Summary

A proposal to:

- Increase supply cap for PT-USDE-25SEP2025 on the Ethereum Core instance

- Increase supply cap for tBTC on the Ethereum Core instance

- Increase borrow cap for BTC.b on the Avalanche instance

- Increase borrow cap for CELO on the Celo instance

- Increase supply and borrow caps for USDC on the Linea instance

- Increase supply cap for wS on the Sonic instance

All cap increases are backed by Chaos Labs’ risk simulations, which consider user behavior, on-chain liquidity, and price impact, ensuring that higher caps do not introduce additional risk to the platform.

Our recent research paper, “Stress Testing Ethena: A Quantitative Look at Protocol Stability,” examines how rapidly growing deposits of Ethena’s USDe, sUSDe and especially Pendle Principal Tokens are reshaping Aave’s collateral pool and funding dynamics. It maps out both on‑chain liquidity hazards (e.g., thin PT markets, leveraged looping, rehypothecation) and backing‑side tail risks (exchange or custodian failure, collateral de‑peg, prolonged negative funding) via scenario modeling and Monte‑Carlo simulations, while proving that Aave’s current risk‑oracle floors, eMode parameterization and liquidation controls would absorb most plausible shocks. The proposed cap increases reflect and incorporate the insights from this paper.

Finally, our most recent paper, “Aave’s Growing Exposure to Ethena: Risk Implications Throughout the Growth and Contraction Cycles of USDe ,” shows that contraction and stabilization dynamics within the Aave-Ethena ecosystem are closely linked. When sUSDe yields decline, leveraged positions unwind, freeing up significant stablecoin liquidity in Aave through repayments. Simultaneously, PT/USDe borrowers shift their debt into other stablecoins, generating upward price pressure on USDe precisely when redemption demand rises. Crucially, stablecoin repayments from leverage unwinders typically outweigh PT debt migration into stablecoins, creating a natural liquidity buffer. Our analysis indicates this dynamic effectively stabilizes Aave markets, comfortably absorbing potential stress even during Ethena’s withdrawal of backing assets. Overall, the current market structure supports increased exposure, provided backing deployment into Aave remains prudently managed. The proposed cap increases reflect and incorporate the insights from the aforementioned papers.

For more insight into how the PT Risk Oracle operates, please consult the following post and its follow up. In addition, the Risk Oracles outputs can be monitored live at the following page.

PT-USDE-25SEP2025 (Ethereum Core)

PT-USDE-25SEP2025 has reached its full supply cap of 1.4B, with an inflow of 600M on August 12th alone. This indicates persistent demand for collateralizing stablecoin looping positions.

Supply Distribution

PT-USDE-25SEP2025’s supply is moderately concentrated, with the largest supplier holding 7.5% of the total and the top 10 wallets collectively accounting for 50%. Health factors among these top suppliers are tightly clustered between 1.02 and 1.23, indicating a strong appetite for leverage. Most suppliers borrow stablecoins, and due to the design of USDe Principal Tokens, liquidation risk decreases over time as the PTs converge toward the underlying asset.

All assets borrowed against PT-USDE-25SEP2025 collateral are stablecoins, with USDe leading the market at over 50% share. This dominance is supported by USDe E-Mode, which enables higher leverage compared to other stablecoins such as USDT and USDC. Due to the PT oracle design and the high correlation between debt and collateral prices, liquidation risk remains minimal.

