compensation beyond Aave protocol for the creation of this proposal. TokenLogic and karpatkey are both delegates within the Aave ecosystem.

Next Steps

As we progress with the proposal to manage Aave DAO’s treasury, it is crucial to engage in a structured and transparent process. To move forward effectively, the following steps will be taken:

-

Gather Community Feedback: this step is vital for ensuring that the proposal resonates with community interests and perspectives.

-

Following sufficient community engagement and feedback, we will conduct a Snapshot vote to gauge the community’s stance on this proposal.

-

Concurrently, we will post the Aave Request for Comment (ARFC), detailing the specifics of the proposal for further community review and input.

-

After the ARFC is shared, a Snapshot vote on the ARFC will be conducted.

-

Subsequent to the Snapshot votes, an On-Chain vote will be held with the right payload to:

-

Deploy the Stream, effectively initiating the proposed treasury management strategy.

-

Implement changes in Aave Liquidity Committee multisig, including the transaction payload. This step is essential for operationalizing the committee’s revised structure and responsibilities.

Each of these steps is designed to ensure that the proposal is thoroughly vetted and aligns with the community’s vision for Aave DAO’s future.

Copyright

Copyright and related rights waived via CC0.