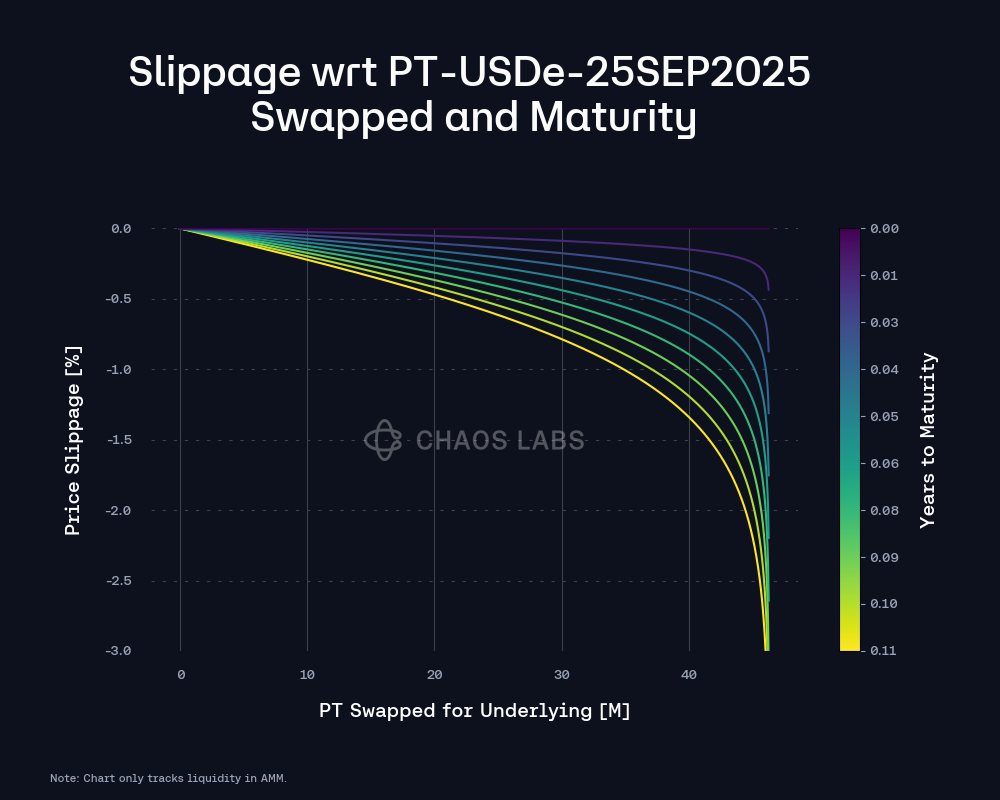

Liquidity and Market

As the PT’s market comes to maturity its AMM liquidity has increased significantly, at the moment is sufficient to facilitate a liquidation of 50M PT-USDE-25SEP2025, scaling considerably over the last few weeks.

The implied yield for the underlying has shown moderate volatility over the past two weeks, fluctuating between 12% and 16%, and is now stabilizing at around 14.8%.

Recommendation

Given the sustained demand, moderate supply concentration, minimal liquidation risk, strong AMM liquidity growth, and stable implied yield settling at 14.8%, we recommend increasing the PT-USDE-25SEP2025 supply cap by 400M. The currently constrained available stablecoin liquidity on the platform, stemming from large Justin Sun-linked withdrawals coupled with rate-agnosticity on the PT side and the expiry of the August PT-eUSDe, deems such a middle ground optimal.

tBTC (Ethereum Core)

tBTC has reached 93% of its supply cap at 2.04K tBTC; the borrow demand has increased slightly in recent weeks, while the overall utilization rate is at 5%.

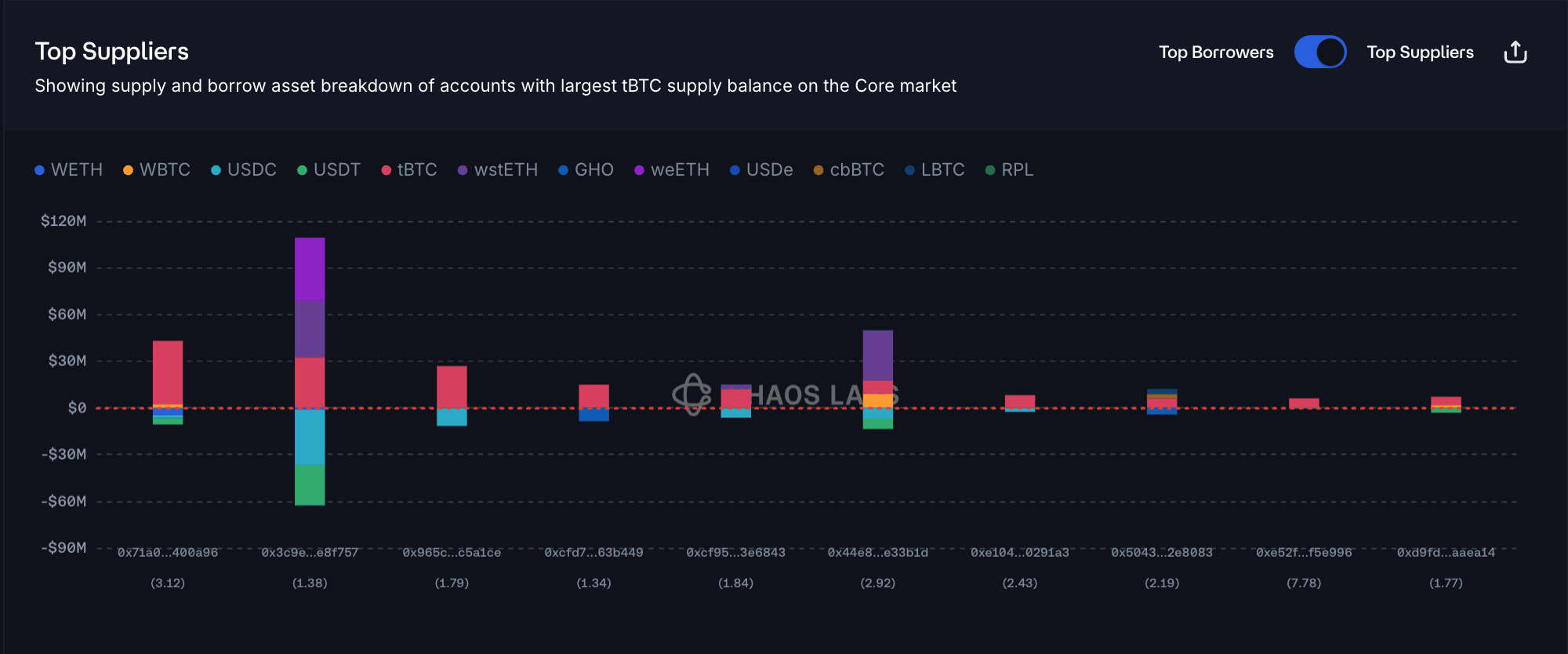

Supply Distribution

tBTC’s supply shows moderate concentration, with the top supplier representing 16% of the total and the top 7 wallets collectively holding 58%. Health factors for the top positions remain safe, ranging from a minimum of 1.38 to an average of 2-3. Additionally, most suppliers are borrowing stablecoins against the tBTC collateral, which, paired with high health factors, limits the liquidation risk.

Liquidity

tBTC’s liquidity has been stable over the past few months. At present, the slippage on a sell order of 100 tBTC would be limited to 2%, supporting a supply cap increase.

Recommendation

Given the strong demand for tBTC supply, sufficient liquidity to handle significant liquidations, and minimal underlying risk, we recommend increasing the supply cap by 400 tBTC.

BTC.b (Avalanche)

BTC.b on Avalanche has reached its borrow cap at 290/300 due to recent increases in borrowing activity over the past month, the borrowing demand has doubled. Additionally, the utilization is at 8.8%, suggesting that an increase of the borrow cap would provide suppliers with a greater yield while keeping the associated risks minimal.

Borrow Distribution

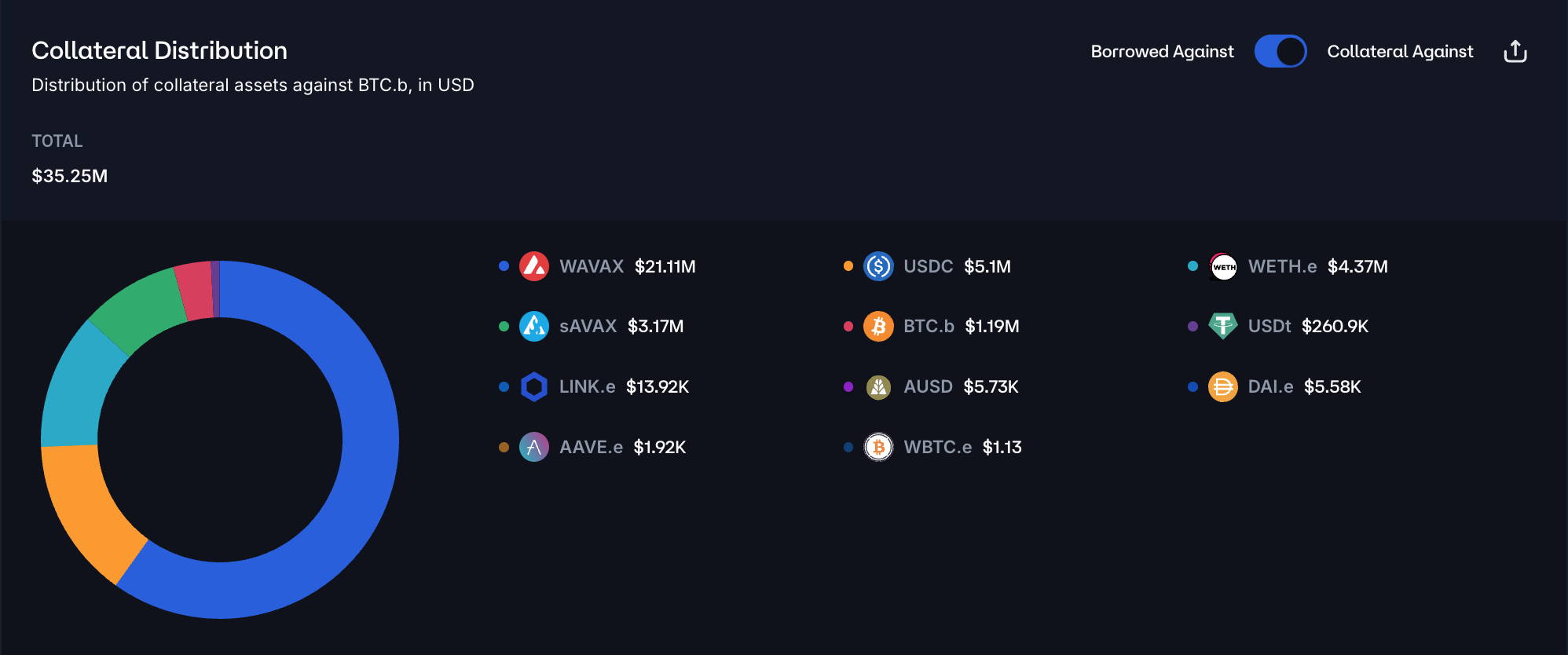

Borrow distribution of BTC.b is heavily concentrated, with the top 2 users having a 66.7% market share, while the top 7 borrowers account for almost 90% of the total. The distribution of health factors for top borrowers is in the safe 1.21 - 3 range, presenting minimal liquidation risk.

The majority of collateral posted against BTC.b is in volatile assets, including WAVAX, WETH, and sAVAX, with a combined dominance of 89%.

Liquidity

At the moment, onchain liquidity on Avalanche can support a sell order of 45 BTC.b with a limited 3% slippage, supporting a borrow cap increase.

Recommendation

We recommend raising the borrow cap for BTC.b on the Avalanche instance by 200 tokens, supported by low-risk borrowing patterns, ample on-chain liquidity to absorb potential liquidations, and steadily increasing market demand.

CELO (Celo)

CELO has reached 98% of its borrow cap at 195K tokens out of 200K, as the demand has doubled over the past 2 weeks. With a utilization rate of only 7%, we can increase the borrow cap to enable additional borrowing activity and price discovery.

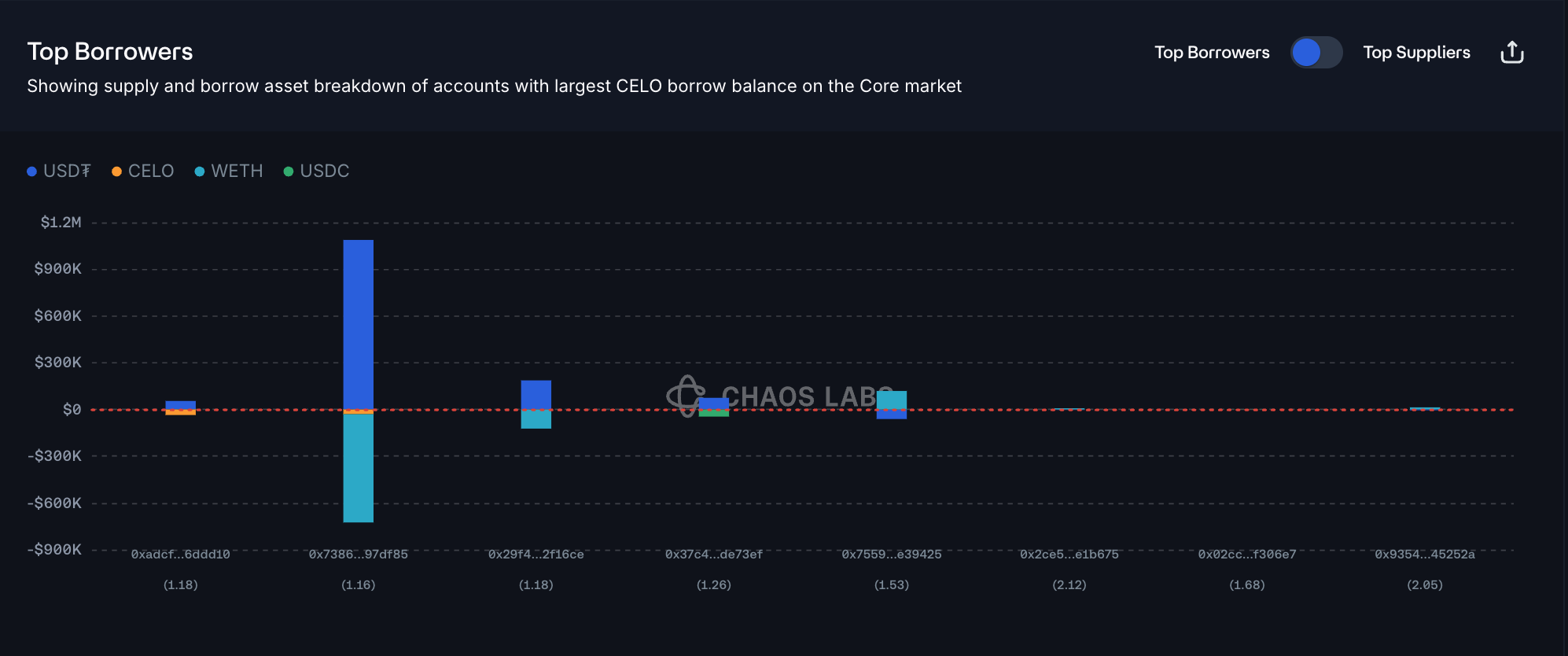

Borrow Distribution

While CELO’s borrow distribution is highly concentrated, with the top user accounting for 49% of the total, the actual borrowing volume in USD is relatively small, currently at $75K. Additionally, the top borrowers are in a slightly low but safe health factor range of 1.12-1.5, presenting minimal liquidation risk.

Liquidity

At present, CELO’s on-chain liquidity on the Celo network can accommodate a sell order of 200K CELO with only ~2% slippage, indicating sufficient depth to support a borrow cap increase.

Recommendation

Given the growing demand for CELO borrowing, safe user behavior, and relatively small USD volumes, we recommend increasing the borrow cap by 200K CELO.

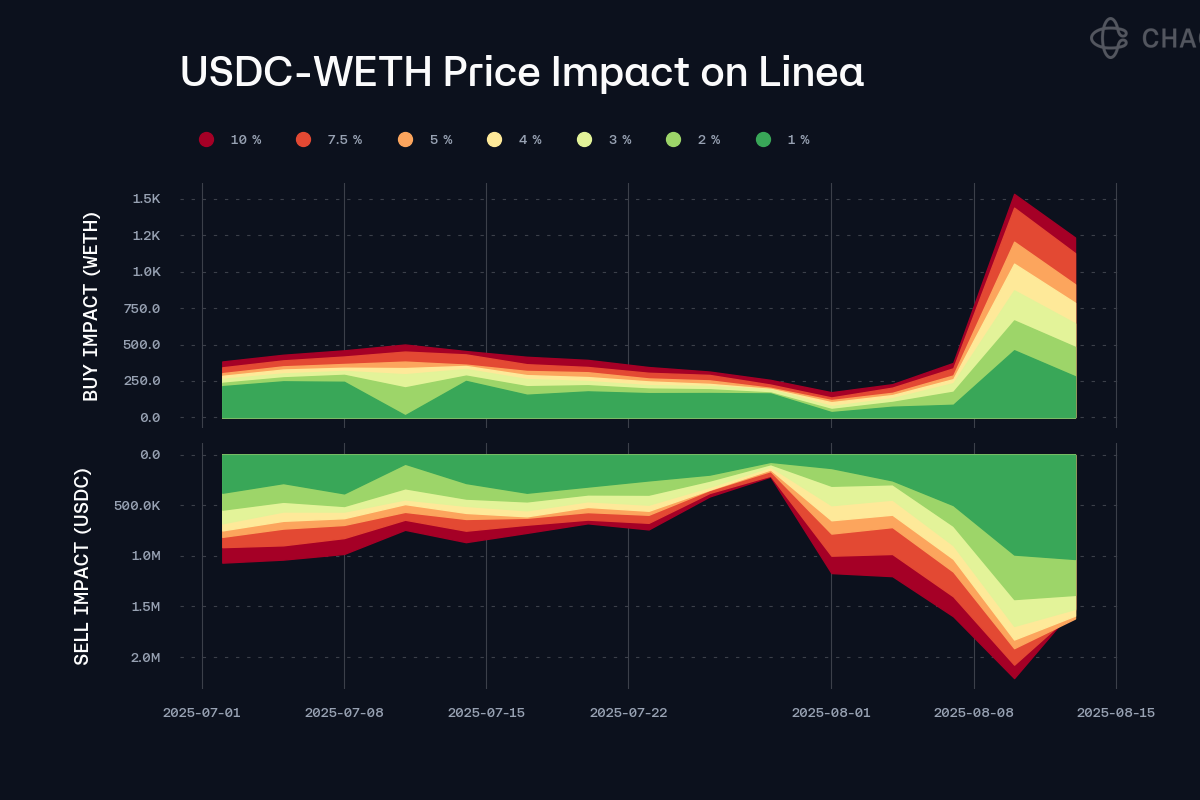

USDC (Linea)

USDC has reached 89% of its supply cap on Linea at 5.3M USDC, following an inflow of 2M during the last two days.

Supply Distribution

USDC’s supply distribution is moderately concentrated, with the top supplier representing approximately 18% of the market, while the top 50 positions account for a cumulative share of 50%. A small portion of the top suppliers have significant debt with health factors in the 1.11-1.17 range, while the majority have no debt at all, significantly reducing the risk of large-scale liquidations.

The overwhelming majority of debt against USDC collateral is WETH, with 94% dominance. Given the relatively moderate health of user positions, the market poses minimal liquidation risk.

Liquidity

USDC liquidity on Linea has been expanding rapidly over the past two weeks. At the moment, a sell order of 1.5M USDC would incur ~1% slippage, supporting an increase in the supply cap.

Recommendation

Considering strong demand, significant expansion in available liquidity, and user behavior, we recommend increasing the supply cap and borrow caps for USDC on Linea to 12M and 10.8M USDC, respectively.

wS (Sonic)

wS has reached 97% of its supply cap at 186.5M, primarily due to the inflow of 40M wS in the past 30 days via incentives.

Supply Distribution

The supply of wS is highly concentrated, as the top 5 wallets account for 50% of the supply, while the largest user supplies 19% of the total. The majority of suppliers either hold no debt or moderate amounts of USDC. The health factors are in the safe range from 1.48 to 4.63, presenting limited liquidation risk.

wS is predominantly used to collateralize USDC debt and a small share of volatile assets like WETH (1.5%) and wS (0.09%).

Recommendation

Given user behavior, low liquidation risks, and significant demand, we recommend increasing wS’s supply cap by 18M.

Specification

| Instance | Asset | Current Supply Cap | Recommended Supply Cap | Current Borrow Cap | Recommended Borrow Cap |

|---|---|---|---|---|---|

| Ethereum Core | PT-USDE-25SEP2025 | 1,400,000,000 | 1,800,000,000 | - | - |

| Ethereum Core | tBTC | 2,200 | 2,600 | - | - |

| Linea | USDC | 6,000,000 | 12,000,000 | 5,400,000 | 10,800,000 |

| Avalanche | BTC.b | 6,000 | - | 300 | 500 |

| Celo | CELO | 4,500,000 | - | 200,000 | 400,000 |

| Sonic | wS | 192,000,000 | 210,000,000 | 100,000,000 | - |

Next Steps

We will move forward and implement these updates via the Risk Steward process.

Disclosure

Chaos Labs has not been compensated by any third party for publishing this AGRS recommendation.

Copyright

Copyright and related rights waived via CC0.